Application of time-series quantum generative model to financial data

0

Sign in to get full access

Overview

- This paper explores the application of a time-series quantum generative model to financial data.

- The model aims to capture the complex dynamics of financial markets and generate realistic synthetic data for analysis and forecasting.

- The researchers evaluate the performance of the quantum model on real-world stock market data and compare it to classical time-series models.

Plain English Explanation

The paper investigates the use of a quantum machine learning approach to analyze and generate financial data, such as stock prices. Quantum computing is a emerging field that leverages the unique properties of quantum systems to potentially outperform classical computers on certain types of problems. In this case, the researchers developed a quantum-based model that can learn the patterns and trends in financial time-series data, and then use that knowledge to create simulated financial data that mimics the behavior of real markets.

The key idea is that the quantum model may be able to capture the complex, nonlinear dynamics of financial markets more effectively than traditional statistical models. By modeling the data in a quantum framework, the researchers hypothesize that the model can generate synthetic financial data that is more realistic and representative of real-world market behavior. This synthetic data could then be used for a variety of applications, such as improved financial forecasting via quantum machine learning, Fourier-series guided design of quantum convolutional neural networks, or comparing quantum vs. classical long short-term memory (LSTM) models.

Technical Explanation

The researchers developed a time-series quantum generative model (TSQG) to learn the underlying dynamics of financial time-series data. The model uses a quantum circuit to generate synthetic data that mimics the statistical properties of the real-world data.

The key elements of the TSQG model include:

-

Quantum Circuit Architecture: The model uses a quantum circuit with several qubits (the fundamental units of quantum information) and a series of gates that apply transformations to the qubits. This quantum circuit is trained on the financial time-series data to learn the underlying patterns.

-

Variational Quantum Circuit: The model employs a variational approach, where the parameters of the quantum circuit are iteratively adjusted to minimize the difference between the generated synthetic data and the real data, similar to the let quantum neural networks choose their own architecture approach.

-

Time-Series Modeling: The model is designed to capture the temporal dependencies in the financial data by incorporating a time-series structure into the quantum circuit. This allows the model to generate synthetic data that preserves the chaotic characteristics of the original time series.

