A Framework for Empowering Reinforcement Learning Agents with Causal Analysis: Enhancing Automated Cryptocurrency Trading

0

Sign in to get full access

Overview

- This paper proposes a framework that integrates causal analysis with reinforcement learning to enhance automated cryptocurrency trading.

- The key idea is to leverage causal relationships between market factors and asset prices to guide the reinforcement learning agent's decision-making process.

- The framework is designed to help the agent better understand the underlying dynamics of the cryptocurrency market and make more informed trading decisions.

Plain English Explanation

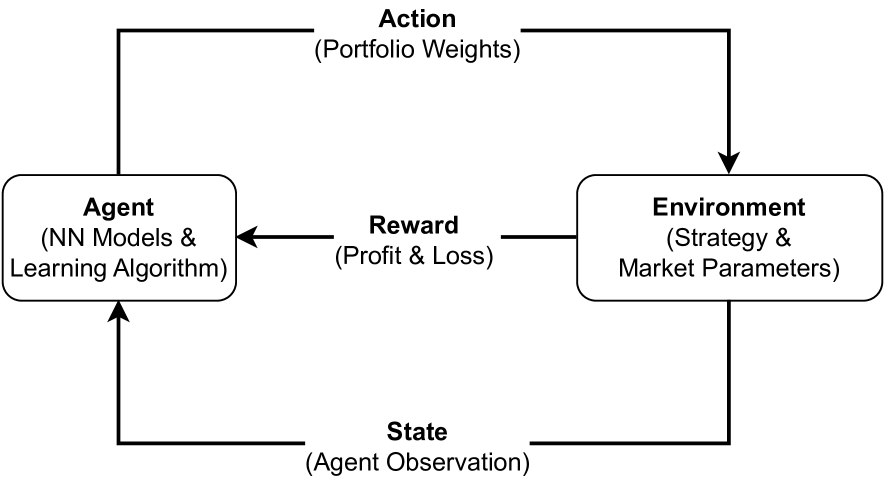

The paper presents a new approach to improve automated cryptocurrency trading using a combination of reinforcement learning and causal analysis. Reinforcement learning is a type of machine learning where an agent learns by interacting with an environment and receiving rewards or penalties for its actions.

The main challenge in applying reinforcement learning to cryptocurrency trading is that the market dynamics are complex and can be influenced by many different factors. This makes it difficult for the agent to learn an optimal trading strategy based solely on historical price data.

To address this, the researchers integrate causal analysis into the reinforcement learning framework. Causal analysis is a way of understanding how different variables in a system are related and how changes in one variable can affect others. By incorporating causal relationships between market factors and asset prices, the reinforcement learning agent can gain a deeper understanding of the underlying drivers of the cryptocurrency market.

This allows the agent to make more informed and strategic trading decisions, potentially leading to improved trading performance and profitability. The researchers test their framework on real-world cryptocurrency data and demonstrate its effectiveness compared to traditional reinforcement learning approaches.

Technical Explanation

The paper proposes a framework that combines reinforcement learning with causal analysis to enhance automated cryptocurrency trading. The key components of the framework are:

-

Causal Analysis: The researchers use causal discovery algorithms to identify the causal relationships between various market factors (e.g., trading volume, volatility, macroeconomic indicators) and the target cryptocurrency's price. This helps the agent understand how changes in these factors can influence the asset's price.

-

Reinforcement Learning: The agent is trained using a reinforcement learning algorithm, which enables it to learn an optimal trading strategy by interacting with the market environment and receiving rewards or penalties for its actions.

-

Causal-Aware Reward Function: The causal relationships identified in the first step are used to design a more informative reward function for the reinforcement learning agent. This reward function incorporates the agent's understanding of the underlying market dynamics, guiding it towards making more informed and profitable trading decisions.

The researchers evaluate their framework using real-world cryptocurrency data and compare its performance to traditional reinforcement learning approaches. They find that the causal-aware framework outperforms the baseline methods, demonstrating the benefits of integrating causal analysis into the reinforcement learning process for automated cryptocurrency trading.

Critical Analysis

The paper presents a novel and promising approach to improving automated cryptocurrency trading by leveraging causal analysis. The key strength of the framework is its ability to help the reinforcement learning agent better understand the underlying market dynamics, which can lead to more informed and profitable trading decisions.

However, the paper does not address several important limitations and potential issues:

-

Causal Model Accuracy: The effectiveness of the framework heavily depends on the accuracy of the causal relationships identified by the causal discovery algorithms. If these causal models are inaccurate or incomplete, they could lead to suboptimal trading decisions by the reinforcement learning agent.

-

Market Complexity and Nonstationarity: Cryptocurrency markets are highly complex and can exhibit significant nonstationarity, where the underlying relationships and dynamics may change over time. The paper does not discuss how the framework might handle these challenges and adapt to changes in the market.

-

Overfitting and Generalization: The researchers should have conducted more rigorous out-of-sample testing to ensure that the framework can generalize well to new, unseen market conditions, and not just perform well on the training data.

-

Interpretability and Explainability: While the causal analysis component provides some level of interpretability, the paper could have discussed the importance of making the trading decisions more transparent and explainable to human traders and analysts.

Overall, the proposed framework is a valuable contribution to the field of automated cryptocurrency trading, but further research is needed to address the limitations and potential issues mentioned above.

Conclusion

This paper presents a novel framework that integrates causal analysis with reinforcement learning to enhance automated cryptocurrency trading. By leveraging the insights gained from causal relationships between market factors and asset prices, the reinforcement learning agent can make more informed and strategic trading decisions.

