Large-scale Time-Varying Portfolio Optimisation using Graph Attention Networks

0

Sign in to get full access

Overview

- This paper presents a novel approach for large-scale, time-varying portfolio optimization using Graph Attention Networks (GATs).

- The researchers develop a GAT-based model that can effectively capture the complex relationships between financial assets and optimize portfolio returns over time.

- The proposed method outperforms traditional portfolio optimization techniques in extensive experiments on real-world financial data.

Plain English Explanation

When you invest in the stock market, you often try to build a portfolio - a collection of different stocks, bonds, and other assets - that can maximize your returns while minimizing your risk. This is called portfolio optimization.

However, as the financial markets constantly change over time, it can be challenging to optimize your portfolio effectively. The researchers in this paper developed a new approach using a type of artificial intelligence called Graph Attention Networks (GATs).

GATs can model the complex relationships between different financial assets in your portfolio, and how those relationships change over time. This allows the researchers' model to optimize your portfolio more accurately than traditional portfolio optimization techniques, even for very large and complex portfolios.

The key idea is that GATs can pay attention to the most important connections between assets, which helps the model make better decisions about how to allocate your investments. This "attention" mechanism is what gives GATs their power for this type of optimization problem.

Technical Explanation

The researchers propose a Graph Attention Network (GAT)-based model for large-scale, time-varying portfolio optimization. The model takes as input a dynamic financial asset graph, where nodes represent assets and edges capture relationships between them.

The GAT component of the model learns to attend to the most important connections between assets, allowing it to effectively capture the complex, time-varying dependencies in the financial data. This attention mechanism is a key innovation that differentiates the proposed approach from traditional portfolio optimization techniques.

The researchers evaluate their model on extensive experiments using real-world financial data, including daily stock prices and other market information. They compare the performance of their GAT-based optimizer to several baseline methods, and demonstrate that it consistently outperforms the state-of-the-art in terms of portfolio returns, risk, and other key metrics.

Critical Analysis

One potential limitation of the research is that it assumes the availability of a comprehensive financial asset graph, which may not always be the case in practice. The researchers mention that constructing such a graph could be challenging, and may require additional data sources or preprocessing steps.

Additionally, the paper does not explore the interpretability of the attention weights learned by the GAT model. While the attention mechanism is a powerful tool for capturing complex relationships, it can also be difficult to understand the underlying logic behind the model's decisions. Further research may be needed to improve the transparency and explainability of the proposed approach.

Overall, the researchers present a compelling and innovative approach to a critical problem in finance. The use of Graph Attention Networks for large-scale, time-varying portfolio optimization is a significant contribution to the field, and the strong empirical results suggest that the method has the potential for real-world impact.

Conclusion

This paper introduces a novel Graph Attention Network-based model for large-scale, time-varying portfolio optimization. The key innovation is the use of an attention mechanism to effectively capture the complex, evolving relationships between financial assets, which allows the model to outperform traditional portfolio optimization techniques.

The proposed method has the potential to improve investment outcomes for a wide range of financial institutions and individual investors, by providing a more accurate and adaptive approach to portfolio management. As the financial markets continue to evolve, techniques like this that can effectively handle time-varying, high-dimensional data will become increasingly important.

While the research has some limitations, it represents an exciting advance in the application of graph-based deep learning methods to problems in finance and investment management. The findings in this paper may inspire further work exploring the use of attention-based models for other challenges in this domain.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Large-scale Time-Varying Portfolio Optimisation using Graph Attention Networks

