Optimizing Portfolio with Two-Sided Transactions and Lending: A Reinforcement Learning Framework

0

Sign in to get full access

Overview

- Optimizes investment portfolio using reinforcement learning with two-sided transactions and lending

- Develops a framework that learns to make optimal trading decisions to maximize returns

- Considers both buying and selling of assets, as well as lending, to improve portfolio performance

Plain English Explanation

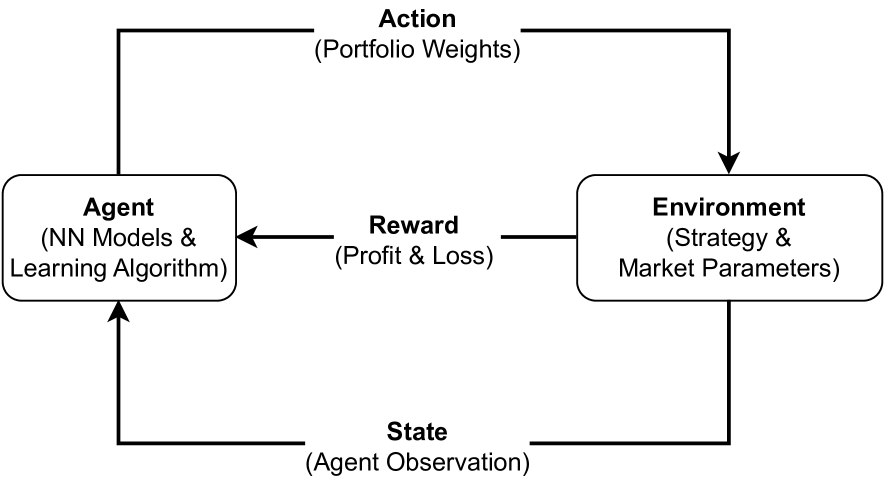

This research paper presents a reinforcement learning framework for optimizing an investment portfolio. Unlike traditional portfolio management approaches, this framework allows for two-sided transactions - both buying and selling of assets. It also incorporates the ability to lend assets, which can generate additional returns.

The key idea is to train an intelligent agent, using reinforcement learning techniques, to learn the optimal trading strategy. The agent interacts with a simulated investment environment, receives rewards based on portfolio performance, and gradually learns to make trading decisions that maximize returns over time.

By enabling both buying and selling, as well as lending, the framework provides the agent with more flexibility to navigate market conditions and identify profitable opportunities. This can lead to improved portfolio performance compared to more limited strategies that only allow one-sided transactions.

Technical Explanation

The proposed framework consists of several key components:

-

Investment Environment: A simulated environment that models the dynamics of asset prices, trading opportunities, and lending/borrowing rates. This environment provides the necessary signals and feedback for the reinforcement learning agent to learn from.

-

Reinforcement Learning Agent: The agent is responsible for observing the current state of the investment environment (e.g., asset prices, portfolio composition) and taking actions (buying, selling, lending) to maximize the cumulative reward, which is typically defined as the growth of the investment portfolio over time.

-

Two-Sided Transactions: The agent is able to both buy and sell assets, allowing it to take advantage of market fluctuations and potentially generate profits from both rising and falling asset prices.

-

Lending: The agent can also lend out assets from the portfolio, earning additional returns through lending fees. This provides another revenue stream to complement the trading of assets.

-

Learning Algorithm: The reinforcement learning algorithm, such as Deep Q-Learning or Actor-Critic, is responsible for training the agent to learn the optimal trading and lending strategies over time.

Through extensive simulation and training, the reinforcement learning agent learns to make decisions that maximize the long-term growth of the investment portfolio, taking advantage of the flexibility provided by two-sided transactions and lending.

Critical Analysis

The research paper provides a promising approach to portfolio optimization, but there are a few potential caveats and areas for further exploration:

-

Realistic Market Conditions: While the simulated environment aims to capture the dynamics of asset prices and trading, real-world financial markets can be much more complex and volatile. Careful consideration should be given to how well the simulation can capture the nuances of actual market behavior.

-

Computational Complexity: Reinforcement learning algorithms can be computationally intensive, especially when dealing with a large number of assets and complex trading strategies. The scalability of the approach to real-world portfolio management with a diverse set of assets may be a challenge.

-

Overfitting and Generalization: As with any machine learning model, there is a risk of the agent overfitting to the training data and failing to generalize well to new, unseen market conditions. Robust testing and validation procedures would be crucial to ensure the framework's reliability and adaptability.

-

Interpretability and Explainability: The inner workings of the reinforcement learning agent's decision-making process may be opaque, making it difficult to understand and explain the rationale behind the trading and lending decisions. Enhancing the interpretability of the model could improve its acceptance and adoption in the financial industry.

Despite these potential limitations, the proposed framework represents an innovative approach to portfolio optimization that leverages the power of reinforcement learning to navigate complex market dynamics and generate superior investment returns.

