A Deep Reinforcement Learning Framework For Financial Portfolio Management

0

Sign in to get full access

Overview

- This paper proposes a deep reinforcement learning framework for financial portfolio management.

- The approach aims to optimize portfolio returns while considering transaction costs and other constraints.

- Experiments on real-world stock market data demonstrate the framework's effectiveness compared to traditional portfolio optimization methods.

Plain English Explanation

The researchers have developed a deep reinforcement learning framework to help manage financial portfolios. This means they've created a system that uses advanced machine learning techniques to automatically make investment decisions and optimize a portfolio's performance.

The key idea is to train an AI agent to manage a portfolio in a way that maximizes returns, while also considering important factors like transaction costs and other constraints. The agent learns by interacting with a simulated stock market environment and receiving rewards or penalties based on the performance of the portfolio.

Through experiments on real-world stock market data, the researchers show that their portfolio management framework outperforms traditional portfolio optimization methods. This suggests the potential for AI-powered tools to enhance financial decision-making and portfolio management.

Technical Explanation

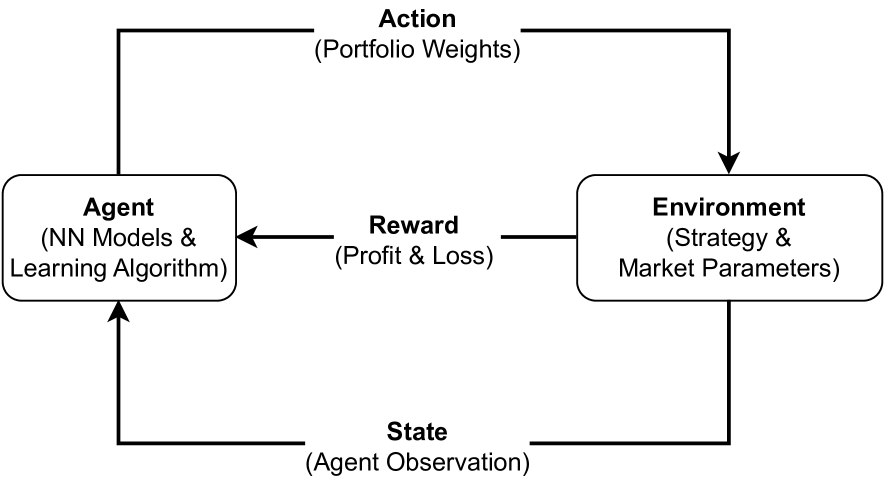

The paper proposes a deep reinforcement learning framework for financial portfolio management. The key components of the framework are:

-

State representation: The current state of the portfolio, including asset weights, account balance, and other relevant features, is encoded as the input to the reinforcement learning agent.

-

Action space: The agent can take actions to adjust the portfolio, such as buying, selling, or holding different assets.

-

Reward function: The agent receives rewards based on the portfolio's performance, considering factors like transaction costs and other constraints.

-

Learning algorithm: The agent uses a deep neural network to learn an optimal policy for managing the portfolio, updating its weights through reinforcement learning.

The researchers evaluate their portfolio management framework on real-world stock market data and compare it to traditional portfolio optimization methods. The results demonstrate the framework's ability to generate higher returns while considering the practical constraints of portfolio management.

Critical Analysis

The paper provides a detailed and technical explanation of the deep reinforcement learning framework for portfolio management, which is a promising approach for enhancing financial decision-making. However, some potential limitations and areas for further research are:

-

Generalizability: The experiments are conducted on a specific stock market dataset, and further testing on other markets or asset classes would be needed to assess the framework's broader applicability.

-

Interpretability: Explainable AI techniques could be explored to improve the transparency and interpretability of the agent's decision-making process, which is crucial for financial applications.

-

Multi-agent considerations: The paper focuses on a single-agent framework, but incorporating multiple agents with different objectives or strategies could lead to more robust and adaptive portfolio management solutions.

Overall, the proposed deep reinforcement learning framework represents an interesting and promising approach to financial portfolio management, but further research and development may be needed to address potential limitations and enhance its practical impact.

Conclusion

This paper presents a deep reinforcement learning framework for financial portfolio management that aims to optimize portfolio returns while considering practical constraints. The experimental results demonstrate the framework's effectiveness compared to traditional portfolio optimization methods, suggesting the potential for AI-powered tools to enhance financial decision-making.