Kamesh Korangi, Christophe Mues, Cristi'an Bravo

Apart from assessing individual asset performance, investors in financial markets also need to consider how a set of firms performs collectively as a portfolio. Whereas traditional Markowitz-based mean-variance portfolios are widespread, network-based optimisation techniques have built upon these developments. However, most studies do not contain firms at risk of default and remove any firms that drop off indices over a certain time. This is the first study to incorporate risky firms and use all the firms in portfolio optimisation. We propose and empirically test a novel method that leverages Graph Attention networks (GATs), a subclass of Graph Neural Networks (GNNs). GNNs, as deep learning-based models, can exploit network data to uncover nonlinear relationships. Their ability to handle high-dimensional features and accommodate customised layers for specific purposes makes them particularly appealing for large-scale problems such as mid- and small-cap portfolio optimization. This study utilises 30 years of data on mid-cap firms, creating graphs of firms using distance correlation and the Triangulated Maximally Filtered Graph approach. These graphs are the inputs to a GAT model that we train using custom layers which impose weight and allocation constraints and a loss function derived from the Sharpe ratio, thus directly maximising portfolio risk-adjusted returns. This new model is benchmarked against a network characteristic-based portfolio, a mean variance-based portfolio, and an equal-weighted portfolio. The results show that the portfolio produced by the GAT-based model outperforms all benchmarks and is consistently superior to other strategies over a long period while also being informative of market dynamics.

Read more7/23/2024

0

Multivariate Time-Series Anomaly Detection based on Enhancing Graph Attention Networks with Topological Analysis

Zhe Liu, Xiang Huang, Jingyun Zhang, Zhifeng Hao, Li Sun, Hao Peng

Unsupervised anomaly detection in time series is essential in industrial applications, as it significantly reduces the need for manual intervention. Multivariate time series pose a complex challenge due to their feature and temporal dimensions. Traditional methods use Graph Neural Networks (GNNs) or Transformers to analyze spatial while RNNs to model temporal dependencies. These methods focus narrowly on one dimension or engage in coarse-grained feature extraction, which can be inadequate for large datasets characterized by intricate relationships and dynamic changes. This paper introduces a novel temporal model built on an enhanced Graph Attention Network (GAT) for multivariate time series anomaly detection called TopoGDN. Our model analyzes both time and feature dimensions from a fine-grained perspective. First, we introduce a multi-scale temporal convolution module to extract detailed temporal features. Additionally, we present an augmented GAT to manage complex inter-feature dependencies, which incorporates graph topology into node features across multiple scales, a versatile, plug-and-play enhancement that significantly boosts the performance of GAT. Our experimental results confirm that our approach surpasses the baseline models on four datasets, demonstrating its potential for widespread application in fields requiring robust anomaly detection. The code is available at https://github.com/ljj-cyber/TopoGDN.

Read more8/26/2024

0

Developing An Attention-Based Ensemble Learning Framework for Financial Portfolio Optimisation

