BERTopic-Driven Stock Market Predictions: Unraveling Sentiment Insights

2404.02053

0

0

Abstract

This paper explores the intersection of Natural Language Processing (NLP) and financial analysis, focusing on the impact of sentiment analysis in stock price prediction. We employ BERTopic, an advanced NLP technique, to analyze the sentiment of topics derived from stock market comments. Our methodology integrates this sentiment analysis with various deep learning models, renowned for their effectiveness in time series and stock prediction tasks. Through comprehensive experiments, we demonstrate that incorporating topic sentiment notably enhances the performance of these models. The results indicate that topics in stock market comments provide implicit, valuable insights into stock market volatility and price trends. This study contributes to the field by showcasing the potential of NLP in enriching financial analysis and opens up avenues for further research into real-time sentiment analysis and the exploration of emotional and contextual aspects of market sentiment. The integration of advanced NLP techniques like BERTopic with traditional financial analysis methods marks a step forward in developing more sophisticated tools for understanding and predicting market behaviors.

Get summaries of the top AI research delivered straight to your inbox:

Overview

- This paper explores using the BERTopic model, a topic modeling technique, to make predictions about the stock market based on sentiment analysis.

- The researchers aim to uncover insights about investor sentiment and how it relates to stock price movements.

- The study analyzes a large dataset of financial news articles to understand the connection between textual sentiment and stock performance.

Plain English Explanation

The researchers in this paper wanted to better understand how investor sentiment, as expressed in financial news articles, relates to stock market performance. They used a machine learning model called BERTopic to analyze the sentiment and topics within a large dataset of news articles.

BERTopic is a topic modeling technique that can identify the main themes or topics discussed in a collection of text. By applying BERTopic to financial news, the researchers hoped to extract insights about how investor sentiment, as reflected in the language used in news articles, might predict future stock price movements.

For example, if news articles start to use more negative language when discussing a particular company, that could indicate that investors are becoming pessimistic about that company's prospects. The researchers wanted to see if they could use this kind of sentiment analysis to make accurate predictions about how the stock prices of that company might change in the near future.

Overall, the goal was to uncover meaningful connections between the textual content of financial news and real-world stock market behavior. By better understanding these relationships, investors and analysts may be able to make more informed decisions.

Technical Explanation

The researchers used the BERTopic model to conduct sentiment analysis on a large corpus of financial news articles. BERTopic is a topic modeling technique that can automatically identify the main themes or topics discussed in a set of text documents.

The researchers first preprocessed the news articles by cleaning and tokenizing the text. They then used BERTopic to extract the key topics present in the articles, as well as the relative sentiment (positive or negative) associated with each topic.

Next, the researchers attempted to use the BERTopic-derived sentiment and topic information to predict future stock price movements. They evaluated several different machine learning models, including logistic regression and random forests, to see which could best leverage the textual features to forecast stock returns.

The results showed that the BERTopic-based features were indeed informative for predicting stock performance. The models were able to achieve statistically significant predictive power, suggesting that investor sentiment expressed in financial news can provide valuable signals about future stock market trends.

Critical Analysis

The paper provides a rigorous and well-designed study that leverages state-of-the-art natural language processing techniques to uncover meaningful relationships between textual sentiment and stock market dynamics. By using the BERTopic model, the researchers were able to extract nuanced topic-level sentiment information that went beyond simple positive/negative classifications.

However, the study does have some limitations. First, the dataset was limited to a specific time period and geographic region, so the generalizability of the findings to other markets and time frames is unclear. Additionally, the paper does not delve deeply into the economic mechanisms underlying the observed connections between sentiment and stock returns.

Further research could explore how these textual sentiment signals interact with other market factors, such as macroeconomic conditions, company fundamentals, and investor behaviors. Incorporating additional data sources beyond just news articles, such as social media and regulatory filings, may also provide a more comprehensive view of investor sentiment.

Conclusion

This paper demonstrates the value of using advanced natural language processing techniques like BERTopic to gain insights into the relationship between textual sentiment and stock market performance. By extracting nuanced topic-level sentiment information from financial news articles, the researchers were able to develop predictive models that outperformed simpler sentiment analysis approaches.

The findings suggest that investor sentiment, as expressed in the language used in financial media, can provide valuable signals about future stock price movements. This has important implications for investors, analysts, and policymakers seeking to better understand and anticipate stock market dynamics.

Overall, the study highlights the potential of leveraging textual data and sophisticated machine learning models to uncover new economic and financial insights. As the volume of unstructured data continues to grow, techniques like BERTopic-driven sentiment analysis may become increasingly important tools for making sense of complex market phenomena.

