Deep Learning for Options Trading: An End-To-End Approach

0

Sign in to get full access

Overview

- This paper presents an end-to-end deep learning approach for options trading.

- The proposed model combines several deep learning techniques to predict option prices and generate trading strategies.

- The model is evaluated on real-world options data and shows promising results in terms of profitability and risk management.

Plain English Explanation

The paper describes a new way to use deep learning, a type of artificial intelligence, to help with options trading. Options are a type of financial instrument that allow investors to buy or sell assets at a specific price in the future. The deep learning model in this paper is designed to predict the future prices of options and then use that information to generate profitable trading strategies.

The model combines several different deep learning techniques, including reinforcement learning and multi-asset optimization, to make these predictions and decisions. The researchers tested the model on real-world options data and found that it was able to generate trading strategies that were both profitable and managed risk well.

The key idea behind this work is to leverage the power of deep learning to automate and improve the process of options trading, which can be complex and difficult for human traders to manage effectively. By using a deep learning model, the researchers aim to take advantage of patterns in financial data that may be difficult for humans to detect.

Technical Explanation

The paper presents an end-to-end deep learning approach for options trading that combines several key components:

-

Option Price Prediction: The model uses a deep neural network to predict the future prices of options based on historical market data and other relevant features.

-

Trading Strategy Generation: The model then uses reinforcement learning to generate trading strategies that aim to maximize profitability while managing risk, based on the predicted option prices.

-

Multi-Asset Optimization: To further improve the trading strategies, the model also considers the interactions between different options and other assets, using techniques from multi-asset optimization.

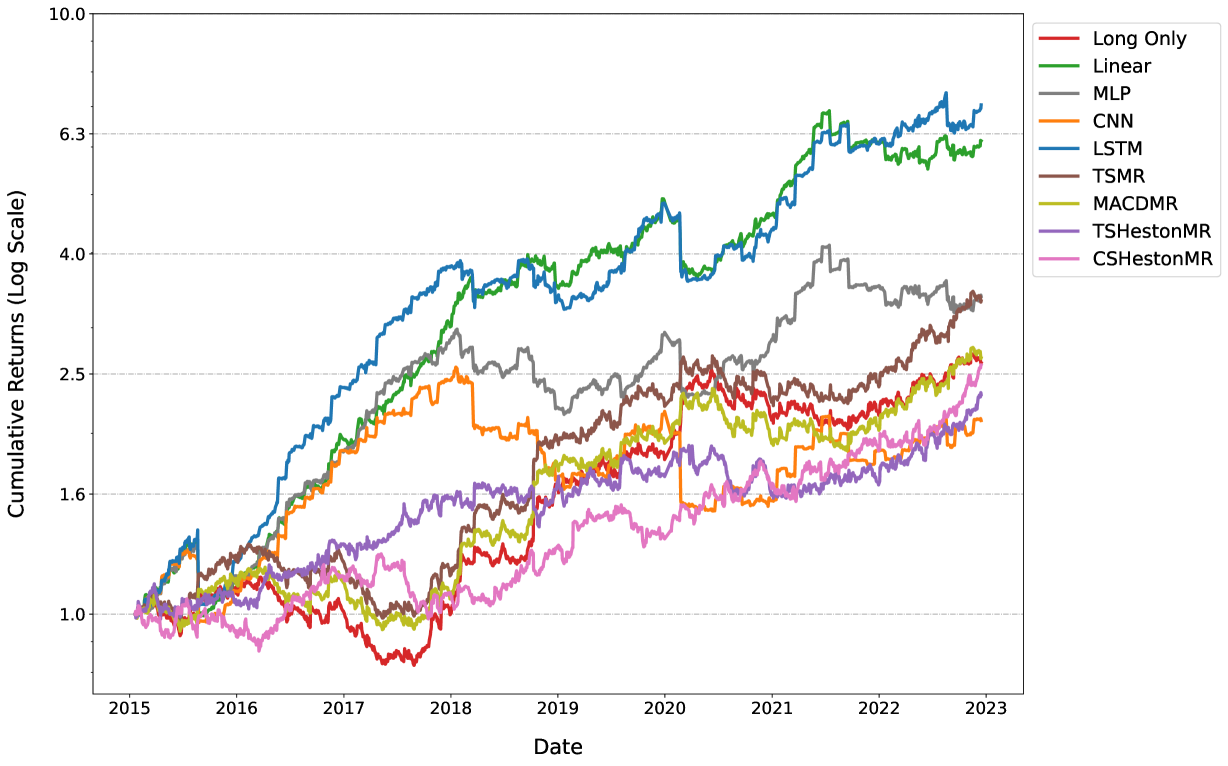

The researchers evaluated the performance of their model on real-world options data from the S&P 500 index. They found that the model was able to generate trading strategies that outperformed several benchmark strategies in terms of profitability and risk management.

Critical Analysis

The paper presents a promising approach to using deep learning for options trading, but there are a few potential limitations and areas for further research:

-

Data Availability and Quality: The performance of the model is heavily dependent on the availability and quality of the historical options data used for training. In practice, obtaining high-quality and comprehensive data may be a challenge.

-

Model Complexity and Interpretability: The combination of multiple deep learning techniques makes the model quite complex, which could make it difficult to interpret the underlying decision-making process. This could be a concern for some investors who prefer more transparent and explainable strategies.

