Feature-Driven Strategies for Trading Wind Power and Hydrogen

0

🌐

Sign in to get full access

Overview

- This paper develops a new model for hybrid power plants that can make optimal decisions about trading wind power and hydrogen in the day-ahead stage.

- The model uses historical data and forecasts to inform these trading decisions.

- The paper also proposes a real-time adjustment strategy for hydrogen production.

- The authors find their approach performs very close to an ideal benchmark with perfect information.

Plain English Explanation

Hybrid power plants can generate electricity from multiple sources, like wind and hydrogen. This paper creates a new way for these plants to plan their wind power and hydrogen trading in advance. The model uses data like past wind power forecasts to help the plant make smart decisions about how much wind power and hydrogen to buy and sell a day ahead of time.

The paper also suggests a real-time adjustment strategy to fine-tune the hydrogen production as needed. The results show this approach performs almost as well as having perfect information about the future, which is impossible in the real world. Overall, the new model helps hybrid power plants maximize their profits by optimizing their trading decisions.

Technical Explanation

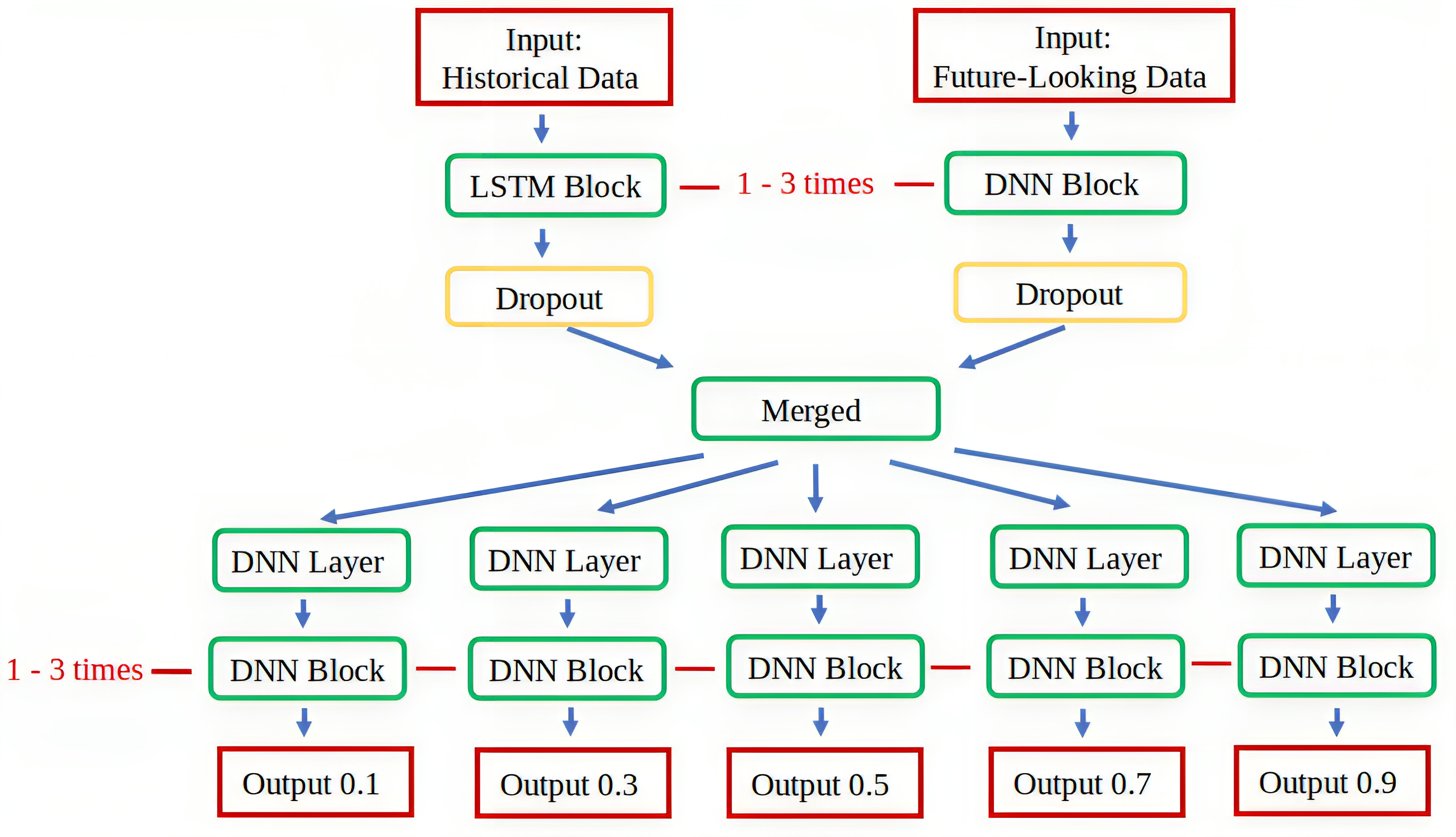

The paper develops a "feature-driven" model for hybrid power plants. This means the model uses available contextual information, like historical wind power forecasts, to inform optimal trading decisions for wind power and hydrogen in the day-ahead market.

The authors explore different variations of this feature-driven approach, including one where the trading policies depend on price domains, resulting in a price-quantity bidding curve. They also propose a real-time adjustment strategy to modify hydrogen production as needed.