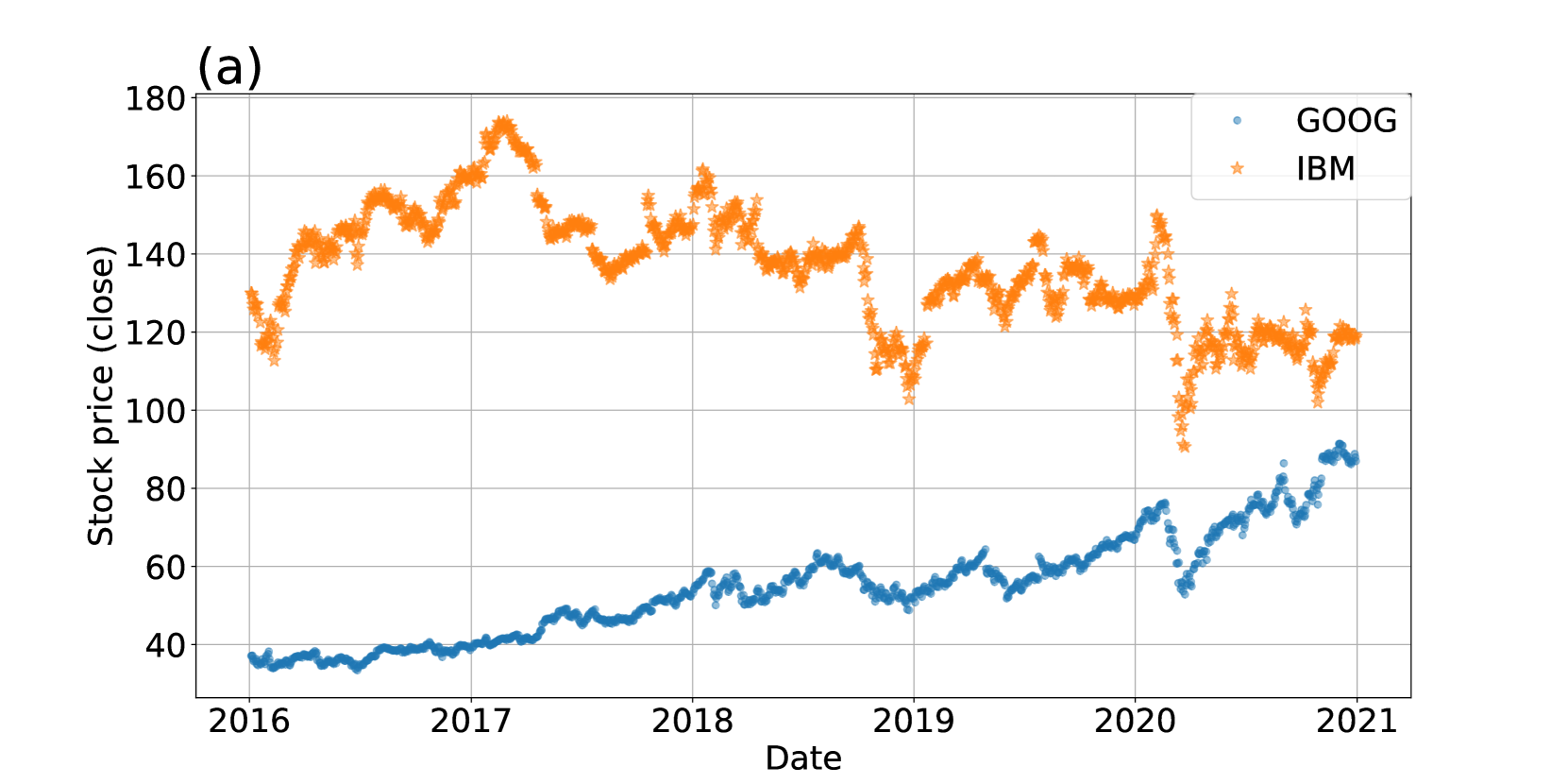

The researchers evaluate the performance of the TSQG model on real-world stock market data and compare it to classical time-series models, such as autoregressive (AR) and vector autoregressive (VAR) models. The results suggest that the quantum-based TSQG model can generate synthetic financial data that more closely matches the statistical properties of the real-world data, potentially making it a useful tool for financial analysis and forecasting.

Critical Analysis

The paper presents a novel application of quantum machine learning to the domain of financial time-series modeling. The researchers have made a compelling case for the potential benefits of using a quantum-based approach to capture the complex dynamics of financial markets.

However, it's important to note that the research is still in its early stages, and there are several limitations and areas for further exploration:

-

Scalability: The current implementation of the TSQG model may be limited in its ability to scale to larger, more complex financial datasets. The researchers acknowledge the need to optimize the quantum circuit design and training process to improve the model's scalability.

-

Interpretability: As with many machine learning models, the inner workings of the TSQG model can be difficult to interpret, making it challenging to understand the specific mechanisms by which the model is generating the synthetic data. Further research is needed to improve the interpretability of the model.

-

Real-World Applicability: While the model has shown promising results on the test datasets, its performance on real-world financial applications, such as portfolio optimization or risk management, remains to be demonstrated. Rigorous testing and validation in real-world financial settings would be necessary to assess the model's practical utility.

-

Computational Overhead: Quantum computing is still a relatively nascent field, and the computational resources required to run the TSQG model may be significant, potentially limiting its adoption in real-world financial applications. The researchers should explore ways to optimize the model's computational efficiency.

Despite these limitations, the paper represents an important step forward in the application of quantum machine learning to financial data analysis. As the field of quantum computing continues to evolve, the insights and techniques presented in this research could pave the way for more advanced and effective quantum-based financial modeling approaches in the future.

Conclusion

This paper explores the application of a time-series quantum generative model (TSQG) to financial data, with the goal of generating synthetic data that accurately captures the complex dynamics of financial markets. The researchers have developed a quantum-based model that can learn the underlying patterns in real-world stock market data and use that knowledge to create realistic simulated financial data.

The results suggest that the TSQG model outperforms classical time-series models in terms of its ability to generate synthetic data that closely matches the statistical properties of the original data. This synthetic data could potentially be used for a variety of applications, such as financial forecasting, risk analysis, and portfolio optimization.

