Conformal Prediction for Stochastic Decision-Making of PV Power in Electricity Markets

2403.20149

0

0

Abstract

This paper studies the use of conformal prediction (CP), an emerging probabilistic forecasting method, for day-ahead photovoltaic power predictions to enhance participation in electricity markets. First, machine learning models are used to construct point predictions. Thereafter, several variants of CP are implemented to quantify the uncertainty of those predictions by creating CP intervals and cumulative distribution functions. Optimal quantity bids for the electricity market are estimated using several bidding strategies under uncertainty, namely: trust-the-forecast, worst-case, Newsvendor and expected utility maximization (EUM). Results show that CP in combination with k-nearest neighbors and/or Mondrian binning outperforms its corresponding linear quantile regressors. Using CP in combination with certain bidding strategies can yield high profit with minimal energy imbalance. In concrete, using conformal predictive systems with k-nearest neighbors and Mondrian binning after random forest regression yields the best profit and imbalance regardless of the decision-making strategy. Combining this uncertainty quantification method with the EUM strategy with conditional value at risk (CVaR) can yield up to 93% of the potential profit with minimal energy imbalance.

Create account to get full access

Introduction

The paper discusses the use of conformal prediction (CP) to improve decision-making for solar photovoltaic (PV) power suppliers in the day-ahead electricity market (DAM). In the DAM, suppliers offer a specific volume of electricity at a minimum price, while buyers bid a volume at a maximum price. Deviations from accepted bids in real-time result in high imbalance costs. Accurate PV power forecasts are crucial for suppliers with PV assets and for grid operators to manage network congestion.

The paper proposes a framework that combines point prediction models for PV power with CP to quantify the uncertainty of the predictions. Several bidding strategies, including Trust-the-forecast, worst-case, Newsvendor, and expected utility maximization, are then employed to facilitate decision-making for PV power suppliers in the DAM. The goal is to determine the optimal quantity a supplier should offer to maximize profit while minimizing energy imbalance.

The framework is evaluated using actual weather and energy market data from the Netherlands. The main contributions of the paper are the proposal of a novel framework using CP to aid decision-making for PV power market participants, and the development, application, and evaluation of various combinations of CP with bidding strategies.

Methods

The paper discusses the limitations of classical machine learning models in properly estimating prediction uncertainty, and how Conformal Prediction (CP) can address this issue. CP is a relatively new methodology that has seen growing interest in recent years, with publications increasing from 0 in 2006 to 73 in 2022.

CP transforms point predictions into uncertainty intervals without requiring assumptions about the data distribution. The uncertainty intervals provided by CP offer a probabilistic guarantee of covering the true outcome, based on a user-specified error rate.

The paper proposes a framework to determine day-ahead market (DAM) bids for photovoltaic (PV) generation using a CP method. The framework involves three steps: making point predictions for PV generation, quantifying the uncertainty of these predictions, and then determining the optimal DAM bids.

This study examines three models for making PV power point predictions: simple and multiple linear regression (SLR & MLR) and random forest regression (RFR). Linear and tree-based models are selected as they have shown good performance for forecasting electricity consumption and PV power.

Before making point predictions, the input data is split into training, calibration and test sets. The training set is used to determine the optimal predictor feature set and tune hyperparameters. The calibration and test sets are then predicted with the fitted model.

