Multi-Knowledge Fusion Network for Time Series Representation Learning

0

Sign in to get full access

Overview

- This paper proposes a Multi-Knowledge Fusion Network (MKFN) for learning representations of time series data.

- MKFN integrates multiple knowledge sources, including statistical, semantic, and temporal information, to capture comprehensive features of the input time series.

- The authors demonstrate the effectiveness of MKFN on several benchmark datasets for time series classification and forecasting tasks.

Plain English Explanation

The paper introduces a new model called the Multi-Knowledge Fusion Network (MKFN) that can learn useful representations from time series data. Time series data refers to measurements or observations collected over time, such as stock prices, weather patterns, or sensor readings.

The key idea behind MKFN is to combine multiple types of knowledge about the time series, including statistical, semantic, and temporal information. By integrating these diverse knowledge sources, the model can capture a more comprehensive understanding of the underlying patterns in the time series data.

For example, the statistical knowledge might reveal trends or seasonality in the data, the semantic knowledge could provide contextual information about the variables being measured, and the temporal knowledge could highlight dependencies between different time points. MKFN is designed to learn from all of these aspects of the data, rather than relying on just one type of information.

The authors test MKFN on several standard benchmarks for time series classification and forecasting tasks, and show that it outperforms other state-of-the-art models. This suggests that the multi-knowledge fusion approach is an effective way to learn powerful representations from time series data, which can then be used for a variety of downstream applications.

