Stock Recommendations for Individual Investors: A Temporal Graph Network Approach with Diversification-Enhancing Contrastive Learning

0

Sign in to get full access

Overview

- Proposes a novel Temporal Graph Network (TGN) approach for stock recommendations that enhances diversification through contrastive learning

- Aims to provide personalized stock recommendations for individual investors by capturing evolving investor-stock relationships over time

- Leverages the power of graph neural networks to model the complex temporal dynamics of the stock market

Plain English Explanation

This research paper presents a new method for providing personalized stock recommendations to individual investors. The key idea is to model the relationships between investors and stocks as a temporal graph network. This allows the system to capture how these relationships change over time, which is important for making accurate stock recommendations.

The researchers use a technique called contrastive learning to help ensure that the recommended stocks are diverse and reduce the risk of an investor's portfolio. This is important because individual investors often struggle to build well-diversified portfolios on their own.

Overall, the goal is to leverage the power of graph neural networks and modern machine learning techniques to provide individual investors with personalized stock recommendations that can help them achieve better investment outcomes.

Technical Explanation

The paper proposes a Temporal Graph Network (TGN) model for personalized stock recommendations. The TGN approach models the evolving relationships between investors and stocks as a dynamic graph, where nodes represent investors and stocks, and edges represent the interactions between them.

The key innovations of the TGN model include:

-

Temporal Encoding: The model encodes the temporal dynamics of the investor-stock relationships using specialized temporal embedding layers. This allows the model to capture how these relationships change over time.

-

Contrastive Learning: The researchers employ a contrastive learning strategy to encourage the model to recommend a diverse set of stocks. This helps to enhance the diversification of the recommended portfolio.

-

Personalization: The TGN model is trained to provide personalized recommendations for each individual investor, taking into account their unique investment preferences and past behavior.

