Design and Optimization of Big Data and Machine Learning-Based Risk Monitoring System in Financial Markets

0

🛠️

Sign in to get full access

Overview

- The complexity of financial markets and rapid growth in data have made traditional risk monitoring methods insufficient for modern financial institutions.

- This paper designs and optimizes a risk monitoring system based on big data and machine learning.

- The system effectively integrates large-scale financial data and advanced machine learning algorithms through a four-layer architecture.

- Key technologies employed include Long Short-Term Memory (LSTM) networks, Random Forest, Gradient Boosting Trees, and the real-time data processing platform Apache Flink.

- The system aims to enhance efficiency and accuracy in risk management, particularly in identifying and warning against market crash risks.

Plain English Explanation

Financial markets have become increasingly complex, and the amount of data available has grown rapidly. Traditional methods of monitoring risk are no longer adequate for modern financial institutions. This paper describes the design and optimization of a new risk monitoring system that uses big data and machine learning techniques.

The system has a four-layer architecture that allows it to effectively integrate large amounts of financial data and advanced machine learning algorithms. It uses specific technologies like LSTM networks, Random Forest, and Gradient Boosting Trees to analyze the data in real-time using the Apache Flink platform.

The goal of this system is to improve the efficiency and accuracy of risk management, especially when it comes to identifying and providing early warnings about the risk of market crashes. By using advanced analytics and processing large amounts of data quickly, the system aims to help financial institutions better understand and prepare for potential financial crises.

Technical Explanation

The paper describes a four-layer architecture for the risk monitoring system:

- Data Layer: Collects and preprocesses large-scale financial data from various sources.

- Algorithm Layer: Employs advanced machine learning algorithms such as LSTM networks, Random Forest, and Gradient Boosting Trees to analyze the data and identify risk patterns.

- Processing Layer: Uses the Apache Flink real-time data processing platform to enable low-latency, high-throughput risk monitoring.

- Application Layer: Provides risk monitoring and warning functionalities to end-users, such as financial institutions and regulators.

The researchers tested the system's performance on historical financial data and found that it significantly outperformed traditional risk monitoring methods in terms of efficiency and accuracy. The system was particularly effective in identifying and providing early warnings about the risk of market crashes.

Critical Analysis

The paper provides a comprehensive and well-designed solution for addressing the challenges of modern risk monitoring in financial markets. However, some potential limitations and areas for further research are worth considering:

- The system's performance may be dependent on the quality and completeness of the financial data used for training. Ensuring the availability and integrity of this data could be a significant challenge in real-world deployments.

- The paper does not discuss the computational resources required to run the system, which could be a concern for smaller financial institutions with limited IT infrastructure.

- While the paper highlights the system's effectiveness in identifying market crash risks, it would be valuable to understand its performance in detecting other types of financial risks, such as credit risk or operational risk.

- The researchers could consider expanding the system's capabilities to include not only risk monitoring but also risk mitigation and response strategies, providing a more holistic solution for financial institutions.

Conclusion

This paper presents a promising approach to addressing the challenges of risk monitoring in the modern financial landscape. By leveraging big data and advanced machine learning techniques, the proposed system demonstrates significant improvements in efficiency and accuracy compared to traditional methods, particularly in the area of market crash risk identification.

While the paper highlights several key strengths of the system, it also raises some areas for further exploration and improvement. Continued research and real-world deployments could help refine the system and expand its capabilities to provide a comprehensive risk management solution for financial institutions.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

🛠️

0

Design and Optimization of Big Data and Machine Learning-Based Risk Monitoring System in Financial Markets

Liyang Wang, Yu Cheng, Xingxin Gu, Zhizhong Wu

With the increasing complexity of financial markets and rapid growth in data volume, traditional risk monitoring methods no longer suffice for modern financial institutions. This paper designs and optimizes a risk monitoring system based on big data and machine learning. By constructing a four-layer architecture, it effectively integrates large-scale financial data and advanced machine learning algorithms. Key technologies employed in the system include Long Short-Term Memory (LSTM) networks, Random Forest, Gradient Boosting Trees, and real-time data processing platform Apache Flink, ensuring the real-time and accurate nature of risk monitoring. Research findings demonstrate that the system significantly enhances efficiency and accuracy in risk management, particularly excelling in identifying and warning against market crash risks.

