On-line conformalized neural networks ensembles for probabilistic forecasting of day-ahead electricity prices

2404.02722

0

0

Abstract

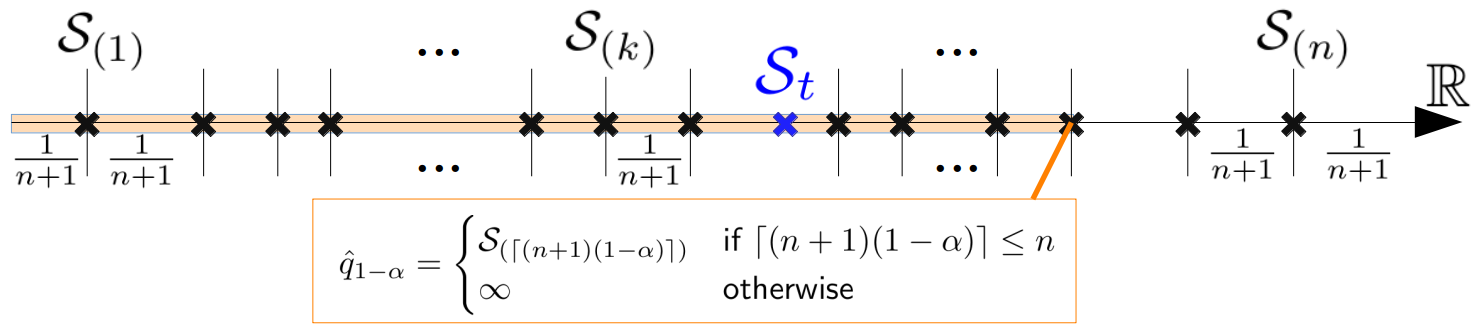

Probabilistic electricity price forecasting (PEPF) is subject of increasing interest, following the demand for proper quantification of prediction uncertainty, to support the operation in complex power markets with increasing share of renewable generation. Distributional neural networks ensembles have been recently shown to outperform state of the art PEPF benchmarks. Still, they require critical reliability enhancements, as fail to pass the coverage tests at various steps on the prediction horizon. In this work, we propose a novel approach to PEPF, extending the state of the art neural networks ensembles based methods through conformal inference based techniques, deployed within an on-line recalibration procedure. Experiments have been conducted on multiple market regions, achieving day-ahead forecasts with improved hourly coverage and stable probabilistic scores.

Create account to get full access

Overview

- This paper proposes an online conformalized neural network ensemble for probabilistic forecasting of day-ahead electricity prices.

- The approach combines multiple neural network models to provide probabilistic predictions, with a conformalization step to calibrate the prediction intervals.

- The researchers evaluate the method on real-world electricity price data and compare it to other forecasting techniques.

Plain English Explanation

The paper describes a new way to predict future electricity prices using a collection of machine learning models. Electricity prices can be difficult to forecast accurately, as they can be influenced by many complex factors like weather, demand, and energy supply.

The researchers' approach uses multiple neural network models working together as an "ensemble." Each individual model makes its own prediction, and then a special mathematical technique called "conformalization" is used to combine the predictions into a range or interval that captures the uncertainty. This provides not just a single forecast, but a probabilistic estimate of the likely future price.

The key idea is that by having multiple models contribute to the forecast, and then calibrating the results, the researchers can produce more reliable and trustworthy predictions than a single model alone. This could be very valuable for electricity grid operators, energy traders, and consumers who need to plan ahead and manage price volatility.

Technical Explanation

The paper introduces an online conformalized neural network ensemble (OCNNE) for probabilistic forecasting of day-ahead electricity prices. The approach combines multiple neural network models into an ensemble, where each model makes its own price prediction. A conformal prediction technique is then used to calibrate the prediction intervals to ensure they have the desired coverage probability.

The ensemble consists of multiple neural networks with different architectures and hyperparameters, trained on the same historical electricity price data. During online deployment, the ensemble generates multiple point forecasts, which are then transformed into probabilistic forecasts using the conformal prediction framework. This allows the model to provide not just a single point estimate, but a full probability distribution of the likely price outcomes.

The researchers evaluate the OCNNE approach on real-world electricity price datasets, comparing its performance to various benchmark models like ARIMA and single neural networks. The results show that the ensemble method outperforms the alternatives in terms of accuracy, calibration, and other key metrics for probabilistic forecasting.

Critical Analysis

The paper provides a thorough technical description of the OCNNE approach and demonstrates its effectiveness on realistic electricity price data. However, the authors acknowledge some limitations. The conformalization step relies on certain statistical assumptions that may not always hold in practice. Additionally, the performance of the ensemble is dependent on the quality and diversity of the individual neural network models, which requires careful model selection and tuning.

An interesting area for further research would be investigating ways to dynamically adapt the ensemble composition and weighting to changing market conditions. This could potentially improve the model's ability to capture non-stationary patterns in electricity prices.

Another limitation is that the evaluation is focused on a single application domain - day-ahead electricity prices. It would be valuable to see how the OCNNE approach generalizes to other forecasting problems, such as longer-term electricity price forecasting or forecasting in other energy markets.