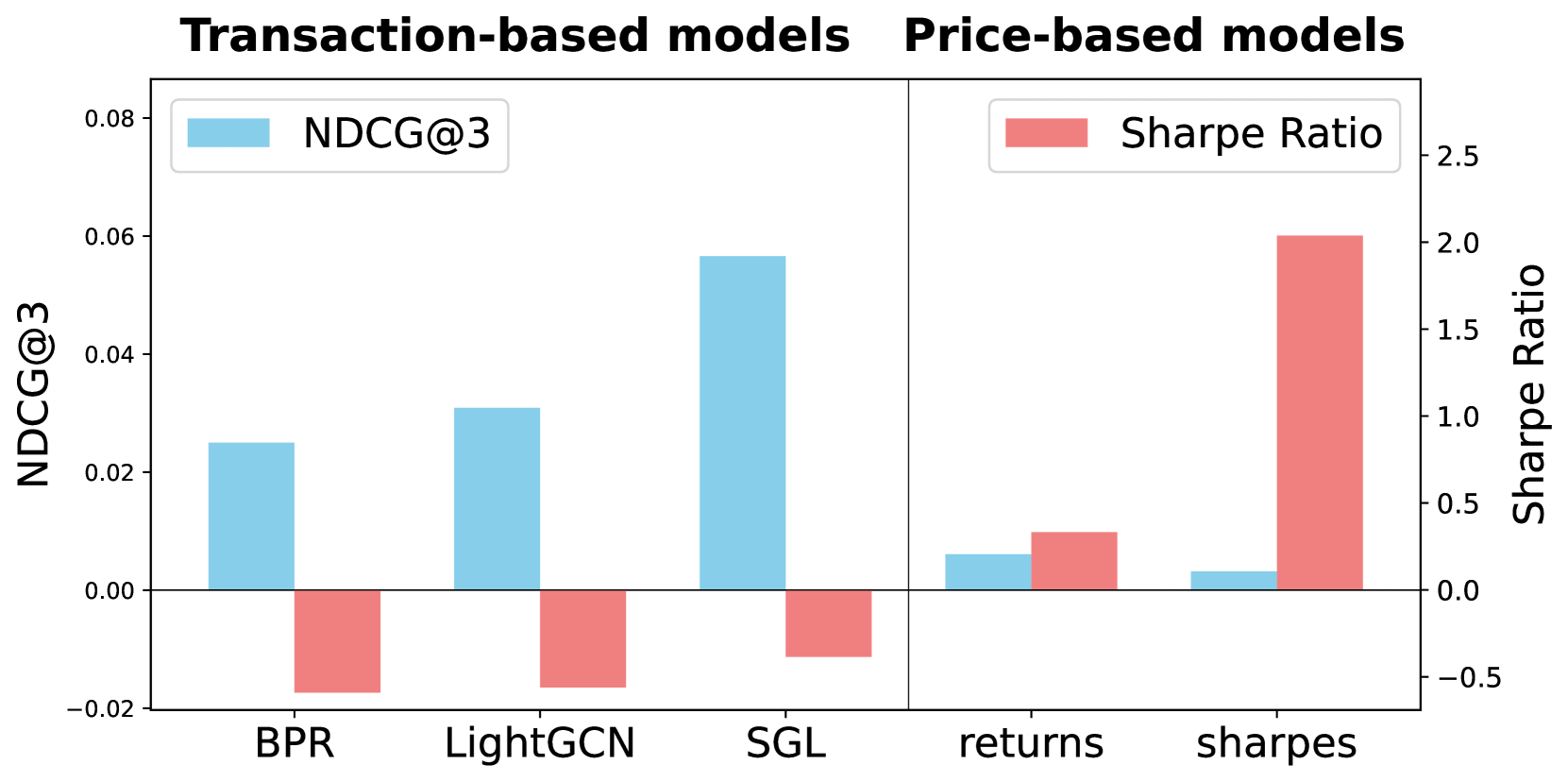

The researchers evaluate their TGN model on real-world stock market data and demonstrate that it outperforms several state-of-the-art baselines in terms of recommendation accuracy and diversification.

Critical Analysis

The paper presents a well-designed and technically sound approach for addressing the challenge of personalized stock recommendations for individual investors. The key strengths of the research include:

- The use of a temporal graph network to model the evolving investor-stock relationships, which is a novel and promising approach in this domain.

- The incorporation of contrastive learning to enhance the diversification of recommended portfolios, which is an important consideration for individual investors.

- The personalization aspect, which tailors the recommendations to each individual's investment preferences and history.

However, the paper also acknowledges several limitations and areas for future research:

- The model's performance may be sensitive to the quality and availability of the underlying data, which can be a challenge in the stock market domain.

- The researchers suggest exploring additional features, such as news and sentiment data, to further improve the model's predictive power.

- Incorporating more sophisticated risk modeling and portfolio optimization techniques could potentially lead to even stronger investment recommendations.

Overall, this research represents an important step forward in the field of personalized stock recommendations for individual investors, and the proposed TGN model with diversification-enhancing contrastive learning is a valuable contribution to the literature.

Conclusion

The paper presents a novel Temporal Graph Network (TGN) approach for providing personalized stock recommendations to individual investors. By modeling the evolving investor-stock relationships as a dynamic graph and leveraging contrastive learning to enhance portfolio diversification, the TGN model aims to deliver more accurate and well-rounded investment recommendations.

The strong technical approach and promising results demonstrated in the paper suggest that this research could have significant implications for improving the investment outcomes of individual investors. As the authors note, there are still opportunities for further refinement and expansion of the TGN model, but this work represents an important step forward in the field of personalized finance.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Stock Recommendations for Individual Investors: A Temporal Graph Network Approach with Diversification-Enhancing Contrastive Learning

Youngbin Lee, Yejin Kim, Javier Sanz-Cruzado, Richard McCreadie, Yongjae Lee

Recommender systems can be helpful for individuals to make well-informed decisions in complex financial markets. While many studies have focused on predicting stock prices, even advanced models fall short of accurately forecasting them. Additionally, previous studies indicate that individual investors often disregard established investment theories, favoring their personal preferences instead. This presents a challenge for stock recommendation systems, which must not only provide strong investment performance but also respect these individual preferences. To create effective stock recommender systems, three critical elements must be incorporated: 1) individual preferences, 2) portfolio diversification, and 3) the temporal dynamics of the first two. In response, we propose a new model, Portfolio Temporal Graph Network Recommender, PfoTGNRec, which can handle time-varying collaborative signals and incorporates diversification-enhancing sampling. On real-world individual trading data, our approach demonstrates superior performance compared to state-of-the-art baselines, including cutting-edge dynamic embedding models and existing stock recommendation models. Indeed, we show that PfoTGNRec is an effective solution that can balance customer preferences with the need to suggest portfolios with high Return-on-Investment. The source code and data are available at https://anonymous.4open.science/r/ICAIF2024-E23E.