The results demonstrate the potential benefits of this approach, suggesting that incorporating causal analysis into the reinforcement learning process can lead to improved trading performance and profitability. However, the framework also has some limitations, such as the accuracy of the causal models and the challenges of handling market complexity and nonstationarity.

Moving forward, further research is needed to address these limitations and explore ways to make the trading decisions more interpretable and explainable. Nonetheless, this paper represents an important step towards developing more sophisticated and effective automated trading systems for the cryptocurrency market.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

A Framework for Empowering Reinforcement Learning Agents with Causal Analysis: Enhancing Automated Cryptocurrency Trading

Rasoul Amirzadeh, Dhananjay Thiruvady, Asef Nazari, Mong Shan Ee

Despite advances in artificial intelligence-enhanced trading methods, developing a profitable automated trading system remains challenging in the rapidly evolving cryptocurrency market. This research focuses on developing a reinforcement learning (RL) framework to tackle the complexities of trading five prominent altcoins: Binance Coin, Ethereum, Litecoin, Ripple, and Tether. To this end, we present the CausalReinforceNet~(CRN) framework, which integrates both Bayesian and dynamic Bayesian network techniques to empower the RL agent in trade decision-making. We develop two agents using the framework based on distinct RL algorithms to analyse performance compared to the Buy-and-Hold benchmark strategy and a baseline RL model. The results indicate that our framework surpasses both models in profitability, highlighting CRN's consistent superiority, although the level of effectiveness varies across different cryptocurrencies.

Read more8/21/2024

0

Reinforcement Learning Pair Trading: A Dynamic Scaling approach

Hongshen Yang, Avinash Malik

Cryptocurrency is a cryptography-based digital asset with extremely volatile prices. Around $70 billion worth of crypto-currency is traded daily on exchanges. Trading crypto-currency is difficult due to the inherent volatility of the crypto-market. In this work, we want to test the hypothesis: Can techniques from artificial intelligence help with algorithmically trading cryptocurrencies?. In order to address this question, we combine Reinforcement Learning (RL) with pair trading. Pair trading is a statistical arbitrage trading technique which exploits the price difference between statistically correlated assets. We train reinforcement learners to determine when and how to trade pairs of cryptocurrencies. We develop new reward shaping and observation/action spaces for reinforcement learning. We performed experiments with the developed reinforcement learner on pairs of BTC-GBP and BTC-EUR data separated by 1-minute intervals (n = 263,520). The traditional non-RL pair trading technique achieved an annualised profit of 8.33%, while the proposed RL-based pair trading technique achieved annualised profits from 9.94% - 31.53%, depending upon the RL learner. Our results show that RL can significantly outperform manual and traditional pair trading techniques when applied to volatile markets such as cryptocurrencies.

Read more7/24/2024

0

Optimizing Portfolio with Two-Sided Transactions and Lending: A Reinforcement Learning Framework

Ali Habibnia, Mahdi Soltanzadeh

This study presents a Reinforcement Learning (RL)-based portfolio management model tailored for high-risk environments, addressing the limitations of traditional RL models and exploiting market opportunities through two-sided transactions and lending. Our approach integrates a new environmental formulation with a Profit and Loss (PnL)-based reward function, enhancing the RL agent's ability in downside risk management and capital optimization. We implemented the model using the Soft Actor-Critic (SAC) agent with a Convolutional Neural Network with Multi-Head Attention (CNN-MHA). This setup effectively manages a diversified 12-crypto asset portfolio in the Binance perpetual futures market, leveraging USDT for both granting and receiving loans and rebalancing every 4 hours, utilizing market data from the preceding 48 hours. Tested over two 16-month periods of varying market volatility, the model significantly outperformed benchmarks, particularly in high-volatility scenarios, achieving higher return-to-risk ratios and demonstrating robust profitability. These results confirm the model's effectiveness in leveraging market dynamics and managing risks in volatile environments like the cryptocurrency market.

Read more8/13/2024

🤿

0

A Deep Reinforcement Learning Approach for Trading Optimization in the Forex Market with Multi-Agent Asynchronous Distribution

Davoud Sarani, Dr. Parviz Rashidi-Khazaee

In today's forex market traders increasingly turn to algorithmic trading, leveraging computers to seek more profits. Deep learning techniques as cutting-edge advancements in machine learning, capable of identifying patterns in financial data. Traders utilize these patterns to execute more effective trades, adhering to algorithmic trading rules. Deep reinforcement learning methods (DRL), by directly executing trades based on identified patterns and assessing their profitability, offer advantages over traditional DL approaches. This research pioneers the application of a multi-agent (MA) RL framework with the state-of-the-art Asynchronous Advantage Actor-Critic (A3C) algorithm. The proposed method employs parallel learning across multiple asynchronous workers, each specialized in trading across multiple currency pairs to explore the potential for nuanced strategies tailored to different market conditions and currency pairs. Two different A3C with lock and without lock MA model was proposed and trained on single currency and multi-currency. The results indicate that both model outperform on Proximal Policy Optimization model. A3C with lock outperforms other in single currency training scenario and A3C without Lock outperforms other in multi-currency scenario. The findings demonstrate that this approach facilitates broader and faster exploration of different currency pairs, significantly enhancing trading returns. Additionally, the agent can learn a more profitable trading strategy in a shorter time.

Read more5/31/2024