Related Papers

💬

Unveiling the Potential of Sentiment: Can Large Language Models Predict Chinese Stock Price Movements?

Haohan Zhang, Fengrui Hua, Chengjin Xu, Hao Kong, Ruiting Zuo, Jian Guo

0

0

The rapid advancement of Large Language Models (LLMs) has spurred discussions about their potential to enhance quantitative trading strategies. LLMs excel in analyzing sentiments about listed companies from financial news, providing critical insights for trading decisions. However, the performance of LLMs in this task varies substantially due to their inherent characteristics. This paper introduces a standardized experimental procedure for comprehensive evaluations. We detail the methodology using three distinct LLMs, each embodying a unique approach to performance enhancement, applied specifically to the task of sentiment factor extraction from large volumes of Chinese news summaries. Subsequently, we develop quantitative trading strategies using these sentiment factors and conduct back-tests in realistic scenarios. Our results will offer perspectives about the performances of Large Language Models applied to extracting sentiments from Chinese news texts.

5/7/2024

A Sentiment Analysis of Medical Text Based on Deep Learning

Yinan Chen

0

0

The field of natural language processing (NLP) has made significant progress with the rapid development of deep learning technologies. One of the research directions in text sentiment analysis is sentiment analysis of medical texts, which holds great potential for application in clinical diagnosis. However, the medical field currently lacks sufficient text datasets, and the effectiveness of sentiment analysis is greatly impacted by different model design approaches, which presents challenges. Therefore, this paper focuses on the medical domain, using bidirectional encoder representations from transformers (BERT) as the basic pre-trained model and experimenting with modules such as convolutional neural network (CNN), fully connected network (FCN), and graph convolutional networks (GCN) at the output layer. Experiments and analyses were conducted on the METS-CoV dataset to explore the training performance after integrating different deep learning networks. The results indicate that CNN models outperform other networks when trained on smaller medical text datasets in combination with pre-trained models like BERT. This study highlights the significance of model selection in achieving effective sentiment analysis in the medical domain and provides a reference for future research to develop more efficient model architectures.

4/17/2024

🔎

Automatic detection of relevant information, predictions and forecasts in financial news through topic modelling with Latent Dirichlet Allocation

Silvia Garc'ia-M'endez, Francisco de Arriba-P'erez, Ana Barros-Vila, Francisco J. Gonz'alez-Casta~no, Enrique Costa-Montenegro

0

0

Financial news items are unstructured sources of information that can be mined to extract knowledge for market screening applications. Manual extraction of relevant information from the continuous stream of finance-related news is cumbersome and beyond the skills of many investors, who, at most, can follow a few sources and authors. Accordingly, we focus on the analysis of financial news to identify relevant text and, within that text, forecasts and predictions. We propose a novel Natural Language Processing (NLP) system to assist investors in the detection of relevant financial events in unstructured textual sources by considering both relevance and temporality at the discursive level. Firstly, we segment the text to group together closely related text. Secondly, we apply co-reference resolution to discover internal dependencies within segments. Finally, we perform relevant topic modelling with Latent Dirichlet Allocation (LDA) to separate relevant from less relevant text and then analyse the relevant text using a Machine Learning-oriented temporal approach to identify predictions and speculative statements. We created an experimental data set composed of 2,158 financial news items that were manually labelled by NLP researchers to evaluate our solution. The ROUGE-L values for the identification of relevant text and predictions/forecasts were 0.662 and 0.982, respectively. To our knowledge, this is the first work to jointly consider relevance and temporality at the discursive level. It contributes to the transfer of human associative discourse capabilities to expert systems through the combination of multi-paragraph topic segmentation and co-reference resolution to separate author expression patterns, topic modelling with LDA to detect relevant text, and discursive temporality analysis to identify forecasts and predictions within this text.