Read more7/30/2024

📊

0

New!Research and Design of a Financial Intelligent Risk Control Platform Based on Big Data Analysis and Deep Machine Learning

Shuochen Bi, Yufan Lian, Ziyue Wang

In the financial field of the United States, the application of big data technology has become one of the important means for financial institutions to enhance competitiveness and reduce risks. The core objective of this article is to explore how to fully utilize big data technology to achieve complete integration of internal and external data of financial institutions, and create an efficient and reliable platform for big data collection, storage, and analysis. With the continuous expansion and innovation of financial business, traditional risk management models are no longer able to meet the increasingly complex market demands. This article adopts big data mining and real-time streaming data processing technology to monitor, analyze, and alert various business data. Through statistical analysis of historical data and precise mining of customer transaction behavior and relationships, potential risks can be more accurately identified and timely responses can be made. This article designs and implements a financial big data intelligent risk control platform. This platform not only achieves effective integration, storage, and analysis of internal and external data of financial institutions, but also intelligently displays customer characteristics and their related relationships, as well as intelligent supervision of various risk information

Read more9/17/2024

🔮

0

Advancing Financial Risk Prediction Through Optimized LSTM Model Performance and Comparative Analysis

Ke Xu, Yu Cheng, Shiqing Long, Junjie Guo, Jue Xiao, Mengfang Sun

This paper focuses on the application and optimization of LSTM model in financial risk prediction. The study starts with an overview of the architecture and algorithm foundation of LSTM, and then details the model training process and hyperparameter tuning strategy, and adjusts network parameters through experiments to improve performance. Comparative experiments show that the optimized LSTM model shows significant advantages in AUC index compared with random forest, BP neural network and XGBoost, which verifies its efficiency and practicability in the field of financial risk prediction, especially its ability to deal with complex time series data, which lays a solid foundation for the application of the model in the actual production environment.