Technical Explanation

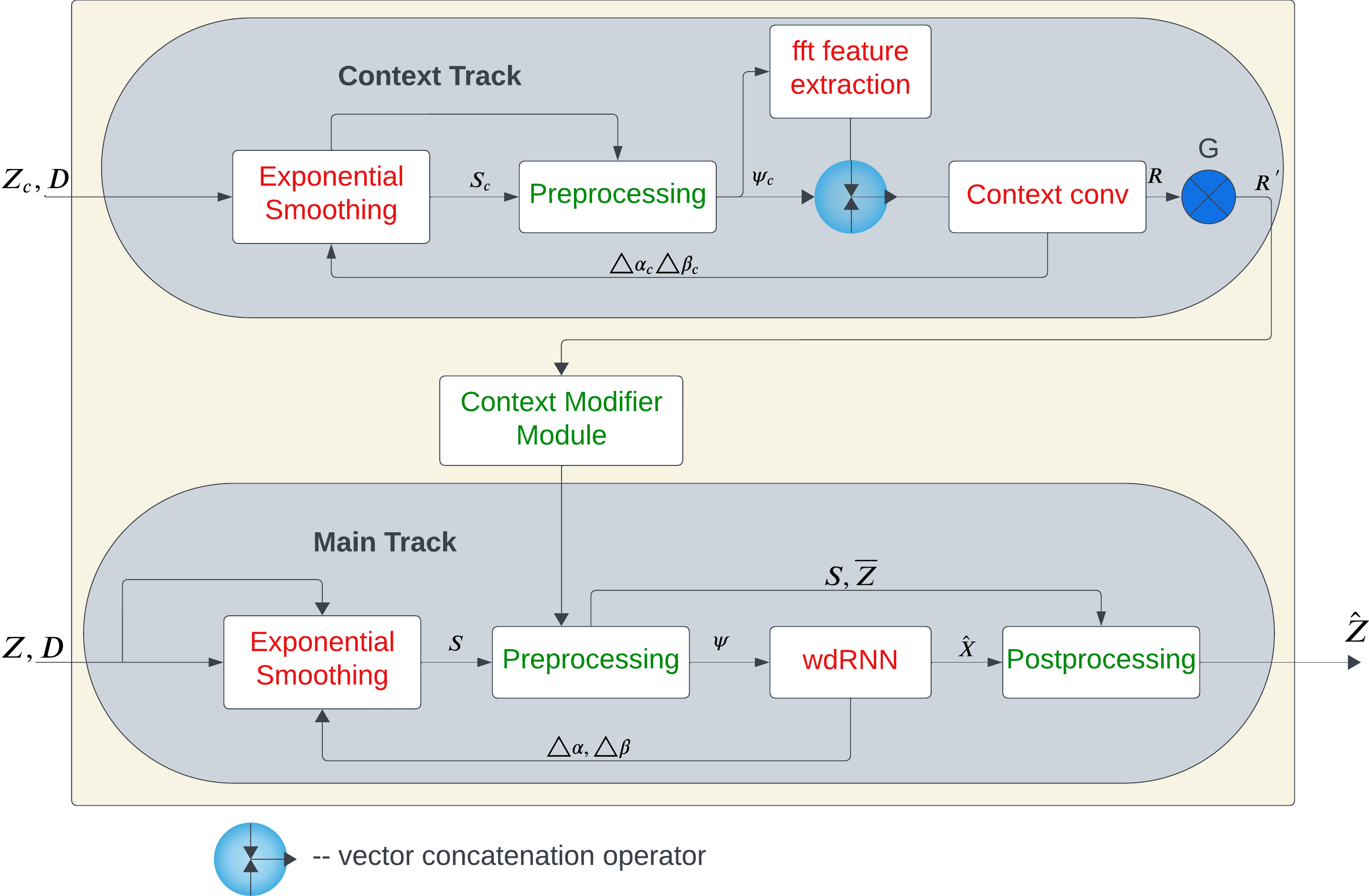

The paper proposes a Multi-Knowledge Fusion Network (MKFN) for time series representation learning. The key idea is to integrate multiple knowledge sources, including statistical, semantic, and temporal information, to capture comprehensive features of the input time series.

The MKFN architecture consists of three main components:

-

Statistical Knowledge Extractor: This module learns statistical features of the time series, such as trends, seasonality, and autocorrelation patterns.

-

Semantic Knowledge Extractor: This component extracts semantic information about the time series, such as the context and relationships between the variables being measured.

-

Temporal Knowledge Extractor: This module models the temporal dependencies within the time series, capturing how the values at different time points are related.

The outputs from these three knowledge extractors are then combined using a fusion module to produce a comprehensive representation of the input time series. This fused representation can be used for various downstream tasks, such as time series classification and forecasting.

The authors evaluate MKFN on several benchmark datasets for these tasks, and compare its performance to other state-of-the-art time series models. The results demonstrate that MKFN outperforms the competing methods, highlighting the benefits of the multi-knowledge fusion approach.

Critical Analysis

The paper presents a well-designed and thorough evaluation of the MKFN model, with experiments on multiple benchmark datasets and comparisons to several baselines. The authors also provide detailed ablation studies to understand the contribution of each knowledge source to the overall performance.

One potential limitation of the MKFN approach is the complexity of the model, which may make it more difficult to interpret and understand the underlying reasons for its success. The authors do not provide much insight into the specific mechanisms by which the fusion of the different knowledge sources leads to improved performance.

Additionally, the paper does not explore the robustness of MKFN to noisy or missing data, which is an important consideration for real-world time series applications. It would be valuable to investigate how the model's performance is affected by common data quality issues.

Overall, the Multi-Knowledge Fusion Network represents an interesting and promising approach to time series representation learning. Further research could explore ways to make the model more interpretable and investigate its performance in more challenging and realistic scenarios.

Conclusion

This paper introduces the Multi-Knowledge Fusion Network (MKFN), a novel model for learning representations of time series data. MKFN integrates multiple knowledge sources, including statistical, semantic, and temporal information, to capture comprehensive features of the input time series.

The authors demonstrate the effectiveness of MKFN on several benchmark datasets for time series classification and forecasting tasks, where it outperforms other state-of-the-art models. This suggests that the multi-knowledge fusion approach is a promising direction for improving the performance of time series analysis and prediction systems.

While the paper presents a thorough evaluation, there are opportunities to further explore the interpretability and robustness of the MKFN model. Nonetheless, this work represents an important contribution to the field of time series representation learning and opens up new avenues for future research.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Multi-Knowledge Fusion Network for Time Series Representation Learning

Sagar Srinivas Sakhinana, Shivam Gupta, Krishna Sai Sudhir Aripirala, Venkataramana Runkana

