TimeSieve: Extracting Temporal Dynamics through Information Bottlenecks

0

Sign in to get full access

Overview

- The paper presents "TimeSieve," a novel approach for extracting temporal dynamics from time series data using an information bottleneck framework.

- TimeSieve aims to identify the essential temporal patterns in the data while discarding irrelevant information, providing a concise and interpretable representation of the time series.

- The method leverages the information bottleneck principle to learn a compressed representation that captures the relevant temporal dynamics.

- TimeSieve is evaluated on several real-world datasets, demonstrating its effectiveness in tasks like time series forecasting and anomaly detection.

Plain English Explanation

The paper introduces a new technique called "TimeSieve" that can extract the essential patterns over time from data that changes over time, like stock prices or weather measurements. The key idea is to find a compact summary of the data that captures the important dynamics while filtering out unnecessary details.

The approach works by using a concept called the "information bottleneck," which tries to find a balance between keeping the important information and compressing the data. This allows TimeSieve to identify the crucial temporal patterns in the data in a way that is easy for humans to understand, rather than getting bogged down in all the minute details.

The researchers tested TimeSieve on real-world datasets, showing that it can improve the performance of tasks like forecasting future values or detecting unusual events in time series data. By focusing on the essential temporal dynamics, TimeSieve provides a concise and interpretable representation of the data that can be valuable for analysis and decision-making.

Technical Explanation

The paper presents a novel method called "TimeSieve" that aims to extract the key temporal dynamics from time series data using an information bottleneck framework. The core idea is to learn a compressed representation of the time series that captures the essential patterns while discarding irrelevant information.

TimeSieve leverages the information bottleneck principle, which seeks to find a concise summary of the input data that preserves the relevant information for a given task. In the context of time series, this allows the method to identify the critical temporal dynamics that are important for downstream applications like forecasting or anomaly detection.

The authors evaluate TimeSieve on several real-world datasets, including financial time series, weather measurements, and smart city sensor data. The results demonstrate the effectiveness of the approach in learning a compact and interpretable representation of the temporal dynamics, leading to improved performance on various time series analysis tasks.

Critical Analysis

The paper presents a well-designed and empirically validated approach for extracting temporal dynamics from time series data. The authors acknowledge some potential limitations, such as the assumption of piecewise-linear dynamics and the need for careful hyperparameter tuning.

One area for further research could be exploring the application of more flexible temporal models, such as those based on adaptive wavelets, to capture a wider range of nonlinear patterns in the data. Additionally, investigating the robustness of TimeSieve to missing data or noisy observations could be a valuable extension.

Overall, the paper makes a compelling case for the effectiveness of the information bottleneck principle in time series analysis and provides a promising direction for developing more interpretable and efficient representations of temporal dynamics in data.

Conclusion

The "TimeSieve" method introduced in this paper offers a novel approach to extracting the essential temporal patterns from time series data. By leveraging the information bottleneck principle, TimeSieve is able to learn a compressed representation that captures the crucial dynamics while discarding irrelevant information.

The evaluation of TimeSieve on various real-world datasets demonstrates its potential to improve the performance of time series analysis tasks, such as forecasting and anomaly detection. The interpretable nature of the learned representations can also provide valuable insights for domain experts and decision-makers.

As the volume and complexity of time series data continue to grow, methods like TimeSieve will become increasingly important for making sense of the underlying temporal dynamics in a concise and meaningful way. The paper lays the groundwork for further advancements in this direction, paving the way for more efficient and interpretable time series analysis techniques.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

