Application of Natural Language Processing in Financial Risk Detection

2406.09765

0

0

🌿

Abstract

This paper explores the application of Natural Language Processing (NLP) in financial risk detection. By constructing an NLP-based financial risk detection model, this study aims to identify and predict potential risks in financial documents and communications. First, the fundamental concepts of NLP and its theoretical foundation, including text mining methods, NLP model design principles, and machine learning algorithms, are introduced. Second, the process of text data preprocessing and feature extraction is described. Finally, the effectiveness and predictive performance of the model are validated through empirical research. The results show that the NLP-based financial risk detection model performs excellently in risk identification and prediction, providing effective risk management tools for financial institutions. This study offers valuable references for the field of financial risk management, utilizing advanced NLP techniques to improve the accuracy and efficiency of financial risk detection.

Create account to get full access

Overview

- This paper explores the use of Natural Language Processing (NLP) techniques to detect financial risks in documents and communications.

- The study aims to develop an NLP-based model that can identify and predict potential risks in financial data.

- The paper covers the fundamental concepts of NLP, the process of text data preprocessing and feature extraction, and the validation of the model's effectiveness and predictive performance.

Plain English Explanation

The paper investigates how Natural Language Processing (NLP) can be used to detect financial risks. The researchers built an NLP-based model to analyze financial documents and communications and identify potential risks.

First, the paper explains the basics of NLP, including text mining methods, model design principles, and machine learning algorithms. This provides the foundation for understanding how the NLP-based model works.

Next, the researchers describe the process of preparing the text data and extracting relevant features for the model. This preprocessing step is crucial for ensuring the model can accurately analyze the financial information.

Finally, the researchers validate the effectiveness and predictive performance of the NLP-based financial risk detection model. The results show that the model is excellent at identifying and predicting risks, which can provide valuable tools for financial risk management.

Overall, this study demonstrates how advanced NLP techniques can be applied to improve the accuracy and efficiency of financial risk detection. This can be especially useful for financial institutions looking to enhance their risk management capabilities.

Technical Explanation

The paper first introduces the fundamental concepts of NLP and its theoretical foundations, including text mining methods, NLP model design principles, and machine learning algorithms. This lays the groundwork for understanding the approach used in the study.

The researchers then describe the process of text data preprocessing and feature extraction. This involves cleaning and structuring the financial documents and communications to prepare them for analysis by the NLP-based model.

The researchers validate the effectiveness and predictive performance of the NLP-based financial risk detection model through empirical research. The results show that the model performs excellently in identifying and predicting potential risks, providing a valuable tool for financial risk management.

Critical Analysis

The paper provides a comprehensive overview of the application of NLP techniques to financial risk detection, offering a solid foundation for further research in this area. However, the study does not delve into the specific challenges or limitations encountered during the model development and validation process.

While the results demonstrate the model's strong performance, the paper could have explored potential biases or edge cases that may affect the model's reliability in real-world financial settings. Additionally, the paper does not address potential privacy or ethical concerns related to the use of NLP for analyzing sensitive financial data.

Further research could investigate the model's robustness to different types of financial documents and communications, as well as its adaptability to changing market conditions and regulatory environments. Exploring the integration of the NLP-based risk detection model with other financial risk management tools could also be a valuable area of study.

Conclusion

This paper presents a promising application of NLP techniques to financial risk detection. The developed NLP-based model demonstrates excellent performance in identifying and predicting potential risks in financial documents and communications.

The findings of this study have significant implications for the field of financial risk management, providing financial institutions with advanced tools to enhance their risk monitoring and mitigation capabilities. By leveraging the power of NLP, financial organizations can improve the accuracy and efficiency of their risk detection processes, ultimately contributing to more informed decision-making and greater financial stability.

