PayOff: A Regulated Central Bank Digital Currency with Private Offline Payments

0

Sign in to get full access

Overview

- This paper proposes a novel central bank digital currency (CBDC) system called PayOff that enables private offline payments.

- PayOff aims to combine the privacy of cash with the convenience of digital payments, while remaining under the regulation and oversight of a central bank.

- The system utilizes a cryptographic protocol to allow users to make transactions without revealing their identities to the central bank.

Plain English Explanation

The paper describes a new type of digital currency called PayOff that is issued and controlled by a central bank, but allows for private, offline transactions between users. This is intended to provide the privacy benefits of cash along with the convenience of digital payments.

The key idea is that users can make payments to each other without the central bank being able to identify the parties involved. This is achieved through a cryptographic protocol that hides the users' identities while still allowing the central bank to oversee the system and ensure it is used properly.

This could be useful for situations where people want to make transactions privately, such as paying for goods or services without leaving a digital trail. At the same time, the central bank maintains control and can intervene if the system is being used for illegal activities.

Technical Explanation

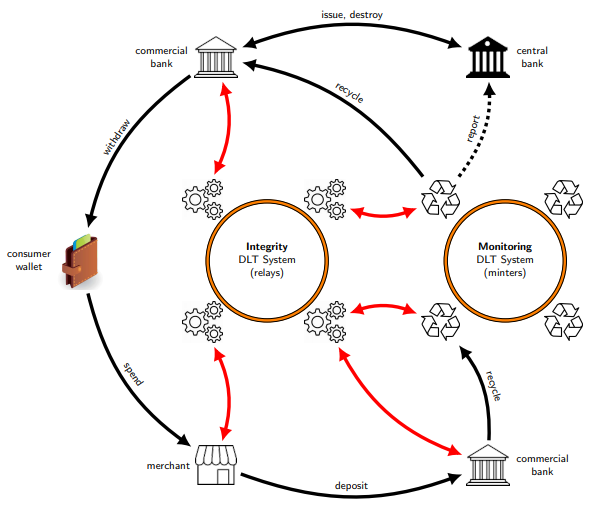

The paper proposes a regulated CBDC system called PayOff that enables private offline payments. The system utilizes a cryptographic protocol to allow users to make transactions without revealing their identities to the central bank.

The core technical components of PayOff include:

- A non-custodial wallet design that stores user funds and facilitates offline transactions

- A decentralized token architecture for representing the digital currency

- A FIDO2-compatible smart card that acts as a secure hardware device for user authentication and transaction signing

The protocol allows users to make payments to each other without revealing their identities to the central bank. This is achieved through the use of cryptographic techniques such as anonymous credentials and zero-knowledge proofs.

Critical Analysis

The paper addresses an important challenge in CBDC design - balancing privacy and regulatory oversight. By enabling private offline payments, PayOff aims to provide the benefits of cash-like privacy while still maintaining central bank control and the ability to monitor the system for illicit activities.

However, the paper does not fully explore the tradeoffs and potential risks of this approach. For example, it's unclear how the central bank would detect and prevent money laundering or other financial crimes in a system with strong user privacy. Additionally, the reliance on specialized hardware (smart cards) could introduce accessibility and scalability challenges.

Further research would be needed to better understand the security and practical implications of the PayOff design, as well as to explore alternative approaches that might achieve a different balance between privacy and regulatory control.

Conclusion

The PayOff CBDC system proposed in this paper represents an interesting attempt to combine the privacy of cash with the convenience of digital payments, while still maintaining central bank oversight and regulation.

The technical details of the protocol are promising, but the paper raises some critical questions about the practicality and safety of this approach. Ongoing research and experimentation will be needed to further develop and refine CBDC designs that can meet the diverse needs of users, regulators, and society as a whole.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

PayOff: A Regulated Central Bank Digital Currency with Private Offline Payments

Carolin Beer, Sheila Zingg, Kari Kostiainen, Karl Wust, Vedran Capkun, Srdjan Capkun

