DeepClair: Utilizing Market Forecasts for Effective Portfolio Selection

0

Sign in to get full access

Overview

- Proposes a deep reinforcement learning (DRL) framework called DeepClair for effective portfolio selection using market forecasts

- Integrates various market forecasting models to capture different market dynamics and trends

- Demonstrates improved portfolio performance compared to traditional portfolio optimization methods

Plain English Explanation

DeepClair: Utilizing Market Forecasts for Effective Portfolio Selection is a research paper that presents a new approach to portfolio management using deep reinforcement learning (DRL). The key idea is to utilize various market forecasting models to inform the portfolio selection process, rather than relying solely on historical data.

The researchers recognize that financial markets are complex and dynamic, with multiple factors influencing their behavior. By combining different forecasting models, the DeepClair framework aims to capture a more comprehensive understanding of the market landscape. This includes incorporating insights from models that can identify market trends and scale data effectively for improved forecasting accuracy.

The DRL component of DeepClair is designed to learn an optimal portfolio management strategy by interacting with the simulated market environment and receiving rewards based on the portfolio's performance. This allows the system to adapt and refine its decision-making over time, potentially outperforming traditional portfolio optimization methods.

Technical Explanation

DeepClair: Utilizing Market Forecasts for Effective Portfolio Selection proposes a deep reinforcement learning (DRL) framework for portfolio selection that integrates various market forecasting models. The authors argue that traditional portfolio optimization methods often rely solely on historical data, which may not capture the complex and dynamic nature of financial markets.

The DeepClair framework consists of two key components: a market forecasting module and a DRL-based portfolio management module. The market forecasting module integrates multiple models, including those that can identify market trends and scale data effectively, to provide a more comprehensive understanding of the market. The DRL-based portfolio management module then uses this forecasting information to learn an optimal portfolio management strategy through interaction with a simulated market environment.

The authors evaluate the performance of DeepClair on historical stock market data and compare it to traditional portfolio optimization methods. The results demonstrate that the proposed framework can outperform these conventional approaches, highlighting the potential benefits of integrating market forecasts into the portfolio selection process.

Critical Analysis

The DeepClair: Utilizing Market Forecasts for Effective Portfolio Selection paper presents a promising approach to portfolio management, but it also acknowledges several limitations and areas for further research.

One potential concern is the reliance on accurate market forecasts, which can be challenging to obtain in practice. The performance of the DeepClair framework is heavily dependent on the quality and reliability of the forecasting models used. The paper does not provide a detailed analysis of the sensitivity of the system to forecast errors or biases.

Additionally, the authors note that the DeepClair framework is evaluated on historical data, which may not fully capture the complexities and uncertainties of real-world financial markets. Further research is needed to assess the system's performance in live trading environments and its ability to adapt to changing market conditions.

The paper also mentions the computational complexity and training time associated with the DRL-based portfolio management module. This could be a practical challenge for real-world deployment, particularly for investors or institutions with limited computational resources.

While the paper presents promising results, it is essential for readers to critically evaluate the research and consider the potential limitations and areas for improvement, as highlighted in the discussion of attention-based ensemble learning frameworks for finance and the insights on automating sales forecasts through market integration.

Conclusion

DeepClair: Utilizing Market Forecasts for Effective Portfolio Selection proposes a novel deep reinforcement learning framework that integrates various market forecasting models to improve portfolio selection performance. The key innovation is the recognition that financial markets are complex and dynamic, and that incorporating diverse market insights can lead to more effective portfolio management strategies.

The results presented in the paper demonstrate the potential of this approach, but also highlight the need for further research to address the limitations, such as the reliance on accurate forecasts and the computational challenges. As the field of AI-driven finance continues to evolve, frameworks like DeepClair may play an increasingly important role in helping investors and financial institutions navigate the complexities of modern markets.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

