Factor Augmented Tensor-on-Tensor Neural Networks

0

Sign in to get full access

Overview

- Introduces a novel neural network architecture called Factor Augmented Tensor-on-Tensor Neural Networks (FATT-NN) for modeling high-dimensional data

- Focuses on applications in financial asset management, where datasets are often multi-dimensional tensors

- Proposes techniques to mitigate the challenge of heterogeneity among factor tensors in such datasets

Plain English Explanation

The research paper presents a new type of neural network called Factor Augmented Tensor-on-Tensor Neural Networks (FATT-NN) that is designed to work with complex, high-dimensional datasets, such as those commonly found in financial asset management.

In the financial domain, datasets often have a tensor structure, meaning they have multiple dimensions (e.g., time, asset types, macroeconomic factors). The FATT-NN architecture aims to effectively capture the relationships and interdependencies within these multi-dimensional datasets.

A key challenge addressed by the researchers is the issue of "heterogeneity" among the different factor tensors in the dataset. This refers to the fact that the various factors (e.g., asset types, macroeconomic indicators) may have different statistical properties and patterns. The paper introduces techniques to mitigate this heterogeneity and improve the model's ability to learn from the data.

By using the FATT-NN approach, the researchers hope to enhance the performance of deep learning models in financial applications, such as factor timing asset management and modeling multilayer network interdependence.

Technical Explanation

The FATT-NN architecture combines the strengths of tensor factorization and neural networks to handle high-dimensional, multi-modal data. It incorporates several key components:

-

Tensor Representation: The input data is represented as a multi-dimensional tensor, capturing the complex relationships and interdependencies within the dataset.

-

Factor Augmentation: The model learns a set of "factor tensors" that encode the essential features of the input data. These factor tensors are then used to augment the input, allowing the neural network to better capture the underlying structure.

-

Heterogeneity Mitigation: To address the issue of heterogeneity among the factor tensors, the researchers propose techniques based on Lie group theory and tensor factorization.

-

Tensor-on-Tensor Neural Network: The augmented input tensor is then processed through a neural network architecture specifically designed to handle tensor-valued inputs and outputs.

The researchers evaluate the FATT-NN model on several benchmark datasets, including CAFA-GEOS for global weather forecasting, and demonstrate its superior performance compared to traditional tensor-based methods and deep learning models.

Critical Analysis

The paper presents a novel and promising approach for modeling complex, high-dimensional data using tensor-based neural networks. The researchers have addressed several key challenges, such as the issue of heterogeneity among factor tensors, which is an important consideration in many real-world applications.

However, the paper does not provide a detailed analysis of the computational complexity and training time of the FATT-NN model, which could be an important factor for practical deployment in time-sensitive settings like financial asset management.

Additionally, the paper could have explored the interpretability and explainability of the learned factor tensors and their relationship to the underlying domain knowledge. This could be valuable for gaining a deeper understanding of the model's decision-making process and facilitating trust in the model's outputs.

Further research could also investigate the applicability of the FATT-NN approach to other domains beyond finance, such as high-dimensional data analysis and multilayer network modeling, to assess its broader utility and generalization capabilities.

Conclusion

The Factor Augmented Tensor-on-Tensor Neural Networks (FATT-NN) proposed in this research paper represents a significant advancement in the field of deep learning for high-dimensional, multi-modal data. By effectively capturing the complex relationships and interdependencies within tensor-structured datasets, the FATT-NN model has the potential to drive innovations in financial asset management and other domains involving large, complex datasets.

The techniques introduced to mitigate the challenge of heterogeneity among factor tensors are particularly noteworthy and could have broader applications in tensor-based machine learning. As the research in this area continues to evolve, the FATT-NN approach may become an increasingly valuable tool for researchers and practitioners working with high-dimensional data.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Factor Augmented Tensor-on-Tensor Neural Networks

Guanhao Zhou, Yuefeng Han, Xiufan Yu

This paper studies the prediction task of tensor-on-tensor regression in which both covariates and responses are multi-dimensional arrays (a.k.a., tensors) across time with arbitrary tensor order and data dimension. Existing methods either focused on linear models without accounting for possibly nonlinear relationships between covariates and responses, or directly employed black-box deep learning algorithms that failed to utilize the inherent tensor structure. In this work, we propose a Factor Augmented Tensor-on-Tensor Neural Network (FATTNN) that integrates tensor factor models into deep neural networks. We begin with summarizing and extracting useful predictive information (represented by the ``factor tensor'') from the complex structured tensor covariates, and then proceed with the prediction task using the estimated factor tensor as input of a temporal convolutional neural network. The proposed methods effectively handle nonlinearity between complex data structures, and improve over traditional statistical models and conventional deep learning approaches in both prediction accuracy and computational cost. By leveraging tensor factor models, our proposed methods exploit the underlying latent factor structure to enhance the prediction, and in the meantime, drastically reduce the data dimensionality that speeds up the computation. The empirical performances of our proposed methods are demonstrated via simulation studies and real-world applications to three public datasets. Numerical results show that our proposed algorithms achieve substantial increases in prediction accuracy and significant reductions in computational time compared to benchmark methods.

