MGCP: A Multi-Grained Correlation based Prediction Network for Multivariate Time Series

0

Sign in to get full access

Overview

• This paper introduces MGCP, a novel Multi-Grained Correlation based Prediction network for forecasting multivariate time series.

• MGCP leverages multi-scale temporal features and cross-feature correlations to improve prediction accuracy over state-of-the-art models.

• The authors evaluate MGCP on several benchmark datasets and demonstrate its superior performance compared to competing methods.

Plain English Explanation

MGCP is a machine learning model designed to predict future values in complex datasets with multiple related variables changing over time, known as multivariate time series.

Rather than looking at the variables in isolation, MGCP examines how the different variables in the dataset are correlated with and influence each other at both short-term and long-term timescales. This allows it to capture richer patterns in the data and make more accurate forecasts.

For example, imagine trying to predict future stock prices. MGCP would look at not just the history of each individual stock, but also how the different stocks are related to each other and how those relationships change over time. This gives it a more holistic understanding of the market dynamics to improve its forecasting ability.

The key innovation of MGCP is its multi-grained architecture that can extract features at multiple temporal resolutions. This enables it to model both short-term fluctuations and long-term trends in the data, leading to better overall predictions.

Technical Explanation

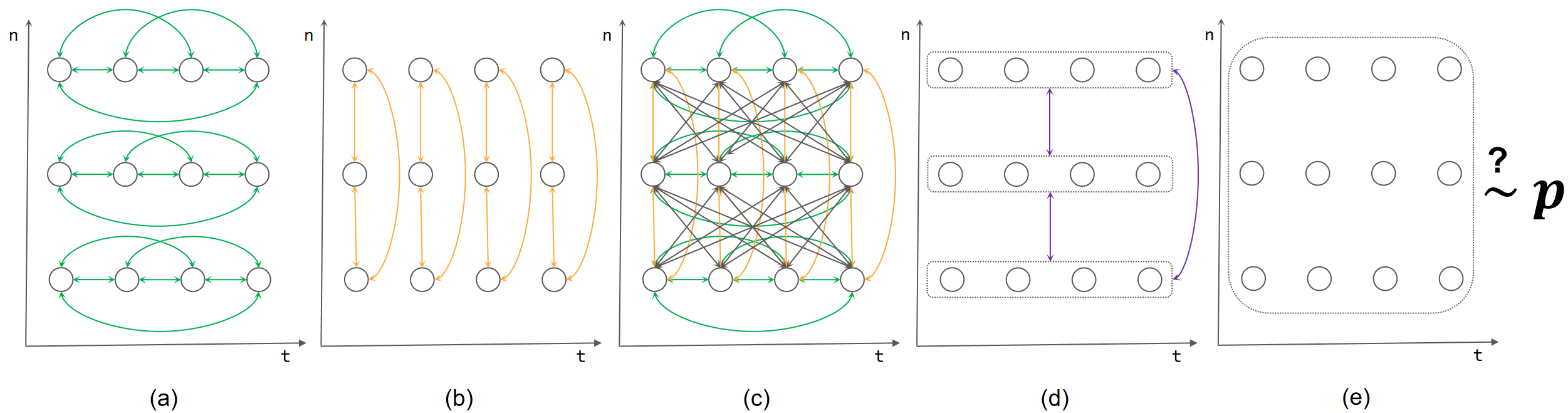

MGCP is a neural network-based model that learns to forecast multivariate time series by jointly capturing multi-scale temporal features and cross-feature correlations.

The core of the architecture is a Multi-Grained Correlation Encoder (MGCE) module, which extracts features at different time granularities using parallel convolutional layers with varying dilation rates. This allows the model to learn both short-term patterns and long-term dependencies in the data.

The extracted features are then passed through a Correlation Attention module, which computes the correlations between the variables at each time step. This correlation information is used to guide the final prediction, helping the model account for the complex interdependencies in the multivariate time series.