The paper serves as a valuable reference for researchers and practitioners interested in exploring the intersection of NLP and financial risk management, paving the way for further advancements in this important field.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

Computational Job Market Analysis with Natural Language Processing

Mike Zhang

0

0

[Abridged Abstract] Recent technological advances underscore labor market dynamics, yielding significant consequences for employment prospects and increasing job vacancy data across platforms and languages. Aggregating such data holds potential for valuable insights into labor market demands, new skills emergence, and facilitating job matching for various stakeholders. However, despite prevalent insights in the private sector, transparent language technology systems and data for this domain are lacking. This thesis investigates Natural Language Processing (NLP) technology for extracting relevant information from job descriptions, identifying challenges including scarcity of training data, lack of standardized annotation guidelines, and shortage of effective extraction methods from job ads. We frame the problem, obtaining annotated data, and introducing extraction methodologies. Our contributions include job description datasets, a de-identification dataset, and a novel active learning algorithm for efficient model training. We propose skill extraction using weak supervision, a taxonomy-aware pre-training methodology adapting multilingual language models to the job market domain, and a retrieval-augmented model leveraging multiple skill extraction datasets to enhance overall performance. Finally, we ground extracted information within a designated taxonomy.

5/1/2024

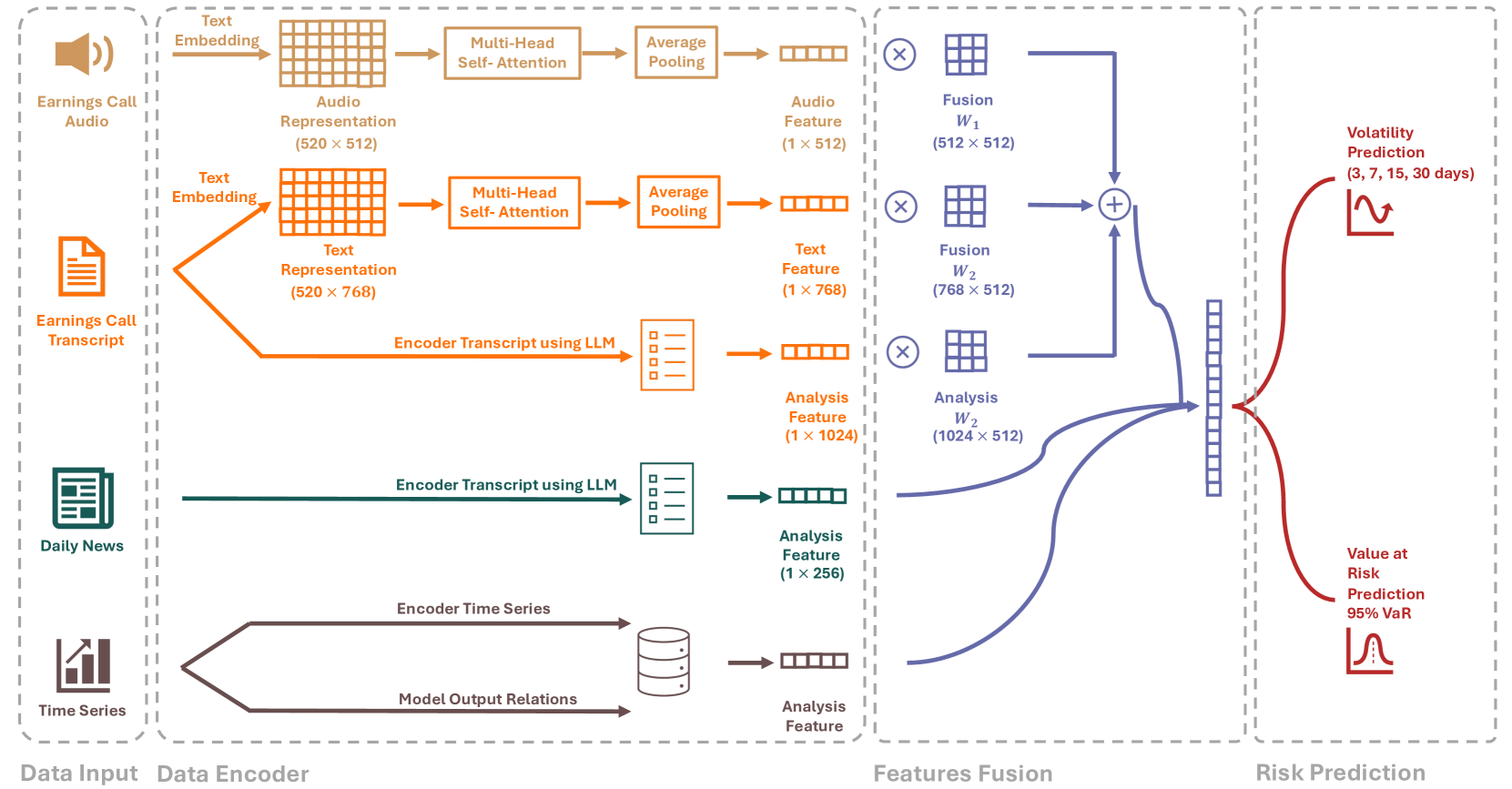

RiskLabs: Predicting Financial Risk Using Large Language Model Based on Multi-Sources Data