Zhenglong Li, Vincent Tam

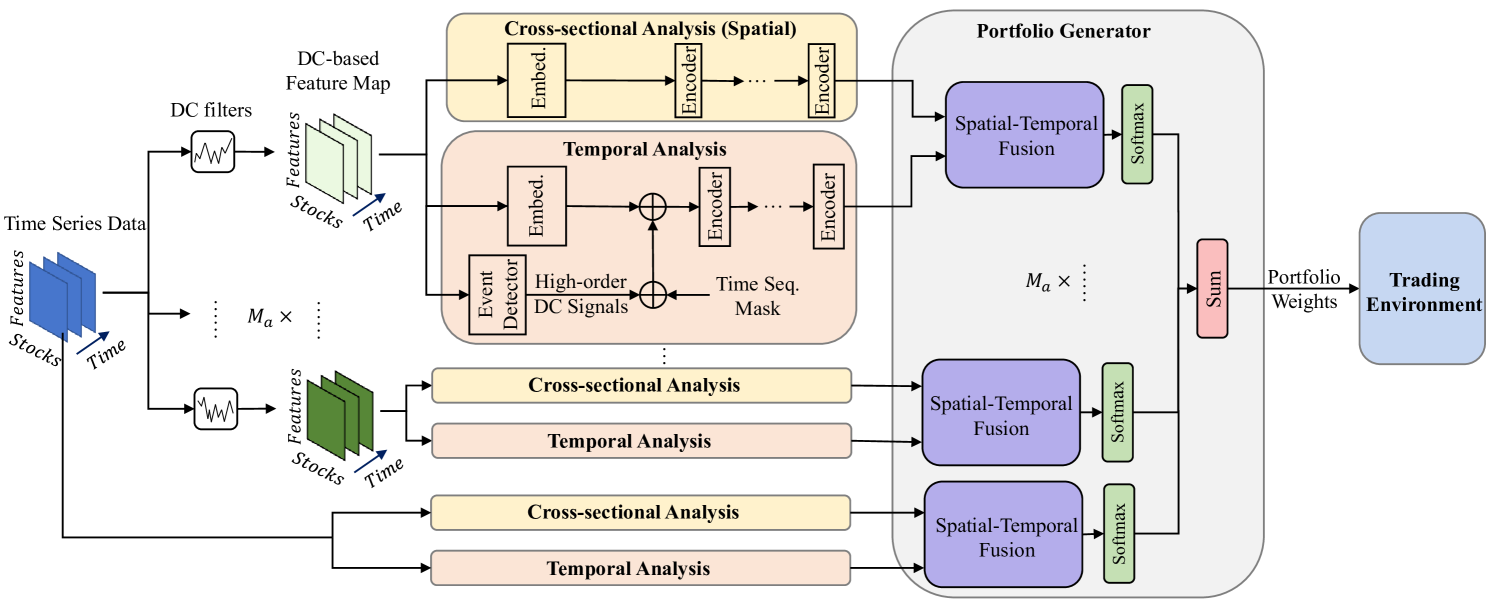

In recent years, deep or reinforcement learning approaches have been applied to optimise investment portfolios through learning the spatial and temporal information under the dynamic financial market. Yet in most cases, the existing approaches may produce biased trading signals based on the conventional price data due to a lot of market noises, which possibly fails to balance the investment returns and risks. Accordingly, a multi-agent and self-adaptive portfolio optimisation framework integrated with attention mechanisms and time series, namely the MASAAT, is proposed in this work in which multiple trading agents are created to observe and analyse the price series and directional change data that recognises the significant changes of asset prices at different levels of granularity for enhancing the signal-to-noise ratio of price series. Afterwards, by reconstructing the tokens of financial data in a sequence, the attention-based cross-sectional analysis module and temporal analysis module of each agent can effectively capture the correlations between assets and the dependencies between time points. Besides, a portfolio generator is integrated into the proposed framework to fuse the spatial-temporal information and then summarise the portfolios suggested by all trading agents to produce a newly ensemble portfolio for reducing biased trading actions and balancing the overall returns and risks. The experimental results clearly demonstrate that the MASAAT framework achieves impressive enhancement when compared with many well-known portfolio optimsation approaches on three challenging data sets of DJIA, S&P 500 and CSI 300. More importantly, our proposal has potential strengths in many possible applications for future study.

Read more4/16/2024

🌐

0

Neighbor Overlay-Induced Graph Attention Network

Tiqiao Wei, Ye Yuan

Graph neural networks (GNNs) have garnered significant attention due to their ability to represent graph data. Among various GNN variants, graph attention network (GAT) stands out since it is able to dynamically learn the importance of different nodes. However, present GATs heavily rely on the smoothed node features to obtain the attention coefficients rather than graph structural information, which fails to provide crucial contextual cues for node representations. To address this issue, this study proposes a neighbor overlay-induced graph attention network (NO-GAT) with the following two-fold ideas: a) learning favorable structural information, i.e., overlaid neighbors, outside the node feature propagation process from an adjacency matrix; b) injecting the information of overlaid neighbors into the node feature propagation process to compute the attention coefficient jointly. Empirical studies on graph benchmark datasets indicate that the proposed NO-GAT consistently outperforms state-of-the-art models.

Read more8/19/2024