TimeSieve: Extracting Temporal Dynamics through Information Bottlenecks

Ninghui Feng, Songning Lai, Jiayu Yang, Fobao Zhou, Zhenxiao Yin, Hang Zhao

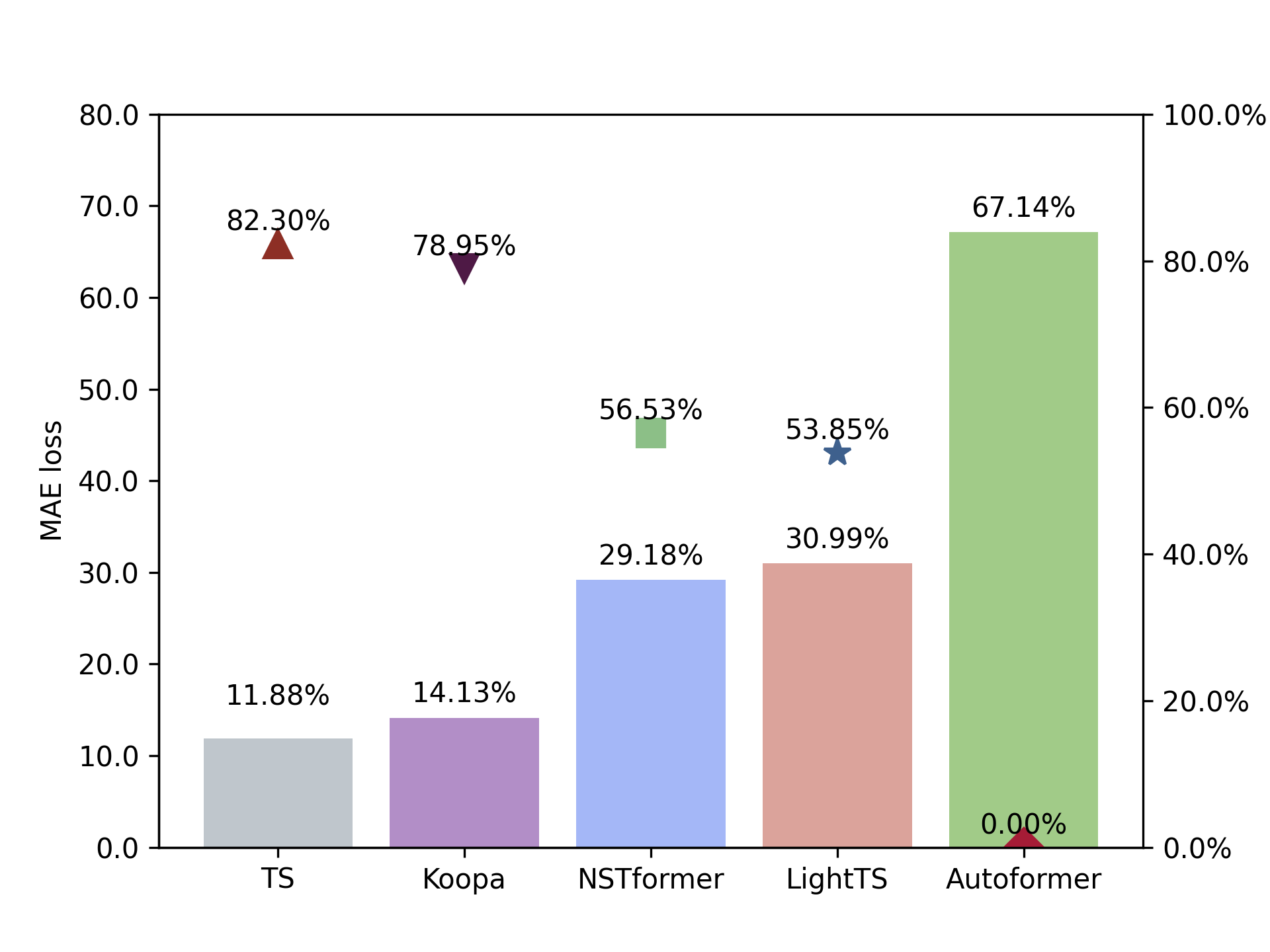

Time series forecasting has become an increasingly popular research area due to its critical applications in various real-world domains such as traffic management, weather prediction, and financial analysis. Despite significant advancements, existing models face notable challenges, including the necessity of manual hyperparameter tuning for different datasets, and difficulty in effectively distinguishing signal from redundant features in data characterized by strong seasonality. These issues hinder the generalization and practical application of time series forecasting models. To solve this issues, we propose an innovative time series forecasting model TimeSieve designed to address these challenges. Our approach employs wavelet transforms to preprocess time series data, effectively capturing multi-scale features without the need for additional parameters or manual hyperparameter tuning. Additionally, we introduce the information bottleneck theory that filters out redundant features from both detail and approximation coefficients, retaining only the most predictive information. This combination reduces significantly improves the model's accuracy. Extensive experiments demonstrate that our model outperforms existing state-of-the-art methods on 70% of the datasets, achieving higher predictive accuracy and better generalization across diverse datasets. Our results validate the effectiveness of our approach in addressing the key challenges in time series forecasting, paving the way for more reliable and efficient predictive models in practical applications. The code for our model is available at https://github.com/xll0328/TimeSieve.