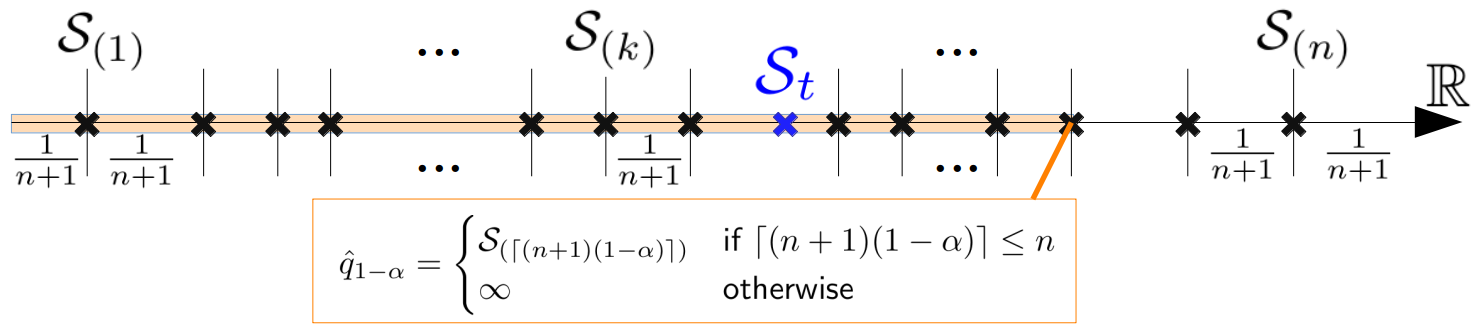

For uncertainty quantification, the study considers various conformal prediction (CP) methods, including simple and multiple linear quantile regression (SLQR & MLQR) as benchmarks. The basic CP method guarantees marginal coverage but not conditional coverage. CP with uncertainty scalars and CP with Mondrian binning are used to increase adaptivity and approximate conditional coverage. Conformal predictive systems (CPS) are also explored, which output conformal predictive distributions instead of just intervals.

Several bidding strategies are then applied to the test dataset to determine optimal quantity bids for the day-ahead market (DAM). These include "trust-the-forecast", "worst-case", "newsvendor", and "expected utility maximization" (EUM) strategies, with and without conditional value at risk (CVaR) considerations. A "perfect information" reference case is also included.

Data inputs and simulation outline

The paper applies the forecasting methodologies outlined in Section II to an open-source dataset of power measurements from 175 PV systems in Utrecht, the Netherlands. The dataset covers January 2014 to December 2017 at a one-minute resolution, which is then converted to average hourly values. The data is split into training (2014-2015), calibration (2016), and test (2017) sets.

Various predictor variables are considered, including temporal and physical properties like hour of day, clear sky irradiance, and solar angles, as well as weather forecast data. Forward subset selection determines the optimal predictor variables for the MLR and SLR models. The hyperparameter tuning for the RFR model finds that 375 trees with a maximum of 3 features per tree performs best.

For the optimization strategies, the paper uses real-world day-ahead market (DAM) and real-time market (RTM) prices for the Netherlands. The RTM prices are derived from the DAM prices and historical imbalance price deltas, which are clustered into 20 scenarios using k-means. The EUM models consider 99 PV power scenarios per timestep.

V Results

The authors evaluated the performance of several point prediction models and uncertainty quantification methods for predicting photovoltaic (PV) power generation. The key findings are:

Point Prediction Models: The random forest regressor (RFR) had the best performance, followed by multiple linear regression (MLR) and single linear regression (SLR).

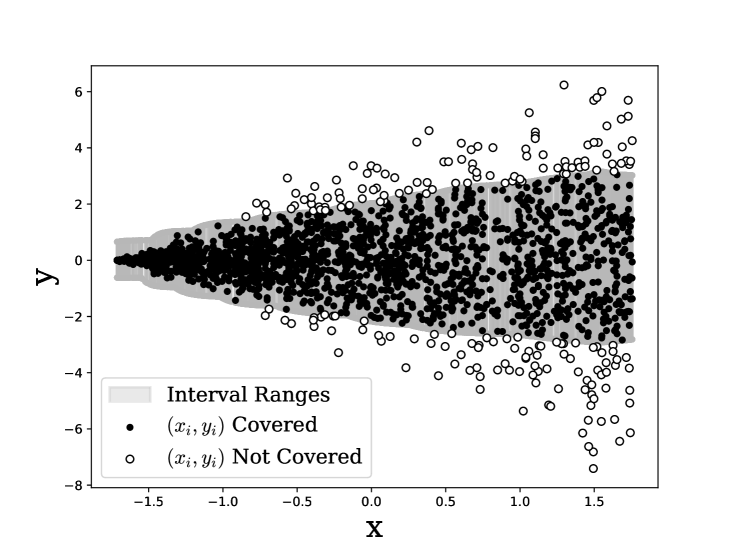

Uncertainty Quantification: The authors assessed confidence prediction (CP) and conformal prediction with shifts (CPS) methods using the weighted interval score (WIS) metric. The more advanced CP methods (M2-M5) outperformed the basic CP method (M1) and the linear quantile regression (LQR) reference. The best-performing model was the CP method with k-nearest neighbors and Mondrian binning (M3).

