Can ChatGPT Forecast Stock Price Movements? Return Predictability and Large Language Models

0

💬

Sign in to get full access

Overview

- This paper explores the capability of large language models (LLMs) like ChatGPT to predict stock price movements using news headlines, without direct financial training.

- The researchers find that ChatGPT's scores significantly predict out-of-sample daily stock returns, outperforming traditional methods.

- The predictability is stronger among smaller stocks and following negative news.

- The researchers develop a theoretical model to explain these findings, incorporating information capacity constraints, underreaction, limits-to-arbitrage, and LLMs.

- The model makes several key predictions, which are empirically tested.

- The paper also introduces an interpretability framework to evaluate LLMs' reasoning, contributing to AI transparency and economic decision-making.

Plain English Explanation

The researchers wanted to see if large language models (LLMs) like ChatGPT could predict how stock prices will change, even without being specifically trained on financial data. They found that ChatGPT's scores, which measure how it interprets news headlines, can actually predict future daily stock returns better than traditional methods.

This predictability was stronger for smaller companies and when the news was negative. To explain these findings, the researchers created a theoretical model that takes into account things like the limits on how much information LLMs can process, how investors sometimes underreact to news, and the constraints on being able to take advantage of these predictions.

The model made some key predictions, which the researchers then tested with data. For example, the model showed that there is a critical level of AI capability needed to make profitable predictions, and that only advanced LLMs can effectively interpret complex information like news articles.

The researchers also introduced a way to better understand how the LLMs are reasoning, which helps make these AI systems more transparent and useful for economic decision-making. Overall, the study suggests that sophisticated AI systems can now forecast stock returns in a way that was previously difficult, and this could change how information spreads and decisions are made in financial markets.

Technical Explanation

The researchers first demonstrate that ChatGPT's scores, which measure its interpretation of news headlines, can significantly predict out-of-sample daily stock returns. This predictability is stronger among smaller stocks and following negative news.

To explain these findings, the researchers develop a theoretical model that incorporates information capacity constraints, underreaction, limits-to-arbitrage, and the capabilities of LLMs. The model makes several key predictions:

-

It establishes a critical threshold in AI capabilities necessary for profitable predictions. Below this threshold, AI systems cannot effectively interpret complex information.

-

It shows that only advanced LLMs like ChatGPT have the necessary information processing power to extract predictive signals from news.

-

It predicts that widespread LLM adoption can enhance market efficiency by improving information diffusion and decision-making.

The researchers empirically test these model predictions using data. They also introduce an interpretability framework to evaluate how LLMs reason, contributing to AI transparency and economic decision-making.

Critical Analysis

The paper provides a comprehensive theoretical and empirical analysis of LLMs' ability to forecast stock returns. However, there are a few potential limitations and areas for further research:

-

The study focuses on ChatGPT, which may have unique capabilities compared to other LLMs. Evaluating a broader range of models could strengthen the generalizability of the findings.

-

The paper does not explore the potential risks or downsides of widespread LLM adoption in financial markets, such as increased volatility or the concentration of power in the hands of a few AI-driven traders.

-

The interpretability framework is a useful first step, but more work is needed to fully understand the "black box" decision-making of these complex models and ensure their transparency and accountability.

Despite these caveats, the research presents a compelling case for the emerging capabilities of AI systems in sophisticated financial forecasting and the potential for these technologies to transform information diffusion and decision-making in markets.

Conclusion

This paper documents the impressive ability of large language models like ChatGPT to predict stock price movements using news headlines, even without direct financial training. The researchers develop a theoretical model to explain these findings, highlighting the critical thresholds in AI capabilities, the advantages of advanced LLMs, and the potential for widespread LLM adoption to enhance market efficiency.