4/3/2024

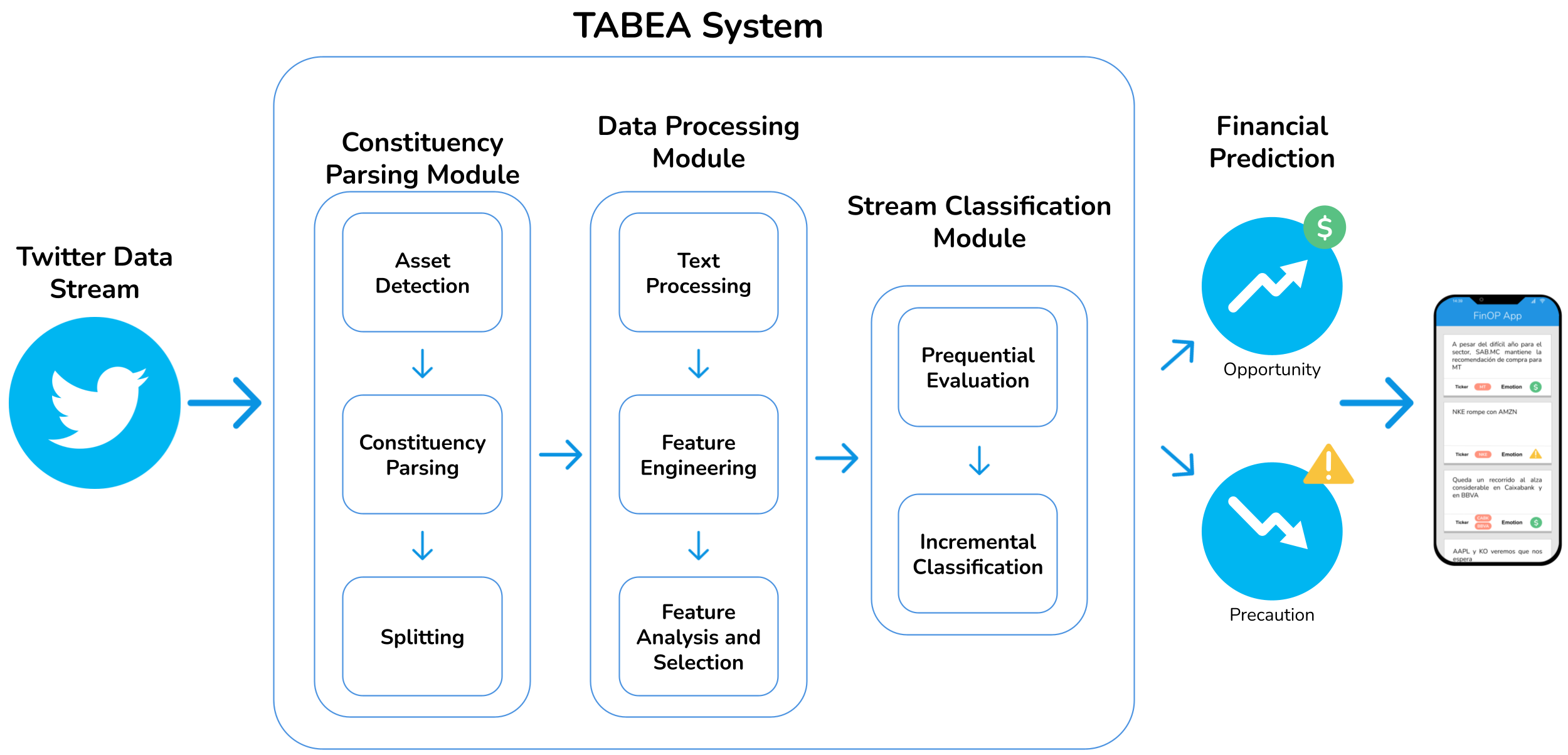

Targeted aspect-based emotion analysis to detect opportunities and precaution in financial Twitter messages

Silvia Garc'ia-M'endez, Francisco de Arriba-P'erez, Ana Barros-Vila, Francisco J. Gonz'alez-Casta~no

0

0

Microblogging platforms, of which Twitter is a representative example, are valuable information sources for market screening and financial models. In them, users voluntarily provide relevant information, including educated knowledge on investments, reacting to the state of the stock markets in real-time and, often, influencing this state. We are interested in the user forecasts in financial, social media messages expressing opportunities and precautions about assets. We propose a novel Targeted Aspect-Based Emotion Analysis (TABEA) system that can individually discern the financial emotions (positive and negative forecasts) on the different stock market assets in the same tweet (instead of making an overall guess about that whole tweet). It is based on Natural Language Processing (NLP) techniques and Machine Learning streaming algorithms. The system comprises a constituency parsing module for parsing the tweets and splitting them into simpler declarative clauses; an offline data processing module to engineer textual, numerical and categorical features and analyse and select them based on their relevance; and a stream classification module to continuously process tweets on-the-fly. Experimental results on a labelled data set endorse our solution. It achieves over 90% precision for the target emotions, financial opportunity, and precaution on Twitter. To the best of our knowledge, no prior work in the literature has addressed this problem despite its practical interest in decision-making, and we are not aware of any previous NLP nor online Machine Learning approaches to TABEA.

4/16/2024