Bidding Strategies: The authors evaluated different bidding strategies using the best-performing point prediction and uncertainty quantification models. The "trust-the-forecast" strategy achieved 92.4% of the maximum profit with perfect information. The CPS methods outperformed the CP methods for the Newsvendor and expected utility maximization (EUM) strategies, despite having a higher WIS, due to the added flexibility of CPS.

Discussion

The paper discusses the methodological assumptions and limitations of the study, as well as the implications of the work. The authors note that several simplifications were necessary due to the extensive scope of the study. For example, they assumed perfect knowledge of DAM prices and accurate representation of RTM price clusters. The analysis was limited to linear and tree-based point prediction models, with a restricted number of RTM price clusters, PV scenarios, and constraint percentages for the Newsvendor strategy. The feature selection and parameter tuning steps also involved simplifications.

Despite these simplifications, the authors are confident that the overall trends are accurately portrayed. Future research could explore more complex models and investigate the impact of the simplifications. Additionally, the intraday market could be incorporated, as it provides market participants opportunities to correct forecasting errors and potentially lead to different bidding strategies.

When interpreting the results, it is important to consider the aggregation steps that reduce the number of extreme values, particularly the impact on CVaR, which functions well for extreme scenarios. The preferred method may differ based on the energy supplier's risk aversion and prioritization of profit versus imbalance. Finally, the framework is limited to quantity bids and does not include a proposed price bid, which should be addressed before implementation.

Conclusions and Future Work

This paper proposes a framework that leverages a probabilistic forecasting method called Conformal Prediction (CP) to enhance decision-making in electricity markets. The framework first generates day-ahead point predictions of photovoltaic (PV) power. It then uses several linear quantile regression (LQR) and CP methods to quantify the uncertainty of the point predictions. Finally, the prediction intervals and cumulative prediction distribution (CPD) are used as input for various decision-making strategies to determine the day-ahead market (DAM) quantity bid under uncertainty.

The key findings are:

- CP methods outperform other uncertainty quantification methods, such as linear quantile regression.

- The CP method using k-nearest neighbors and binning performs best on both profit and imbalance for almost all considered market bidding strategies.

- For high-profit strategies, the Expected Utility Maximization (EUM) strategy with Conditional Value-at-Risk (CVaR) is recommended.

- For lower imbalance, the Newsvendor strategy with a 10% constraint in the decision space should be used.

- Incorporating intraday markets and further exploring the EUM strategy with CVaR could further improve the decision-making strategies.

Appendix A Problem formulation EUM strategy

This paper presents two optimization models for a PV power plant bidding in the day-ahead and real-time electricity markets.

The first model, referred to as A-A EUM (without constraints), aims to maximize the expected profit by optimizing the bid size at each time step. The objective function includes the revenue from day-ahead sales and the penalties/payments from real-time regulation. The model is subject to constraints on the surplus and deficit between the bid and actual PV generation.

The second model, A-B EUM (with CVaR), combines the expected profit with the Conditional Value-at-Risk (CVaR) as the objective function. This model introduces additional constraints to control the risk by limiting the minimum and maximum values of the auxiliary variable σ. The CVaR is calculated based on the profit distributions across scenarios.