Conclusion

This research paper introduces a reinforcement learning-based framework for optimizing investment portfolios. By incorporating two-sided transactions (buying and selling) and lending, the framework provides a more flexible and potentially more effective approach to portfolio management compared to traditional methods.

The key contribution of the work is the development of a reinforcement learning agent that can learn to make optimal trading and lending decisions to maximize the long-term growth of the investment portfolio. This approach has the potential to outperform simpler strategies and generate higher returns for investors.

While the paper highlights several promising aspects of the framework, it also acknowledges the need to address potential challenges related to realistic market simulation, computational complexity, and model interpretability. Continued research and refinement of the approach could further strengthen its practical applicability in the real-world financial domain.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Optimizing Portfolio with Two-Sided Transactions and Lending: A Reinforcement Learning Framework

Ali Habibnia, Mahdi Soltanzadeh

This study presents a Reinforcement Learning (RL)-based portfolio management model tailored for high-risk environments, addressing the limitations of traditional RL models and exploiting market opportunities through two-sided transactions and lending. Our approach integrates a new environmental formulation with a Profit and Loss (PnL)-based reward function, enhancing the RL agent's ability in downside risk management and capital optimization. We implemented the model using the Soft Actor-Critic (SAC) agent with a Convolutional Neural Network with Multi-Head Attention (CNN-MHA). This setup effectively manages a diversified 12-crypto asset portfolio in the Binance perpetual futures market, leveraging USDT for both granting and receiving loans and rebalancing every 4 hours, utilizing market data from the preceding 48 hours. Tested over two 16-month periods of varying market volatility, the model significantly outperformed benchmarks, particularly in high-volatility scenarios, achieving higher return-to-risk ratios and demonstrating robust profitability. These results confirm the model's effectiveness in leveraging market dynamics and managing risks in volatile environments like the cryptocurrency market.

Read more8/13/2024

0

A Deep Reinforcement Learning Framework For Financial Portfolio Management

Jinyang Li

In this research paper, we investigate into a paper named A Deep Reinforcement Learning Framework for the Financial Portfolio Management Problem [arXiv:1706.10059]. It is a portfolio management problem which is solved by deep learning techniques. The original paper proposes a financial-model-free reinforcement learning framework, which consists of the Ensemble of Identical Independent Evaluators (EIIE) topology, a Portfolio-Vector Memory (PVM), an Online Stochastic Batch Learning (OSBL) scheme, and a fully exploiting and explicit reward function. Three different instants are used to realize this framework, namely a Convolutional Neural Network (CNN), a basic Recurrent Neural Network (RNN), and a Long Short-Term Memory (LSTM). The performance is then examined by comparing to a number of recently reviewed or published portfolio-selection strategies. We have successfully replicated their implementations and evaluations. Besides, we further apply this framework in the stock market, instead of the cryptocurrency market that the original paper uses. The experiment in the cryptocurrency market is consistent with the original paper, which achieve superior returns. But it doesn't perform as well when applied in the stock market.

Read more9/16/2024

0

Portfolio Management using Deep Reinforcement Learning

Ashish Anil Pawar, Vishnureddy Prashant Muskawar, Ritesh Tiku

Algorithmic trading or Financial robots have been conquering the stock markets with their ability to fathom complex statistical trading strategies. But with the recent development of deep learning technologies, these strategies are becoming impotent. The DQN and A2C models have previously outperformed eminent humans in game-playing and robotics. In our work, we propose a reinforced portfolio manager offering assistance in the allocation of weights to assets. The environment proffers the manager the freedom to go long and even short on the assets. The weight allocation advisements are restricted to the choice of portfolio assets and tested empirically to knock benchmark indices. The manager performs financial transactions in a postulated liquid market without any transaction charges. This work provides the conclusion that the proposed portfolio manager with actions centered on weight allocations can surpass the risk-adjusted returns of conventional portfolio managers.

Read more5/6/2024

0

A Framework for Empowering Reinforcement Learning Agents with Causal Analysis: Enhancing Automated Cryptocurrency Trading

Rasoul Amirzadeh, Dhananjay Thiruvady, Asef Nazari, Mong Shan Ee

Despite advances in artificial intelligence-enhanced trading methods, developing a profitable automated trading system remains challenging in the rapidly evolving cryptocurrency market. This research focuses on developing a reinforcement learning (RL) framework to tackle the complexities of trading five prominent altcoins: Binance Coin, Ethereum, Litecoin, Ripple, and Tether. To this end, we present the CausalReinforceNet~(CRN) framework, which integrates both Bayesian and dynamic Bayesian network techniques to empower the RL agent in trade decision-making. We develop two agents using the framework based on distinct RL algorithms to analyse performance compared to the Buy-and-Hold benchmark strategy and a baseline RL model. The results indicate that our framework surpasses both models in profitability, highlighting CRN's consistent superiority, although the level of effectiveness varies across different cryptocurrencies.

Read more8/21/2024