Read more6/3/2024

0

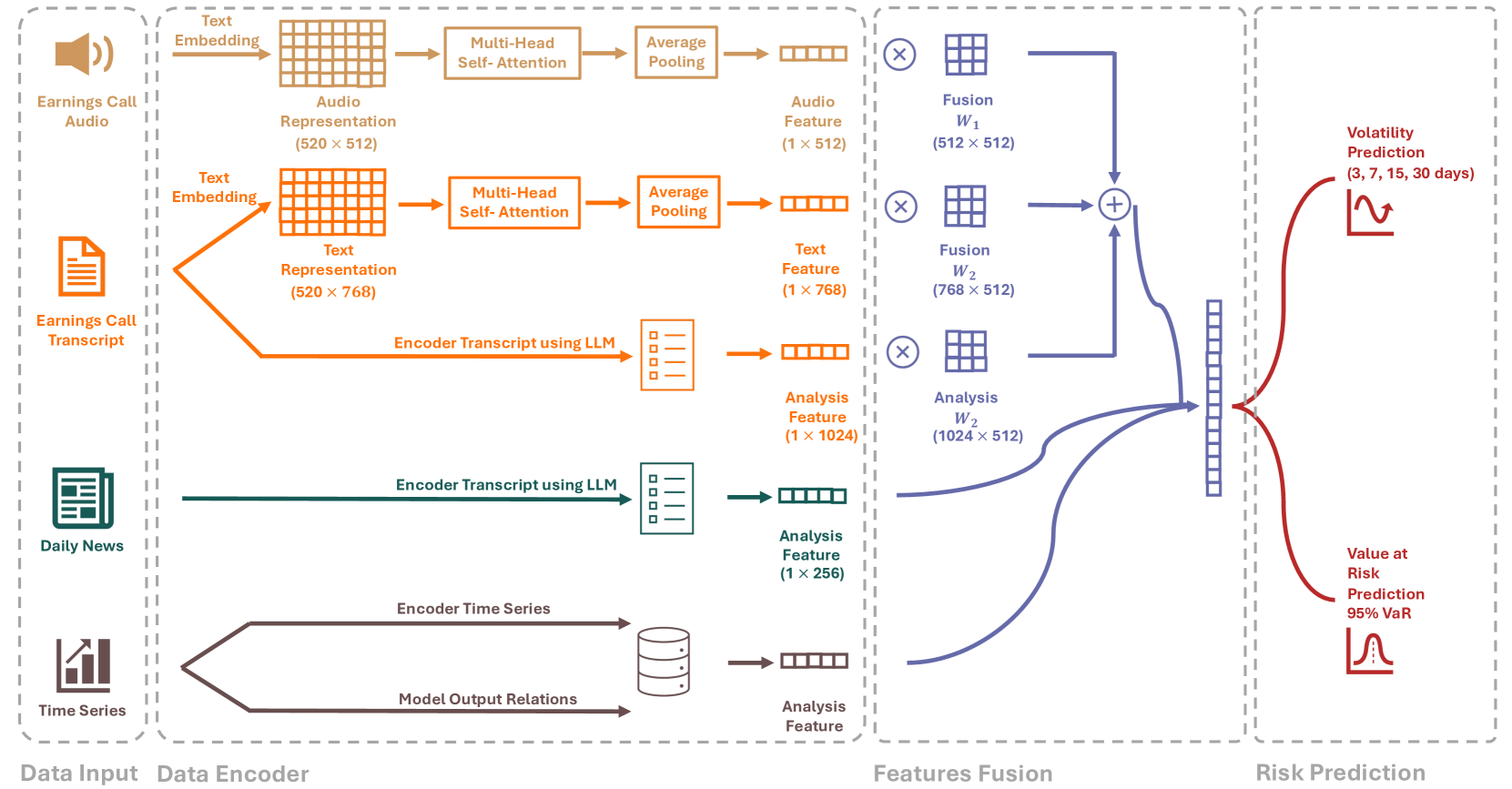

RiskLabs: Predicting Financial Risk Using Large Language Model Based on Multi-Sources Data

Yupeng Cao, Zhi Chen, Qingyun Pei, Fabrizio Dimino, Lorenzo Ausiello, Prashant Kumar, K. P. Subbalakshmi, Papa Momar Ndiaye

The integration of Artificial Intelligence (AI) techniques, particularly large language models (LLMs), in finance has garnered increasing academic attention. Despite progress, existing studies predominantly focus on tasks like financial text summarization, question-answering (Q$&$A), and stock movement prediction (binary classification), with a notable gap in the application of LLMs for financial risk prediction. Addressing this gap, in this paper, we introduce textbf{RiskLabs}, a novel framework that leverages LLMs to analyze and predict financial risks. RiskLabs uniquely combines different types of financial data, including textual and vocal information from Earnings Conference Calls (ECCs), market-related time series data, and contextual news data surrounding ECC release dates. Our approach involves a multi-stage process: initially extracting and analyzing ECC data using LLMs, followed by gathering and processing time-series data before the ECC dates to model and understand risk over different timeframes. Using multimodal fusion techniques, RiskLabs amalgamates these varied data features for comprehensive multi-task financial risk prediction. Empirical experiment results demonstrate RiskLab's effectiveness in forecasting both volatility and variance in financial markets. Through comparative experiments, we demonstrate how different data sources contribute to financial risk assessment and discuss the critical role of LLMs in this context. Our findings not only contribute to the AI in finance application but also open new avenues for applying LLMs in financial risk assessment.

Read more4/12/2024