The numerical results demonstrate that the final profits from this feature-driven trading mechanism, combined with real-time hydrogen adjustments, closely matches an idealized benchmark with perfect future information.

Critical Analysis

The paper provides a comprehensive technical solution for optimizing hybrid power plant operations, but it does not address potential challenges in implementing such a system in the real world. For example, the reliance on historical forecasts assumes these will be accurate and available, which may not always be the case.

Additionally, the real-time adjustment strategy for hydrogen production is not fully fleshed out, and its feasibility and effectiveness would need to be further validated. The authors also do not discuss potential market or regulatory barriers that could impact the adoption of such an approach.

Overall, the research presents a promising modeling framework, but more work is needed to address practical considerations and ensure the proposed solutions are robust and viable in real-world hybrid power plant operations.

Conclusion

This paper develops an advanced model to help hybrid power plants make optimal trading decisions for wind power and hydrogen in the day-ahead market. By incorporating historical data and forecasts, the model can guide these plants to maximize their profits, performing nearly as well as having perfect future information.

While the technical approach is well-designed, further research is needed to address real-world implementation challenges. Nonetheless, this work represents an important step forward in enhancing the operational efficiency and profitability of hybrid power systems, which will be crucial as renewable energy sources continue to play a larger role in the global energy mix.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

🌐

0

Feature-Driven Strategies for Trading Wind Power and Hydrogen

Emil Helgren, Jalal Kazempour, Lesia Mitridati

This paper develops a feature-driven model for hybrid power plants, enabling them to exploit available contextual information such as historical forecasts of wind power, and make optimal wind power and hydrogen trading decisions in the day-ahead stage. For that, we develop different variations of feature-driven linear policies, including a variation where policies depend on price domains, resulting in a price-quantity bidding curve. In addition, we propose a real-time adjustment strategy for hydrogen production. Our numerical results show that the final profit obtained from our proposed feature-driven trading mechanism in the day-ahead stage together with the real-time adjustment strategy is very close to that in an ideal benchmark with perfect information.

Read more4/1/2024

0

Optimizing Quantile-based Trading Strategies in Electricity Arbitrage

Ciaran O'Connor, Joseph Collins, Steven Prestwich, Andrea Visentin

Efficiently integrating renewable resources into electricity markets is vital for addressing the challenges of matching real-time supply and demand while reducing the significant energy wastage resulting from curtailments. To address this challenge effectively, the incorporation of storage devices can enhance the reliability and efficiency of the grid, improving market liquidity and reducing price volatility. In short-term electricity markets, participants navigate numerous options, each presenting unique challenges and opportunities, underscoring the critical role of the trading strategy in maximizing profits. This study delves into the optimization of day-ahead and balancing market trading, leveraging quantile-based forecasts. Employing three trading approaches with practical constraints, our research enhances forecast assessment, increases trading frequency, and employs flexible timestamp orders. Our findings underscore the profit potential of simultaneous participation in both day-ahead and balancing markets, especially with larger battery storage systems; despite increased costs and narrower profit margins associated with higher-volume trading, the implementation of high-frequency strategies plays a significant role in maximizing profits and addressing market challenges. Finally, we modelled four commercial battery storage systems and evaluated their economic viability through a scenario analysis, with larger batteries showing a shorter return on investment.

Read more6/21/2024

0

Transformer meets wcDTW to improve real-time battery bids: A new approach to scenario selection

Sujal Bhavsar, Vera Zaychik Moffitt, Justin Appleby

Stochastic battery bidding in real-time energy markets is a nuanced process, with its efficacy depending on the accuracy of forecasts and the representative scenarios chosen for optimization. In this paper, we introduce a pioneering methodology that amalgamates Transformer-based forecasting with weighted constrained Dynamic Time Warping (wcDTW) to refine scenario selection. Our approach harnesses the predictive capabilities of Transformers to foresee Energy prices, while wcDTW ensures the selection of pertinent historical scenarios by maintaining the coherence between multiple uncertain products. Through extensive simulations in the PJM market for July 2023, our method exhibited a 10% increase in revenue compared to the conventional method, highlighting its potential to revolutionize battery bidding strategies in real-time markets.

Read more4/3/2024

0

Forecasting Day-Ahead Electricity Prices in the Integrated Single Electricity Market: Addressing Volatility with Comparative Machine Learning Methods

Ben Harkin, Xueqin Liu

This paper undertakes a comprehensive investigation of electricity price forecasting methods, focused on the Irish Integrated Single Electricity Market, particularly on changes during recent periods of high volatility. The primary objective of this research is to evaluate and compare the performance of various forecasting models, ranging from traditional machine learning models to more complex neural networks, as well as the impact of different lengths of training periods. The performance metrics, mean absolute error, root mean square error, and relative mean absolute error, are utilized to assess and compare the accuracy of each model. A comprehensive set of input features was investigated and selected from data recorded between October 2018 and September 2022. The paper demonstrates that the daily EU Natural Gas price is a more useful feature for electricity price forecasting in Ireland than the daily Henry Hub Natural Gas price. This study also shows that the correlation of features to the day-ahead market price has changed in recent years. The price of natural gas on the day and the amount of wind energy on the grid that hour are significantly more important than any other features. More specifically speaking, the input fuel for electricity has become a more important driver of the price of it, than the total generation or demand. In addition, it can be seen that System Non-Synchronous Penetration (SNSP) is highly correlated with the day-ahead market price, and that renewables are pushing down the price of electricity.

Read more8/13/2024