Read more5/31/2024

0

An Efficient Approach to Regression Problems with Tensor Neural Networks

Yongxin Li, Yifan Wang, Zhongshuo Lin, Hehu Xie

This paper introduces a tensor neural network (TNN) to address nonparametric regression problems, leveraging its distinct sub-network structure to effectively facilitate variable separation and enhance the approximation of complex, high-dimensional functions. The TNN demonstrates superior performance compared to conventional Feed-Forward Networks (FFN) and Radial Basis Function Networks (RBN) in terms of both approximation accuracy and generalization capacity, even with a comparable number of parameters. A significant innovation in our approach is the integration of statistical regression and numerical integration within the TNN framework. This allows for efficient computation of high-dimensional integrals associated with the regression function and provides detailed insights into the underlying data structure. Furthermore, we employ gradient and Laplacian analysis on the regression outputs to identify key dimensions influencing the predictions, thereby guiding the design of subsequent experiments. These advancements make TNN a powerful tool for applications requiring precise high-dimensional data analysis and predictive modeling.

Read more9/16/2024

🤿

0

Application of Deep Learning for Factor Timing in Asset Management

Prabhu Prasad Panda, Maysam Khodayari Gharanchaei, Xilin Chen, Haoshu Lyu

The paper examines the performance of regression models (OLS linear regression, Ridge regression, Random Forest, and Fully-connected Neural Network) on the prediction of CMA (Conservative Minus Aggressive) factor premium and the performance of factor timing investment with them. Out-of-sample R-squared shows that more flexible models have better performance in explaining the variance in factor premium of the unseen period, and the back testing affirms that the factor timing based on more flexible models tends to over perform the ones with linear models. However, for flexible models like neural networks, the optimal weights based on their prediction tend to be unstable, which can lead to high transaction costs and market impacts. We verify that tilting down the rebalance frequency according to the historical optimal rebalancing scheme can help reduce the transaction costs.

Read more4/30/2024

0

Computational and Statistical Guarantees for Tensor-on-Tensor Regression with Tensor Train Decomposition

Zhen Qin, Zhihui Zhu

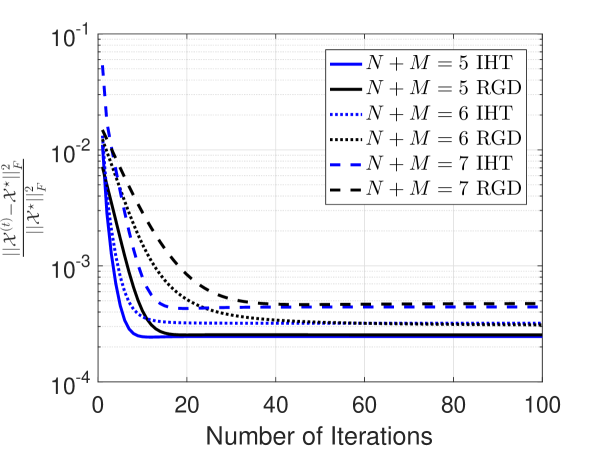

Recently, a tensor-on-tensor (ToT) regression model has been proposed to generalize tensor recovery, encompassing scenarios like scalar-on-tensor regression and tensor-on-vector regression. However, the exponential growth in tensor complexity poses challenges for storage and computation in ToT regression. To overcome this hurdle, tensor decompositions have been introduced, with the tensor train (TT)-based ToT model proving efficient in practice due to reduced memory requirements, enhanced computational efficiency, and decreased sampling complexity. Despite these practical benefits, a disparity exists between theoretical analysis and real-world performance. In this paper, we delve into the theoretical and algorithmic aspects of the TT-based ToT regression model. Assuming the regression operator satisfies the restricted isometry property (RIP), we conduct an error analysis for the solution to a constrained least-squares optimization problem. This analysis includes upper error bound and minimax lower bound, revealing that such error bounds polynomially depend on the order $N+M$. To efficiently find solutions meeting such error bounds, we propose two optimization algorithms: the iterative hard thresholding (IHT) algorithm (employing gradient descent with TT-singular value decomposition (TT-SVD)) and the factorization approach using the Riemannian gradient descent (RGD) algorithm. When RIP is satisfied, spectral initialization facilitates proper initialization, and we establish the linear convergence rate of both IHT and RGD.

Read more6/11/2024