The European Central Bank is preparing for the potential issuance of a central bank digital currency (CBDC), called the digital euro. A recent regulatory proposal by the European Commission defines several requirements for the digital euro, such as support for both online and offline payments. Offline payments are expected to enable cash-like privacy, local payment settlement, and the enforcement of holding limits. While other central banks have expressed similar desired functionality, achieving such offline payments poses a novel technical challenge. We observe that none of the existing research solutions, including offline E-cash schemes, are fully compliant. Proposed solutions based on secure elements offer no guarantees in case of compromise and can therefore lead to significant payment fraud. The main contribution of this paper is PayOff, a novel CBDC design motivated by the digital euro regulation, which focuses on offline payments. We analyze the security implications of local payment settlement and identify new security objectives. PayOff protects user privacy, supports complex regulations such as holding limits, and implements safeguards to increase robustness against secure element failure. Our analysis shows that PayOff provides strong privacy and identifies residual leakages that may arise in real-world deployments. Our evaluation shows that offline payments can be fast and that the central bank can handle high payment loads with moderate computing resources. However, the main limitation of PayOff is that offline payment messages and storage requirements grow in the number of payments that the sender makes or receives without going online in between.

Read more8/14/2024

🤔

0

Retail Central Bank Digital Currency: Motivations, Opportunities, and Mistakes

Geoffrey Goodell, Hazem Danny Al-Nakib, Tomaso Aste

Nations around the world are conducting research into the design of central bank digital currency (CBDC), a new, digital form of money that would be issued by central banks alongside cash and central bank reserves. Retail CBDC would be used by individuals and businesses as form of money suitable for routine commerce. An important motivating factor in the development of retail CBDC is the decline of the popularity of central bank money for retail purchases and the increasing use of digital money created by the private sector for such purposes. The debate about how retail CBDC would be designed and implemented has led to many proposals, which have sparked considerable debate about business models, regulatory frameworks, and the socio-technical role of money in general. Here, we present a critical analysis of the existing proposals. We examine their motivations and themes, as well as their underlying assumptions. We also offer a reflection of the opportunity that retail CBDC represents and suggest a way forward in furtherance of the public interest.

Read more4/5/2024

0

New!Payments Use Cases and Design Options for Interoperability and Funds Locking across Digital Pounds and Commercial Bank Money

Lee Braine, Shreepad Shukla, Piyush Agrawal, Shrirang Khedekar, Aishwarya Nair

Central banks are actively exploring retail central bank digital currencies (CBDCs), with the Bank of England currently in the design phase for a potential UK retail CBDC, the digital pound. In a previous paper, we defined and explored the important concept of functional consistency (which is the principle that different forms of money have the same operational characteristics) and evaluated design options to support functional consistency across digital pounds and commercial bank money, based on a set of key capabilities. In this paper, we continue to analyse the design options for supporting functional consistency and, in order to perform a detailed analysis, we focus on three key capabilities: communication between digital pound ecosystem participants, funds locking, and interoperability across digital pounds and commercial bank money. We explore these key capabilities via three payments use cases: person-to-person push payment, merchant-initiated request to pay, and lock funds and pay on physical delivery. We then present and evaluate the suitability of design options to provide the specific capabilities for each use case and draw initial insights. We conclude that a financial market infrastructure (FMI) providing specific capabilities could simplify the experience of ecosystem participants, simplify the operating platforms for both the Bank of England and digital pound Payment Interface Providers (PIPs), and facilitate the creation of innovative services. We also identify potential next steps.

Read more9/16/2024

0

Benchmarking the performance of a self-custody, non-ledger-based, obliviously managed digital payment system

William Macpherson, Geoffrey Goodell

As global governments intensify efforts to operationalize retail central bank digital currencies (CBDCs), the imperative for architectures that preserve user privacy has never been more pronounced. This paper advances an existing retail CBDC framework developed at University College London. Utilizing the capabilities of the Comet research framework, our proposed design allows users to retain direct custody of their assets without the need for intermediary service providers, all while preserving transactional anonymity. The study unveils a novel technique to expedite the retrieval of Proof of Provenance, significantly accelerating the verification of transaction legitimacy through the refinement of Merkle Trie structures. In parallel, we introduce a streamlined Digital Ledger designed to offer fast, immutable, and decentralized transaction validation within a permissioned ecosystem. The ultimate objective of this research is to benchmark the performance of the legacy system formulated by the original Comet research team against the newly devised system elucidated in this paper. Our endeavour is to establish a foundational design for a scalable national infrastructure proficient in seamlessly processing thousands of transactions in real-time, without compromising consumer privacy or data integrity.

Read more4/22/2024