DeepClair: Utilizing Market Forecasts for Effective Portfolio Selection

Donghee Choi, Jinkyu Kim, Mogan Gim, Jinho Lee, Jaewoo Kang

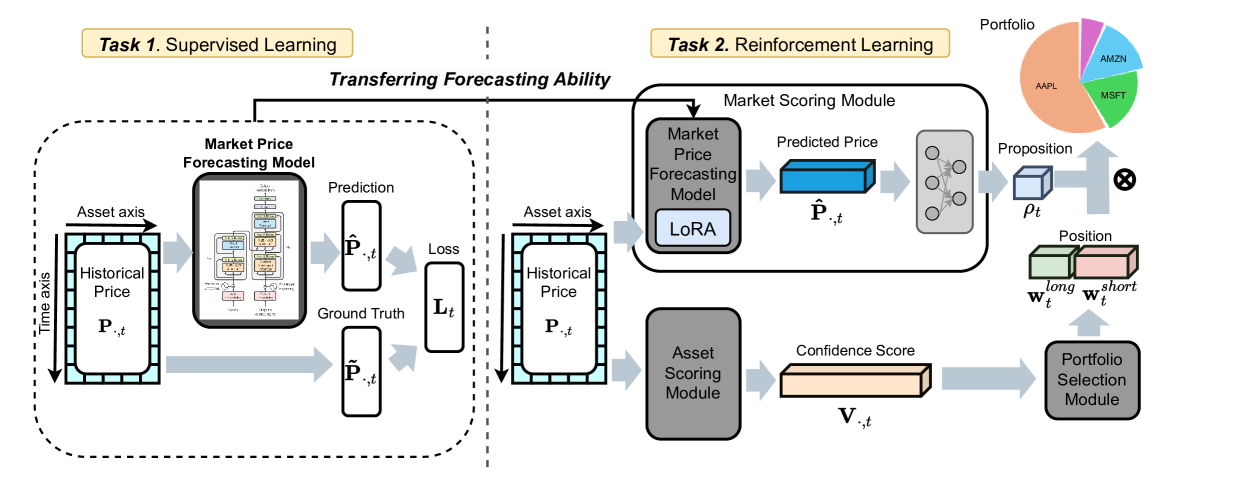

Utilizing market forecasts is pivotal in optimizing portfolio selection strategies. We introduce DeepClair, a novel framework for portfolio selection. DeepClair leverages a transformer-based time-series forecasting model to predict market trends, facilitating more informed and adaptable portfolio decisions. To integrate the forecasting model into a deep reinforcement learning-driven portfolio selection framework, we introduced a two-step strategy: first, pre-training the time-series model on market data, followed by fine-tuning the portfolio selection architecture using this model. Additionally, we investigated the optimization technique, Low-Rank Adaptation (LoRA), to enhance the pre-trained forecasting model for fine-tuning in investment scenarios. This work bridges market forecasting and portfolio selection, facilitating the advancement of investment strategies.

Read more8/19/2024

0

New!A Deep Reinforcement Learning Framework For Financial Portfolio Management

Jinyang Li

In this research paper, we investigate into a paper named A Deep Reinforcement Learning Framework for the Financial Portfolio Management Problem [arXiv:1706.10059]. It is a portfolio management problem which is solved by deep learning techniques. The original paper proposes a financial-model-free reinforcement learning framework, which consists of the Ensemble of Identical Independent Evaluators (EIIE) topology, a Portfolio-Vector Memory (PVM), an Online Stochastic Batch Learning (OSBL) scheme, and a fully exploiting and explicit reward function. Three different instants are used to realize this framework, namely a Convolutional Neural Network (CNN), a basic Recurrent Neural Network (RNN), and a Long Short-Term Memory (LSTM). The performance is then examined by comparing to a number of recently reviewed or published portfolio-selection strategies. We have successfully replicated their implementations and evaluations. Besides, we further apply this framework in the stock market, instead of the cryptocurrency market that the original paper uses. The experiment in the cryptocurrency market is consistent with the original paper, which achieve superior returns. But it doesn't perform as well when applied in the stock market.

Read more9/16/2024

0

Portfolio Management using Deep Reinforcement Learning

Ashish Anil Pawar, Vishnureddy Prashant Muskawar, Ritesh Tiku

Algorithmic trading or Financial robots have been conquering the stock markets with their ability to fathom complex statistical trading strategies. But with the recent development of deep learning technologies, these strategies are becoming impotent. The DQN and A2C models have previously outperformed eminent humans in game-playing and robotics. In our work, we propose a reinforced portfolio manager offering assistance in the allocation of weights to assets. The environment proffers the manager the freedom to go long and even short on the assets. The weight allocation advisements are restricted to the choice of portfolio assets and tested empirically to knock benchmark indices. The manager performs financial transactions in a postulated liquid market without any transaction charges. This work provides the conclusion that the proposed portfolio manager with actions centered on weight allocations can surpass the risk-adjusted returns of conventional portfolio managers.

Read more5/6/2024

📊

0

Data Scaling Effect of Deep Learning in Financial Time Series Forecasting

Chen Liu, Minh-Ngoc Tran, Chao Wang, Richard Gerlach, Robert Kohn

For years, researchers investigated the applications of deep learning in forecasting financial time series. However, they continued to rely on the conventional econometric approach for model training that optimizes the deep learning models on individual assets. This study highlights the importance of global training, where the deep learning model is optimized across a wide spectrum of stocks. Focusing on stock volatility forecasting as an exemplar, we show that global training is not only beneficial but also necessary for deep learning-based financial time series forecasting. We further demonstrate that, given a sufficient amount of training data, a globally trained deep learning model is capable of delivering accurate zero-shot forecasts for any stocks.

Read more6/4/2024