The authors evaluate MGCP on several standard benchmarks for multivariate time series forecasting, including <a href="https://aimodels.fyi/papers/arxiv/forecastgrapher-redefining-multivariate-time-series-forecasting-graph">ForecastGrapher</a>, <a href="https://aimodels.fyi/papers/arxiv/context-neural-networks-scalable-multivariate-model-time">ContextNet</a>, <a href="https://aimodels.fyi/papers/arxiv/deephgnn-study-graph-neural-network-based-forecasting">DeepHGNN</a>, and <a href="https://aimodels.fyi/papers/arxiv/dgcformer-deep-graph-clustering-transformer-multivariate-time">DGCFormer</a>. The results show that MGCP outperforms these state-of-the-art models across a variety of metrics, demonstrating the effectiveness of its multi-grained correlation modeling approach.

Critical Analysis

The paper provides a thorough evaluation of MGCP and thoughtfully discusses several limitations and future research directions.

One potential concern is the computational complexity of the multi-grained feature extraction and correlation attention mechanisms, which could make the model challenging to deploy in real-world scenarios with strict latency requirements. The authors acknowledge this and suggest exploring ways to make the model more efficient.

Additionally, the paper primarily evaluates MGCP on standard benchmark datasets, which may not fully capture the diversity of real-world multivariate time series problems. Further testing on a broader range of datasets, including those with <a href="https://aimodels.fyi/papers/arxiv/adaptive-extraction-network-multivariate-long-sequence-time">long sequences</a> or complex temporal dependencies, could help validate the model's broader applicability.

Overall, the authors have made a compelling case for the effectiveness of MGCP and have laid the groundwork for future research on improved multivariate time series forecasting techniques.

Conclusion

The MGCP model introduced in this paper represents a significant advance in multivariate time series forecasting. By jointly capturing multi-scale temporal features and cross-feature correlations, it is able to outperform state-of-the-art models on a range of benchmark datasets.

This work highlights the importance of considering the complex interdependencies between variables when making predictions, rather than treating them in isolation. The multi-grained architecture and correlation attention mechanisms developed in MGCP provide a powerful framework for leveraging these relationships to improve forecasting accuracy.

As multivariate time series data becomes increasingly prevalent in fields like finance, healthcare, and climate science, models like MGCP will be crucial for extracting insights and making accurate predictions. Further research and development in this area could lead to transformative applications that benefit society as a whole.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

MGCP: A Multi-Grained Correlation based Prediction Network for Multivariate Time Series

Zhicheng Chen, Xi Xiao, Ke Xu, Zhong Zhang, Yu Rong, Qing Li, Guojun Gan, Zhiqiang Xu, Peilin Zhao

Multivariate time series prediction is widely used in daily life, which poses significant challenges due to the complex correlations that exist at multi-grained levels. Unfortunately, the majority of current time series prediction models fail to simultaneously learn the correlations of multivariate time series at multi-grained levels, resulting in suboptimal performance. To address this, we propose a Multi-Grained Correlations-based Prediction (MGCP) Network, which simultaneously considers the correlations at three granularity levels to enhance prediction performance. Specifically, MGCP utilizes Adaptive Fourier Neural Operators and Graph Convolutional Networks to learn the global spatiotemporal correlations and inter-series correlations, enabling the extraction of potential features from multivariate time series at fine-grained and medium-grained levels. Additionally, MGCP employs adversarial training with an attention mechanism-based predictor and conditional discriminator to optimize prediction results at coarse-grained level, ensuring high fidelity between the generated forecast results and the actual data distribution. Finally, we compare MGCP with several state-of-the-art time series prediction algorithms on real-world benchmark datasets, and our results demonstrate the generality and effectiveness of the proposed model.