Forecasting the behaviour of complex dynamical systems such as interconnected sensor networks characterized by high-dimensional multivariate time series(MTS) is of paramount importance for making informed decisions and planning for the future in a broad spectrum of applications. Graph forecasting networks(GFNs) are well-suited for forecasting MTS data that exhibit spatio-temporal dependencies. However, most prior works of GFN-based methods on MTS forecasting rely on domain-expertise to model the nonlinear dynamics of the system, but neglect the potential to leverage the inherent relational-structural dependencies among time series variables underlying MTS data. On the other hand, contemporary works attempt to infer the relational structure of the complex dependencies between the variables and simultaneously learn the nonlinear dynamics of the interconnected system but neglect the possibility of incorporating domain-specific prior knowledge to improve forecast accuracy. To this end, we propose a hybrid architecture that combines explicit prior knowledge with implicit knowledge of the relational structure within the MTS data. It jointly learns intra-series temporal dependencies and inter-series spatial dependencies by encoding time-conditioned structural spatio-temporal inductive biases to provide more accurate and reliable forecasts. It also models the time-varying uncertainty of the multi-horizon forecasts to support decision-making by providing estimates of prediction uncertainty. The proposed architecture has shown promising results on multiple benchmark datasets and outperforms state-of-the-art forecasting methods by a significant margin. We report and discuss the ablation studies to validate our forecasting architecture.

Read more8/23/2024

0

Multi-Source Knowledge-Based Hybrid Neural Framework for Time Series Representation Learning

Sagar Srinivas Sakhinana, Krishna Sai Sudhir Aripirala, Shivam Gupta, Venkataramana Runkana

Accurately predicting the behavior of complex dynamical systems, characterized by high-dimensional multivariate time series(MTS) in interconnected sensor networks, is crucial for informed decision-making in various applications to minimize risk. While graph forecasting networks(GFNs) are ideal for forecasting MTS data that exhibit spatio-temporal dependencies, prior works rely solely on the domain-specific knowledge of time-series variables inter-relationships to model the nonlinear dynamics, neglecting inherent relational structural dependencies among the variables within the MTS data. In contrast, contemporary works infer relational structures from MTS data but neglect domain-specific knowledge. The proposed hybrid architecture addresses these limitations by combining both domain-specific knowledge and implicit knowledge of the relational structure underlying the MTS data using Knowledge-Based Compositional Generalization. The hybrid architecture shows promising results on multiple benchmark datasets, outperforming state-of-the-art forecasting methods. Additionally, the architecture models the time varying uncertainty of multi-horizon forecasts.

Read more8/23/2024

0

ForecastGrapher: Redefining Multivariate Time Series Forecasting with Graph Neural Networks

Wanlin Cai, Kun Wang, Hao Wu, Xiaoxu Chen, Yuankai Wu

The challenge of effectively learning inter-series correlations for multivariate time series forecasting remains a substantial and unresolved problem. Traditional deep learning models, which are largely dependent on the Transformer paradigm for modeling long sequences, often fail to integrate information from multiple time series into a coherent and universally applicable model. To bridge this gap, our paper presents ForecastGrapher, a framework reconceptualizes multivariate time series forecasting as a node regression task, providing a unique avenue for capturing the intricate temporal dynamics and inter-series correlations. Our approach is underpinned by three pivotal steps: firstly, generating custom node embeddings to reflect the temporal variations within each series; secondly, constructing an adaptive adjacency matrix to encode the inter-series correlations; and thirdly, augmenting the GNNs' expressive power by diversifying the node feature distribution. To enhance this expressive power, we introduce the Group Feature Convolution GNN (GFC-GNN). This model employs a learnable scaler to segment node features into multiple groups and applies one-dimensional convolutions with different kernel lengths to each group prior to the aggregation phase. Consequently, the GFC-GNN method enriches the diversity of node feature distribution in a fully end-to-end fashion. Through extensive experiments and ablation studies, we show that ForecastGrapher surpasses strong baselines and leading published techniques in the domain of multivariate time series forecasting.

Read more5/29/2024

0

Context Neural Networks: A Scalable Multivariate Model for Time Series Forecasting

Abishek Sriramulu, Christoph Bergmeir, Slawek Smyl

Real-world time series often exhibit complex interdependencies that cannot be captured in isolation. Global models that model past data from multiple related time series globally while producing series-specific forecasts locally are now common. However, their forecasts for each individual series remain isolated, failing to account for the current state of its neighbouring series. Multivariate models like multivariate attention and graph neural networks can explicitly incorporate inter-series information, thus addressing the shortcomings of global models. However, these techniques exhibit quadratic complexity per timestep, limiting scalability. This paper introduces the Context Neural Network, an efficient linear complexity approach for augmenting time series models with relevant contextual insights from neighbouring time series without significant computational overhead. The proposed method enriches predictive models by providing the target series with real-time information from its neighbours, addressing the limitations of global models, yet remaining computationally tractable for large datasets.

Read more5/14/2024