-

Real-World Deployment Challenges: While the model shows promising results in the paper, there may be additional challenges in deploying it in a real-world trading environment, such as dealing with market volatility, transaction costs, and regulatory constraints.

-

Potential Overfitting: As with any machine learning model, there is a risk of overfitting the training data, which could lead to poor generalization to new, unseen market conditions. The researchers should carefully monitor the model's performance on out-of-sample data.

Overall, the paper presents an innovative approach to options trading using deep learning, but further research and real-world testing will be necessary to fully assess the practical viability and limitations of the proposed method.

Conclusion

This paper introduces an end-to-end deep learning approach for options trading that combines option price prediction, trading strategy generation, and multi-asset optimization. The model shows promising results in terms of profitability and risk management when evaluated on real-world options data. While the approach is innovative and has the potential to improve the efficiency and performance of options trading, there are also some potential limitations and areas for further research, such as data availability, model interpretability, and real-world deployment challenges. Overall, this work demonstrates the growing application of deep learning techniques in the financial domain and highlights the need for continued research and development in this area.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Deep Learning for Options Trading: An End-To-End Approach

Wee Ling Tan, Stephen Roberts, Stefan Zohren

We introduce a novel approach to options trading strategies using a highly scalable and data-driven machine learning algorithm. In contrast to traditional approaches that often require specifications of underlying market dynamics or assumptions on an option pricing model, our models depart fundamentally from the need for these prerequisites, directly learning non-trivial mappings from market data to optimal trading signals. Backtesting on more than a decade of option contracts for equities listed on the S&P 100, we demonstrate that deep learning models trained according to our end-to-end approach exhibit significant improvements in risk-adjusted performance over existing rules-based trading strategies. We find that incorporating turnover regularization into the models leads to further performance enhancements at prohibitively high levels of transaction costs.

Read more8/1/2024

0

Pricing American Options using Machine Learning Algorithms

Prudence Djagba, Callixte Ndizihiwe

This study investigates the application of machine learning algorithms, particularly in the context of pricing American options using Monte Carlo simulations. Traditional models, such as the Black-Scholes-Merton framework, often fail to adequately address the complexities of American options, which include the ability for early exercise and non-linear payoff structures. By leveraging Monte Carlo methods in conjunction Least Square Method machine learning was used. This research aims to improve the accuracy and efficiency of option pricing. The study evaluates several machine learning models, including neural networks and decision trees, highlighting their potential to outperform traditional approaches. The results from applying machine learning algorithm in LSM indicate that integrating machine learning with Monte Carlo simulations can enhance pricing accuracy and provide more robust predictions, offering significant insights into quantitative finance by merging classical financial theories with modern computational techniques. The dataset was split into features and the target variable representing bid prices, with an 80-20 train-validation split. LSTM and GRU models were constructed using TensorFlow's Keras API, each with four hidden layers of 200 neurons and an output layer for bid price prediction, optimized with the Adam optimizer and MSE loss function. The GRU model outperformed the LSTM model across all evaluated metrics, demonstrating lower mean absolute error, mean squared error, and root mean squared error, along with greater stability and efficiency in training.

Read more9/6/2024

📊

0

Data Scaling Effect of Deep Learning in Financial Time Series Forecasting

Chen Liu, Minh-Ngoc Tran, Chao Wang, Richard Gerlach, Robert Kohn

For years, researchers investigated the applications of deep learning in forecasting financial time series. However, they continued to rely on the conventional econometric approach for model training that optimizes the deep learning models on individual assets. This study highlights the importance of global training, where the deep learning model is optimized across a wide spectrum of stocks. Focusing on stock volatility forecasting as an exemplar, we show that global training is not only beneficial but also necessary for deep learning-based financial time series forecasting. We further demonstrate that, given a sufficient amount of training data, a globally trained deep learning model is capable of delivering accurate zero-shot forecasts for any stocks.

Read more6/4/2024

🤿

0

Optimizing Deep Reinforcement Learning for American Put Option Hedging

Reilly Pickard, F. Wredenhagen, Y. Lawryshyn

This paper contributes to the existing literature on hedging American options with Deep Reinforcement Learning (DRL). The study first investigates hyperparameter impact on hedging performance, considering learning rates, training episodes, neural network architectures, training steps, and transaction cost penalty functions. Results highlight the importance of avoiding certain combinations, such as high learning rates with a high number of training episodes or low learning rates with few training episodes and emphasize the significance of utilizing moderate values for optimal outcomes. Additionally, the paper warns against excessive training steps to prevent instability and demonstrates the superiority of a quadratic transaction cost penalty function over a linear version. This study then expands upon the work of Pickard et al. (2024), who utilize a Chebyshev interpolation option pricing method to train DRL agents with market calibrated stochastic volatility models. While the results of Pickard et al. (2024) showed that these DRL agents achieve satisfactory performance on empirical asset paths, this study introduces a novel approach where new agents at weekly intervals to newly calibrated stochastic volatility models. Results show DRL agents re-trained using weekly market data surpass the performance of those trained solely on the sale date. Furthermore, the paper demonstrates that both single-train and weekly-train DRL agents outperform the Black-Scholes Delta method at transaction costs of 1% and 3%. This practical relevance suggests that practitioners can leverage readily available market data to train DRL agents for effective hedging of options in their portfolios.

Read more5/15/2024