Read more5/31/2024

0

TCGPN: Temporal-Correlation Graph Pre-trained Network for Stock Forecasting

Wenbo Yan, Ying Tan

Recently, the incorporation of both temporal features and the correlation across time series has become an effective approach in time series prediction. Spatio-Temporal Graph Neural Networks (STGNNs) demonstrate good performance on many Temporal-correlation Forecasting Problem. However, when applied to tasks lacking periodicity, such as stock data prediction, the effectiveness and robustness of STGNNs are found to be unsatisfactory. And STGNNs are limited by memory savings so that cannot handle problems with a large number of nodes. In this paper, we propose a novel approach called the Temporal-Correlation Graph Pre-trained Network (TCGPN) to address these limitations. TCGPN utilize Temporal-correlation fusion encoder to get a mixed representation and pre-training method with carefully designed temporal and correlation pre-training tasks. Entire structure is independent of the number and order of nodes, so better results can be obtained through various data enhancements. And memory consumption during training can be significantly reduced through multiple sampling. Experiments are conducted on real stock market data sets CSI300 and CSI500 that exhibit minimal periodicity. We fine-tune a simple MLP in downstream tasks and achieve state-of-the-art results, validating the capability to capture more robust temporal correlation patterns.

Read more7/29/2024

0

ForecastGrapher: Redefining Multivariate Time Series Forecasting with Graph Neural Networks

Wanlin Cai, Kun Wang, Hao Wu, Xiaoxu Chen, Yuankai Wu

The challenge of effectively learning inter-series correlations for multivariate time series forecasting remains a substantial and unresolved problem. Traditional deep learning models, which are largely dependent on the Transformer paradigm for modeling long sequences, often fail to integrate information from multiple time series into a coherent and universally applicable model. To bridge this gap, our paper presents ForecastGrapher, a framework reconceptualizes multivariate time series forecasting as a node regression task, providing a unique avenue for capturing the intricate temporal dynamics and inter-series correlations. Our approach is underpinned by three pivotal steps: firstly, generating custom node embeddings to reflect the temporal variations within each series; secondly, constructing an adaptive adjacency matrix to encode the inter-series correlations; and thirdly, augmenting the GNNs' expressive power by diversifying the node feature distribution. To enhance this expressive power, we introduce the Group Feature Convolution GNN (GFC-GNN). This model employs a learnable scaler to segment node features into multiple groups and applies one-dimensional convolutions with different kernel lengths to each group prior to the aggregation phase. Consequently, the GFC-GNN method enriches the diversity of node feature distribution in a fully end-to-end fashion. Through extensive experiments and ablation studies, we show that ForecastGrapher surpasses strong baselines and leading published techniques in the domain of multivariate time series forecasting.

Read more5/29/2024

0

Causally-Aware Spatio-Temporal Multi-Graph Convolution Network for Accurate and Reliable Traffic Prediction

Pingping Dong, Xiao-Lin Wang, Indranil Bose, Kam K. H. Ng, Xiaoning Zhang, Xiaoge Zhang

Accurate and reliable prediction has profound implications to a wide range of applications. In this study, we focus on an instance of spatio-temporal learning problem--traffic prediction--to demonstrate an advanced deep learning model developed for making accurate and reliable forecast. Despite the significant progress in traffic prediction, limited studies have incorporated both explicit and implicit traffic patterns simultaneously to improve prediction performance. Meanwhile, the variability nature of traffic states necessitates quantifying the uncertainty of model predictions in a statistically principled way; however, extant studies offer no provable guarantee on the statistical validity of confidence intervals in reflecting its actual likelihood of containing the ground truth. In this paper, we propose an end-to-end traffic prediction framework that leverages three primary components to generate accurate and reliable traffic predictions: dynamic causal structure learning for discovering implicit traffic patterns from massive traffic data, causally-aware spatio-temporal multi-graph convolution network (CASTMGCN) for learning spatio-temporal dependencies, and conformal prediction for uncertainty quantification. CASTMGCN fuses several graphs that characterize different important aspects of traffic networks and an auxiliary graph that captures the effect of exogenous factors on the road network. On this basis, a conformal prediction approach tailored to spatio-temporal data is further developed for quantifying the uncertainty in node-wise traffic predictions over varying prediction horizons. Experimental results on two real-world traffic datasets demonstrate that the proposed method outperforms several state-of-the-art models in prediction accuracy; moreover, it generates more efficient prediction regions than other methods while strictly satisfying the statistical validity in coverage.

Read more8/27/2024