While the technical details of the framework are compelling, the paper also highlights areas for further research, such as improving the framework's generalizability, interpretability, and multi-agent capabilities. Continued advancements in this direction could lead to more robust and impactful portfolio management solutions that benefit individual investors, financial institutions, and the broader economy.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

New!A Deep Reinforcement Learning Framework For Financial Portfolio Management

Jinyang Li

In this research paper, we investigate into a paper named A Deep Reinforcement Learning Framework for the Financial Portfolio Management Problem [arXiv:1706.10059]. It is a portfolio management problem which is solved by deep learning techniques. The original paper proposes a financial-model-free reinforcement learning framework, which consists of the Ensemble of Identical Independent Evaluators (EIIE) topology, a Portfolio-Vector Memory (PVM), an Online Stochastic Batch Learning (OSBL) scheme, and a fully exploiting and explicit reward function. Three different instants are used to realize this framework, namely a Convolutional Neural Network (CNN), a basic Recurrent Neural Network (RNN), and a Long Short-Term Memory (LSTM). The performance is then examined by comparing to a number of recently reviewed or published portfolio-selection strategies. We have successfully replicated their implementations and evaluations. Besides, we further apply this framework in the stock market, instead of the cryptocurrency market that the original paper uses. The experiment in the cryptocurrency market is consistent with the original paper, which achieve superior returns. But it doesn't perform as well when applied in the stock market.

Read more9/16/2024

0

Portfolio Management using Deep Reinforcement Learning

Ashish Anil Pawar, Vishnureddy Prashant Muskawar, Ritesh Tiku

Algorithmic trading or Financial robots have been conquering the stock markets with their ability to fathom complex statistical trading strategies. But with the recent development of deep learning technologies, these strategies are becoming impotent. The DQN and A2C models have previously outperformed eminent humans in game-playing and robotics. In our work, we propose a reinforced portfolio manager offering assistance in the allocation of weights to assets. The environment proffers the manager the freedom to go long and even short on the assets. The weight allocation advisements are restricted to the choice of portfolio assets and tested empirically to knock benchmark indices. The manager performs financial transactions in a postulated liquid market without any transaction charges. This work provides the conclusion that the proposed portfolio manager with actions centered on weight allocations can surpass the risk-adjusted returns of conventional portfolio managers.

Read more5/6/2024

0

Optimizing Portfolio with Two-Sided Transactions and Lending: A Reinforcement Learning Framework

Ali Habibnia, Mahdi Soltanzadeh

This study presents a Reinforcement Learning (RL)-based portfolio management model tailored for high-risk environments, addressing the limitations of traditional RL models and exploiting market opportunities through two-sided transactions and lending. Our approach integrates a new environmental formulation with a Profit and Loss (PnL)-based reward function, enhancing the RL agent's ability in downside risk management and capital optimization. We implemented the model using the Soft Actor-Critic (SAC) agent with a Convolutional Neural Network with Multi-Head Attention (CNN-MHA). This setup effectively manages a diversified 12-crypto asset portfolio in the Binance perpetual futures market, leveraging USDT for both granting and receiving loans and rebalancing every 4 hours, utilizing market data from the preceding 48 hours. Tested over two 16-month periods of varying market volatility, the model significantly outperformed benchmarks, particularly in high-volatility scenarios, achieving higher return-to-risk ratios and demonstrating robust profitability. These results confirm the model's effectiveness in leveraging market dynamics and managing risks in volatile environments like the cryptocurrency market.

Read more8/13/2024

0

Explainable Post hoc Portfolio Management Financial Policy of a Deep Reinforcement Learning agent

Alejandra de la Rica Escudero, Eduardo C. Garrido-Merchan, Maria Coronado-Vaca

Financial portfolio management investment policies computed quantitatively by modern portfolio theory techniques like the Markowitz model rely on a set on assumptions that are not supported by data in high volatility markets. Hence, quantitative researchers are looking for alternative models to tackle this problem. Concretely, portfolio management is a problem that has been successfully addressed recently by Deep Reinforcement Learning (DRL) approaches. In particular, DRL algorithms train an agent by estimating the distribution of the expected reward of every action performed by an agent given any financial state in a simulator. However, these methods rely on Deep Neural Networks model to represent such a distribution, that although they are universal approximator models, they cannot explain its behaviour, given by a set of parameters that are not interpretable. Critically, financial investors policies require predictions to be interpretable, so DRL agents are not suited to follow a particular policy or explain their actions. In this work, we developed a novel Explainable Deep Reinforcement Learning (XDRL) approach for portfolio management, integrating the Proximal Policy Optimization (PPO) with the model agnostic explainable techniques of feature importance, SHAP and LIME to enhance transparency in prediction time. By executing our methodology, we can interpret in prediction time the actions of the agent to assess whether they follow the requisites of an investment policy or to assess the risk of following the agent suggestions. To the best of our knowledge, our proposed approach is the first explainable post hoc portfolio management financial policy of a DRL agent. We empirically illustrate our methodology by successfully identifying key features influencing investment decisions, which demonstrate the ability to explain the agent actions in prediction time.

Read more7/22/2024