Read more8/22/2024

0

TimeX++: Learning Time-Series Explanations with Information Bottleneck

Zichuan Liu, Tianchun Wang, Jimeng Shi, Xu Zheng, Zhuomin Chen, Lei Song, Wenqian Dong, Jayantha Obeysekera, Farhad Shirani, Dongsheng Luo

Explaining deep learning models operating on time series data is crucial in various applications of interest which require interpretable and transparent insights from time series signals. In this work, we investigate this problem from an information theoretic perspective and show that most existing measures of explainability may suffer from trivial solutions and distributional shift issues. To address these issues, we introduce a simple yet practical objective function for time series explainable learning. The design of the objective function builds upon the principle of information bottleneck (IB), and modifies the IB objective function to avoid trivial solutions and distributional shift issues. We further present TimeX++, a novel explanation framework that leverages a parametric network to produce explanation-embedded instances that are both in-distributed and label-preserving. We evaluate TimeX++ on both synthetic and real-world datasets comparing its performance against leading baselines, and validate its practical efficacy through case studies in a real-world environmental application. Quantitative and qualitative evaluations show that TimeX++ outperforms baselines across all datasets, demonstrating a substantial improvement in explanation quality for time series data. The source code is available at url{https://github.com/zichuan-liu/TimeXplusplus}.

Read more5/16/2024

0

FTS: A Framework to Find a Faithful TimeSieve

Songning Lai, Ninghui Feng, Jiechao Gao, Hao Wang, Haochen Sui, Xin Zou, Jiayu Yang, Wenshuo Chen, Hang Zhao, Xuming Hu, Yutao Yue

The field of time series forecasting has garnered significant attention in recent years, prompting the development of advanced models like TimeSieve, which demonstrates impressive performance. However, an analysis reveals certain unfaithfulness issues, including high sensitivity to random seeds, input and layer noise perturbations and parametric perturbations. Recognizing these challenges, we embark on a quest to define the concept of textbf{underline{F}aithful underline{T}imeunderline{S}ieve underline{(FTS)}}, a model that consistently delivers reliable and robust predictions. To address these issues, we propose a novel framework aimed at identifying and rectifying unfaithfulness in TimeSieve. Our framework is designed to enhance the model's stability and faithfulness, ensuring that its outputs are less susceptible to the aforementioned factors. Experimentation validates the effectiveness of our proposed framework, demonstrating improved faithfulness in the model's behavior.

Read more8/13/2024

0

WEITS: A Wavelet-enhanced residual framework for interpretable time series forecasting

Ziyou Guo, Yan Sun, Tieru Wu

Time series (TS) forecasting has been an unprecedentedly popular problem in recent years, with ubiquitous applications in both scientific and business fields. Various approaches have been introduced to time series analysis, including both statistical approaches and deep neural networks. Although neural network approaches have illustrated stronger ability of representation than statistical methods, they struggle to provide sufficient interpretablility, and can be too complicated to optimize. In this paper, we present WEITS, a frequency-aware deep learning framework that is highly interpretable and computationally efficient. Through multi-level wavelet decomposition, WEITS novelly infuses frequency analysis into a highly deep learning framework. Combined with a forward-backward residual architecture, it enjoys both high representation capability and statistical interpretability. Extensive experiments on real-world datasets have demonstrated competitive performance of our model, along with its additional advantage of high computation efficiency. Furthermore, WEITS provides a general framework that can always seamlessly integrate with state-of-the-art approaches for time series forecast.

Read more5/20/2024