Both models restrict the bid size to be between 0 and 1 (due to normalization). The key parameters in the models include the day-ahead market price, real-time regulation prices, PV generation predictions, and probabilities of PV scenarios.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

🔮

An Information Theoretic Perspective on Conformal Prediction

Alvaro H. C. Correia, Fabio Valerio Massoli, Christos Louizos, Arash Behboodi

0

0

Conformal Prediction (CP) is a distribution-free uncertainty estimation framework that constructs prediction sets guaranteed to contain the true answer with a user-specified probability. Intuitively, the size of the prediction set encodes a general notion of uncertainty, with larger sets associated with higher degrees of uncertainty. In this work, we leverage information theory to connect conformal prediction to other notions of uncertainty. More precisely, we prove three different ways to upper bound the intrinsic uncertainty, as described by the conditional entropy of the target variable given the inputs, by combining CP with information theoretical inequalities. Moreover, we demonstrate two direct and useful applications of such connection between conformal prediction and information theory: (i) more principled and effective conformal training objectives that generalize previous approaches and enable end-to-end training of machine learning models from scratch, and (ii) a natural mechanism to incorporate side information into conformal prediction. We empirically validate both applications in centralized and federated learning settings, showing our theoretical results translate to lower inefficiency (average prediction set size) for popular CP methods.

6/27/2024

Verifiably Robust Conformal Prediction

Linus Jeary, Tom Kuipers, Mehran Hosseini, Nicola Paoletti

0

0

Conformal Prediction (CP) is a popular uncertainty quantification method that provides distribution-free, statistically valid prediction sets, assuming that training and test data are exchangeable. In such a case, CP's prediction sets are guaranteed to cover the (unknown) true test output with a user-specified probability. Nevertheless, this guarantee is violated when the data is subjected to adversarial attacks, which often result in a significant loss of coverage. Recently, several approaches have been put forward to recover CP guarantees in this setting. These approaches leverage variations of randomised smoothing to produce conservative sets which account for the effect of the adversarial perturbations. They are, however, limited in that they only support $ell^2$-bounded perturbations and classification tasks. This paper introduces VRCP (Verifiably Robust Conformal Prediction), a new framework that leverages recent neural network verification methods to recover coverage guarantees under adversarial attacks. Our VRCP method is the first to support perturbations bounded by arbitrary norms including $ell^1$, $ell^2$, and $ell^infty$, as well as regression tasks. We evaluate and compare our approach on image classification tasks (CIFAR10, CIFAR100, and TinyImageNet) and regression tasks for deep reinforcement learning environments. In every case, VRCP achieves above nominal coverage and yields significantly more efficient and informative prediction regions than the SotA.

6/7/2024

On-line conformalized neural networks ensembles for probabilistic forecasting of day-ahead electricity prices

Alessandro Brusaferri, Andrea Ballarino, Luigi Grossi, Fabrizio Laurini

0

0

Probabilistic electricity price forecasting (PEPF) is subject of increasing interest, following the demand for proper quantification of prediction uncertainty, to support the operation in complex power markets with increasing share of renewable generation. Distributional neural networks ensembles have been recently shown to outperform state of the art PEPF benchmarks. Still, they require critical reliability enhancements, as fail to pass the coverage tests at various steps on the prediction horizon. In this work, we propose a novel approach to PEPF, extending the state of the art neural networks ensembles based methods through conformal inference based techniques, deployed within an on-line recalibration procedure. Experiments have been conducted on multiple market regions, achieving day-ahead forecasts with improved hourly coverage and stable probabilistic scores.

6/11/2024

Conformal Prediction via Regression-as-Classification

Etash Guha, Shlok Natarajan, Thomas Mollenhoff, Mohammad Emtiyaz Khan, Eugene Ndiaye

0

0

Conformal prediction (CP) for regression can be challenging, especially when the output distribution is heteroscedastic, multimodal, or skewed. Some of the issues can be addressed by estimating a distribution over the output, but in reality, such approaches can be sensitive to estimation error and yield unstable intervals.~Here, we circumvent the challenges by converting regression to a classification problem and then use CP for classification to obtain CP sets for regression.~To preserve the ordering of the continuous-output space, we design a new loss function and make necessary modifications to the CP classification techniques.~Empirical results on many benchmarks shows that this simple approach gives surprisingly good results on many practical problems.

4/15/2024