Conclusion

Overall, this paper presents a promising approach for probabilistic forecasting of electricity prices using an online conformalized neural network ensemble. The combination of multiple models and calibration of prediction intervals seems to offer advantages over simpler forecasting methods. The technical details and empirical results suggest this technique could be a valuable tool for grid operators, energy traders, and policymakers who need to understand and manage electricity price uncertainty.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

Conformal Prediction for Stochastic Decision-Making of PV Power in Electricity Markets

Yvet Renkema, Nico Brinkel, Tarek Alskaif

0

0

This paper studies the use of conformal prediction (CP), an emerging probabilistic forecasting method, for day-ahead photovoltaic power predictions to enhance participation in electricity markets. First, machine learning models are used to construct point predictions. Thereafter, several variants of CP are implemented to quantify the uncertainty of those predictions by creating CP intervals and cumulative distribution functions. Optimal quantity bids for the electricity market are estimated using several bidding strategies under uncertainty, namely: trust-the-forecast, worst-case, Newsvendor and expected utility maximization (EUM). Results show that CP in combination with k-nearest neighbors and/or Mondrian binning outperforms its corresponding linear quantile regressors. Using CP in combination with certain bidding strategies can yield high profit with minimal energy imbalance. In concrete, using conformal predictive systems with k-nearest neighbors and Mondrian binning after random forest regression yields the best profit and imbalance regardless of the decision-making strategy. Combining this uncertainty quantification method with the EUM strategy with conditional value at risk (CVaR) can yield up to 93% of the potential profit with minimal energy imbalance.

4/1/2024

Forecasting Electricity Market Signals via Generative AI

Xinyi Wang, Qing Zhao, Lang Tong

0

0

This paper presents a generative artificial intelligence approach to probabilistic forecasting of electricity market signals, such as real-time locational marginal prices and area control error signals. Inspired by the Wiener-Kallianpur innovation representation of nonparametric time series, we propose a weak innovation autoencoder architecture and a novel deep learning algorithm that extracts the canonical independent and identically distributed innovation sequence of the time series, from which samples of future time series are generated. The validity of the proposed approach is established by proving that, under ideal training conditions, the generated samples have the same conditional probability distribution as that of the ground truth. Three applications involving highly dynamic and volatile time series in real-time market operations are considered: (i) locational marginal price forecasting for self-scheduled resources such as battery storage participants, (ii) interregional price spread forecasting for virtual bidders in interchange markets, and (iii) area control error forecasting for frequency regulations. Numerical studies based on market data from multiple independent system operators demonstrate the superior performance of the proposed generative forecaster over leading classical and modern machine learning techniques under both probabilistic and point forecasting metrics.

7/1/2024

🧠

Probabilistic forecasting of power system imbalance using neural network-based ensembles

Jonas Van Gompel, Bert Claessens, Chris Develder

0

0

Keeping the balance between electricity generation and consumption is becoming increasingly challenging and costly, mainly due to the rising share of renewables, electric vehicles and heat pumps and electrification of industrial processes. Accurate imbalance forecasts, along with reliable uncertainty estimations, enable transmission system operators (TSOs) to dispatch appropriate reserve volumes, reducing balancing costs. Further, market parties can use these probabilistic forecasts to design strategies that exploit asset flexibility to help balance the grid, generating revenue with known risks. Despite its importance, literature regarding system imbalance (SI) forecasting is limited. Further, existing methods do not focus on situations with high imbalance magnitude, which are crucial to forecast accurately for both TSOs and market parties. Hence, we propose an ensemble of C-VSNs, which are our adaptation of variable selection networks (VSNs). Each minute, our model predicts the imbalance of the current and upcoming two quarter-hours, along with uncertainty estimations on these forecasts. We evaluate our approach by forecasting the imbalance of Belgium, where high imbalance magnitude is defined as $|$SI$| > 500,$MW (occurs 1.3% of the time in Belgium). For high imbalance magnitude situations, our model outperforms the state-of-the-art by 23.4% (in terms of continuous ranked probability score (CRPS), which evaluates probabilistic forecasts), while also attaining a 6.5% improvement in overall CRPS. Similar improvements are achieved in terms of root-mean-squared error. Additionally, we developed a fine-tuning methodology to effectively include new inputs with limited history in our model. This work was performed in collaboration with Elia (the Belgian TSO) to further improve their imbalance forecasts, demonstrating the relevance of our work.

4/24/2024

⚙️

An adaptive standardisation methodology for Day-Ahead electricity price forecasting

Carlos Sebasti'an, Carlos E. Gonz'alez-Guill'en, Jes'us Juan

0

0

The study of Day-Ahead prices in the electricity market is one of the most popular problems in time series forecasting. Previous research has focused on employing increasingly complex learning algorithms to capture the sophisticated dynamics of the market. However, there is a threshold where increased complexity fails to yield substantial improvements. In this work, we propose an alternative approach by introducing an adaptive standardisation to mitigate the effects of dataset shifts that commonly occur in the market. By doing so, learning algorithms can prioritize uncovering the true relationship between the target variable and the explanatory variables. We investigate five distinct markets, including two novel datasets, previously unexplored in the literature. These datasets provide a more realistic representation of the current market context, that conventional datasets do not show. The results demonstrate a significant improvement across all five markets using the widely accepted learning algorithms in the literature (LEAR and DNN). In particular, the combination of the proposed methodology with the methodology previously presented in the literature obtains the best results. This significant advancement unveils new lines of research in this field, highlighting the potential of adaptive transformations in enhancing the performance of forecasting models.

4/29/2024