Yupeng Cao, Zhi Chen, Qingyun Pei, Fabrizio Dimino, Lorenzo Ausiello, Prashant Kumar, K. P. Subbalakshmi, Papa Momar Ndiaye

0

0

The integration of Artificial Intelligence (AI) techniques, particularly large language models (LLMs), in finance has garnered increasing academic attention. Despite progress, existing studies predominantly focus on tasks like financial text summarization, question-answering (Q$&$A), and stock movement prediction (binary classification), with a notable gap in the application of LLMs for financial risk prediction. Addressing this gap, in this paper, we introduce textbf{RiskLabs}, a novel framework that leverages LLMs to analyze and predict financial risks. RiskLabs uniquely combines different types of financial data, including textual and vocal information from Earnings Conference Calls (ECCs), market-related time series data, and contextual news data surrounding ECC release dates. Our approach involves a multi-stage process: initially extracting and analyzing ECC data using LLMs, followed by gathering and processing time-series data before the ECC dates to model and understand risk over different timeframes. Using multimodal fusion techniques, RiskLabs amalgamates these varied data features for comprehensive multi-task financial risk prediction. Empirical experiment results demonstrate RiskLab's effectiveness in forecasting both volatility and variance in financial markets. Through comparative experiments, we demonstrate how different data sources contribute to financial risk assessment and discuss the critical role of LLMs in this context. Our findings not only contribute to the AI in finance application but also open new avenues for applying LLMs in financial risk assessment.

4/12/2024

🔎

Challenges and Opportunities of NLP for HR Applications: A Discussion Paper

Jochen L. Leidner, Mark Stevenson

0

0

Over the course of the recent decade, tremendous progress has been made in the areas of machine learning and natural language processing, which opened up vast areas of potential application use cases, including hiring and human resource management. We review the use cases for text analytics in the realm of human resources/personnel management, including actually realized as well as potential but not yet implemented ones, and we analyze the opportunities and risks of these.

5/14/2024

🔎

Automatic detection of relevant information, predictions and forecasts in financial news through topic modelling with Latent Dirichlet Allocation

Silvia Garc'ia-M'endez, Francisco de Arriba-P'erez, Ana Barros-Vila, Francisco J. Gonz'alez-Casta~no, Enrique Costa-Montenegro

0

0

Financial news items are unstructured sources of information that can be mined to extract knowledge for market screening applications. Manual extraction of relevant information from the continuous stream of finance-related news is cumbersome and beyond the skills of many investors, who, at most, can follow a few sources and authors. Accordingly, we focus on the analysis of financial news to identify relevant text and, within that text, forecasts and predictions. We propose a novel Natural Language Processing (NLP) system to assist investors in the detection of relevant financial events in unstructured textual sources by considering both relevance and temporality at the discursive level. Firstly, we segment the text to group together closely related text. Secondly, we apply co-reference resolution to discover internal dependencies within segments. Finally, we perform relevant topic modelling with Latent Dirichlet Allocation (LDA) to separate relevant from less relevant text and then analyse the relevant text using a Machine Learning-oriented temporal approach to identify predictions and speculative statements. We created an experimental data set composed of 2,158 financial news items that were manually labelled by NLP researchers to evaluate our solution. The ROUGE-L values for the identification of relevant text and predictions/forecasts were 0.662 and 0.982, respectively. To our knowledge, this is the first work to jointly consider relevance and temporality at the discursive level. It contributes to the transfer of human associative discourse capabilities to expert systems through the combination of multi-paragraph topic segmentation and co-reference resolution to separate author expression patterns, topic modelling with LDA to detect relevant text, and discursive temporality analysis to identify forecasts and predictions within this text.

4/3/2024