By introducing an interpretability framework, the study also contributes to the transparency and economic decision-making applications of these AI systems. Overall, the research suggests that sophisticated return forecasting is an emerging capability of AI, with significant implications for how information flows and decisions are made in financial markets.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

💬

0

Can ChatGPT Forecast Stock Price Movements? Return Predictability and Large Language Models

Alejandro Lopez-Lira, Yuehua Tang

We document the capability of large language models (LLMs) like ChatGPT to predict stock price movements using news headlines, even without direct financial training. ChatGPT scores significantly predict out-of-sample daily stock returns, subsuming traditional methods, and predictability is stronger among smaller stocks and following negative news. To explain these findings, we develop a theoretical model incorporating information capacity constraints, underreaction, limits-to-arbitrage, and LLMs. The model generates several key predictions, which we empirically test: (i) it establishes a critical threshold in AI capabilities necessary for profitable predictions, (ii) it demonstrates that only advanced LLMs can effectively interpret complex information, and (iii) it predicts that widespread LLM adoption can enhance market efficiency. Our results suggest that sophisticated return forecasting is an emerging capability of AI systems and that these technologies can alter information diffusion and decision-making processes in financial markets. Finally, we introduce an interpretability framework to evaluate LLMs' reasoning, contributing to AI transparency and economic decision-making.

Read more9/14/2024

0

StockGPT: A GenAI Model for Stock Prediction and Trading

Dat Mai

This paper introduces StockGPT, an autoregressive ``number'' model trained and tested on 70 million daily U.S. stock returns over nearly 100 years. Treating each return series as a sequence of tokens, StockGPT automatically learns the hidden patterns predictive of future returns via its attention mechanism. On a held-out test sample from 2001 to 2023, a daily rebalanced long-short portfolio formed from StockGPT predictions earns an annual return of 119% with a Sharpe ratio of 6.5. The StockGPT-based portfolio completely spans momentum and long-/short-term reversals, eliminating the need for manually crafted price-based strategies, and also encompasses most leading stock market factors. This highlights the immense promise of generative AI in surpassing human in making complex financial investment decisions.

Read more4/11/2024

0

Financial Statement Analysis with Large Language Models

Alex Kim, Maximilian Muhn, Valeri Nikolaev

We investigate whether an LLM can successfully perform financial statement analysis in a way similar to a professional human analyst. We provide standardized and anonymous financial statements to GPT4 and instruct the model to analyze them to determine the direction of future earnings. Even without any narrative or industry-specific information, the LLM outperforms financial analysts in its ability to predict earnings changes. The LLM exhibits a relative advantage over human analysts in situations when the analysts tend to struggle. Furthermore, we find that the prediction accuracy of the LLM is on par with the performance of a narrowly trained state-of-the-art ML model. LLM prediction does not stem from its training memory. Instead, we find that the LLM generates useful narrative insights about a company's future performance. Lastly, our trading strategies based on GPT's predictions yield a higher Sharpe ratio and alphas than strategies based on other models. Taken together, our results suggest that LLMs may take a central role in decision-making.

Read more7/26/2024

0

Can Large Language Models Beat Wall Street? Unveiling the Potential of AI in Stock Selection