Read more8/20/2024

0

Temporal Graph Neural Network-Powered Paper Recommendation on Dynamic Citation Networks

Junhao Shen, Mohammad Ausaf Ali Haqqani, Beichen Hu, Cheng Huang, Xihao Xie, Tsengdar Lee, Jia Zhang

Due to the rapid growth of scientific publications, identifying all related reference articles in the literature has become increasingly challenging yet highly demanding. Existing methods primarily assess candidate publications from a static perspective, focusing on the content of articles and their structural information, such as citation relationships. There is a lack of research regarding how to account for the evolving impact among papers on their embeddings. Toward this goal, this paper introduces a temporal dimension to paper recommendation strategies. The core idea is to continuously update a paper's embedding when new citation relationships appear, enhancing its relevance for future recommendations. Whenever a citation relationship is added to the literature upon the publication of a paper, the embeddings of the two related papers are updated through a Temporal Graph Neural Network (TGN). A learnable memory update module based on a Recurrent Neural Network (RNN) is utilized to study the evolution of the embedding of a paper in order to predict its reference impact in a future timestamp. Such a TGN-based model learns a pattern of how people's views of the paper may evolve, aiming to guide paper recommendations more precisely. Extensive experiments on an open citation network dataset, including 313,278 articles from https://paperswithcode.com/about PaperWithCode, have demonstrated the effectiveness of the proposed approach.

Read more8/29/2024

0

TCGPN: Temporal-Correlation Graph Pre-trained Network for Stock Forecasting

Wenbo Yan, Ying Tan

Recently, the incorporation of both temporal features and the correlation across time series has become an effective approach in time series prediction. Spatio-Temporal Graph Neural Networks (STGNNs) demonstrate good performance on many Temporal-correlation Forecasting Problem. However, when applied to tasks lacking periodicity, such as stock data prediction, the effectiveness and robustness of STGNNs are found to be unsatisfactory. And STGNNs are limited by memory savings so that cannot handle problems with a large number of nodes. In this paper, we propose a novel approach called the Temporal-Correlation Graph Pre-trained Network (TCGPN) to address these limitations. TCGPN utilize Temporal-correlation fusion encoder to get a mixed representation and pre-training method with carefully designed temporal and correlation pre-training tasks. Entire structure is independent of the number and order of nodes, so better results can be obtained through various data enhancements. And memory consumption during training can be significantly reduced through multiple sampling. Experiments are conducted on real stock market data sets CSI300 and CSI500 that exhibit minimal periodicity. We fine-tune a simple MLP in downstream tasks and achieve state-of-the-art results, validating the capability to capture more robust temporal correlation patterns.

Read more7/29/2024

0

Temporal Representation Learning for Stock Similarities and Its Applications in Investment Management

Yoontae Hwang, Stefan Zohren, Yongjae Lee

In the era of rapid globalization and digitalization, accurate identification of similar stocks has become increasingly challenging due to the non-stationary nature of financial markets and the ambiguity in conventional regional and sector classifications. To address these challenges, we examine SimStock, a novel temporal self-supervised learning framework that combines techniques from self-supervised learning (SSL) and temporal domain generalization to learn robust and informative representations of financial time series data. The primary focus of our study is to understand the similarities between stocks from a broader perspective, considering the complex dynamics of the global financial landscape. We conduct extensive experiments on four real-world datasets with thousands of stocks and demonstrate the effectiveness of SimStock in finding similar stocks, outperforming existing methods. The practical utility of SimStock is showcased through its application to various investment strategies, such as pairs trading, index tracking, and portfolio optimization, where it leads to superior performance compared to conventional methods. Our findings empirically examine the potential of data-driven approach to enhance investment decision-making and risk management practices by leveraging the power of temporal self-supervised learning in the face of the ever-changing global financial landscape.

Read more7/19/2024