While the research is still in its early stages and faces some limitations, the paper represents an important step forward in the application of quantum machine learning to the financial domain. As the field of quantum computing continues to evolve, the insights and techniques presented in this work could pave the way for more advanced and effective quantum-based financial modeling approaches in the future.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Application of time-series quantum generative model to financial data

Shun Okumura, Masayuki Ohzeki, Masaya Abe

Despite proposing a quantum generative model for time series that successfully learns correlated series with multiple Brownian motions, the model has not been adapted and evaluated for financial problems. In this study, a time-series generative model was applied as a quantum generative model to actual financial data. Future data for two correlated time series were generated and compared with classical methods such as long short-term memory and vector autoregression. Furthermore, numerical experiments were performed to complete missing values. Based on the results, we evaluated the practical applications of the time-series quantum generation model. It was observed that fewer parameter values were required compared with the classical method. In addition, the quantum time-series generation model was feasible for both stationary and nonstationary data. These results suggest that several parameters can be applied to various types of time-series data.

Read more5/21/2024

0

Exploring Biological Neuronal Correlations with Quantum Generative Models

Vinicius Hernandes, Eliska Greplova

Understanding of how biological neural networks process information is one of the biggest open scientific questions of our time. Advances in machine learning and artificial neural networks have enabled the modeling of neuronal behavior, but classical models often require a large number of parameters, complicating interpretability. Quantum computing offers an alternative approach through quantum machine learning, which can achieve efficient training with fewer parameters. In this work, we introduce a quantum generative model framework for generating synthetic data that captures the spatial and temporal correlations of biological neuronal activity. Our model demonstrates the ability to achieve reliable outcomes with fewer trainable parameters compared to classical methods. These findings highlight the potential of quantum generative models to provide new tools for modeling and understanding neuronal behavior, offering a promising avenue for future research in neuroscience.

Read more9/17/2024

0

QuaCK-TSF: Quantum-Classical Kernelized Time Series Forecasting

Abdallah Aaraba, Soumaya Cherkaoui, Ola Ahmad, Jean-Fr'ed'eric Laprade, Olivier Nahman-L'evesque, Alexis Vieloszynski, Shengrui Wang

Forecasting in probabilistic time series is a complex endeavor that extends beyond predicting future values to also quantifying the uncertainty inherent in these predictions. Gaussian process regression stands out as a Bayesian machine learning technique adept at addressing this multifaceted challenge. This paper introduces a novel approach that blends the robustness of this Bayesian technique with the nuanced insights provided by the kernel perspective on quantum models, aimed at advancing quantum kernelized probabilistic forecasting. We incorporate a quantum feature map inspired by Ising interactions and demonstrate its effectiveness in capturing the temporal dependencies critical for precise forecasting. The optimization of our model's hyperparameters circumvents the need for computationally intensive gradient descent by employing gradient-free Bayesian optimization. Comparative benchmarks against established classical kernel models are provided, affirming that our quantum-enhanced approach achieves competitive performance.

Read more8/23/2024

0

Improved Financial Forecasting via Quantum Machine Learning

Sohum Thakkar (QC Ware Corp), Skander Kazdaghli (QC Ware Corp), Natansh Mathur (QC Ware Corp, IRIF - Universit'e Paris Cit'e and CNRS), Iordanis Kerenidis (QC Ware Corp, IRIF - Universit'e Paris Cit'e and CNRS), Andr'e J. Ferreira-Martins (Ita'u Unibanco), Samurai Brito (Ita'u Unibanco)

Quantum algorithms have the potential to enhance machine learning across a variety of domains and applications. In this work, we show how quantum machine learning can be used to improve financial forecasting. First, we use classical and quantum Determinantal Point Processes to enhance Random Forest models for churn prediction, improving precision by almost 6%. Second, we design quantum neural network architectures with orthogonal and compound layers for credit risk assessment, which match classical performance with significantly fewer parameters. Our results demonstrate that leveraging quantum ideas can effectively enhance the performance of machine learning, both today as quantum-inspired classical ML solutions, and even more in the future, with the advent of better quantum hardware.

Read more4/5/2024