Georgios Fatouros, Konstantinos Metaxas, John Soldatos, Dimosthenis Kyriazis

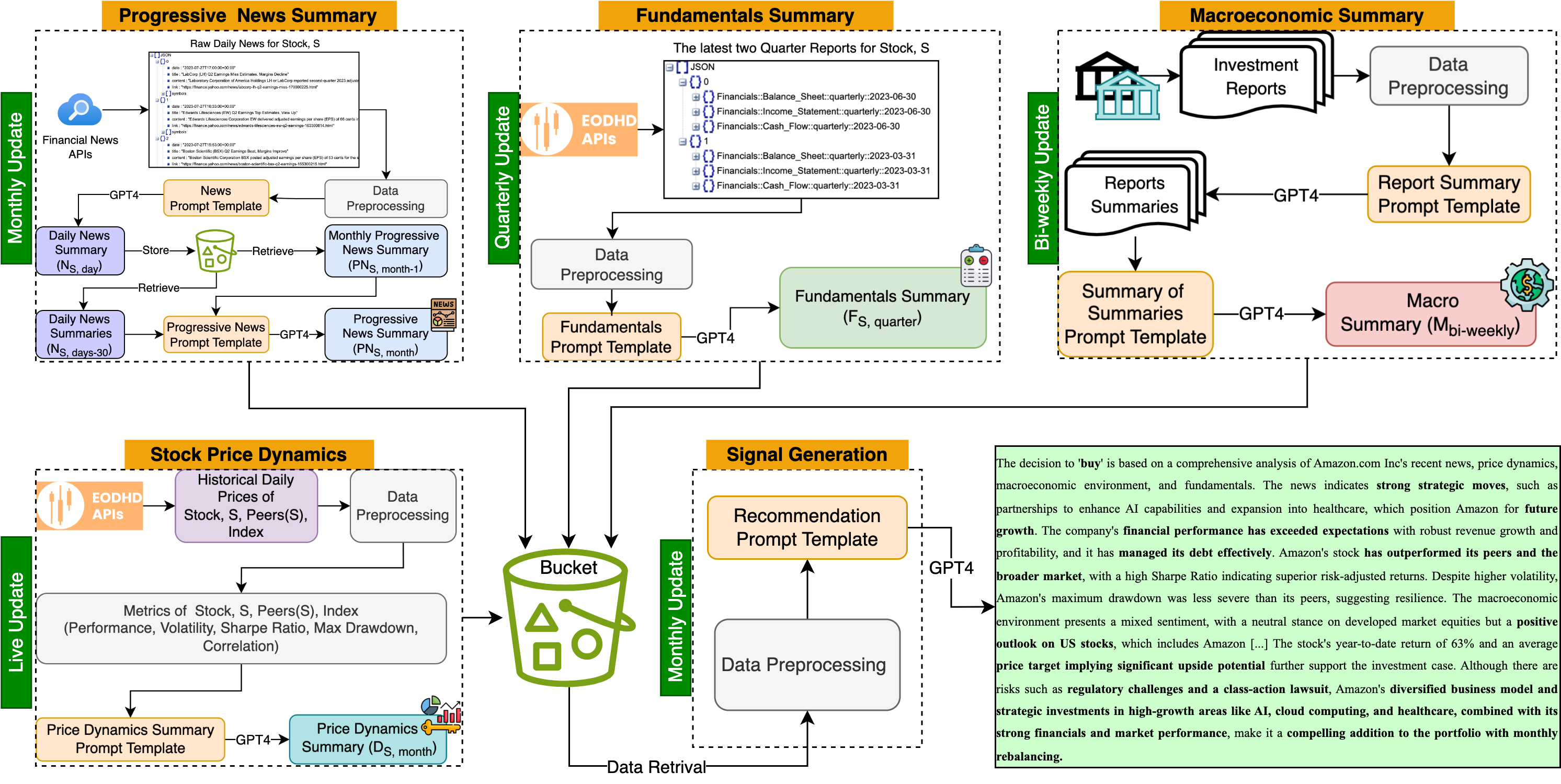

This paper introduces MarketSenseAI, an innovative framework leveraging GPT-4's advanced reasoning for selecting stocks in financial markets. By integrating Chain of Thought and In-Context Learning, MarketSenseAI analyzes diverse data sources, including market trends, news, fundamentals, and macroeconomic factors, to emulate expert investment decision-making. The development, implementation, and validation of the framework are elaborately discussed, underscoring its capability to generate actionable and interpretable investment signals. A notable feature of this work is employing GPT-4 both as a predictive mechanism and signal evaluator, revealing the significant impact of the AI-generated explanations on signal accuracy, reliability and acceptance. Through empirical testing on the competitive S&P 100 stocks over a 15-month period, MarketSenseAI demonstrated exceptional performance, delivering excess alpha of 10% to 30% and achieving a cumulative return of up to 72% over the period, while maintaining a risk profile comparable to the broader market. Our findings highlight the transformative potential of Large Language Models in financial decision-making, marking a significant leap in integrating generative AI into financial analytics and investment strategies.

Read more4/5/2024