Is Mamba Effective for Time Series Forecasting?

2403.11144

0

0

Abstract

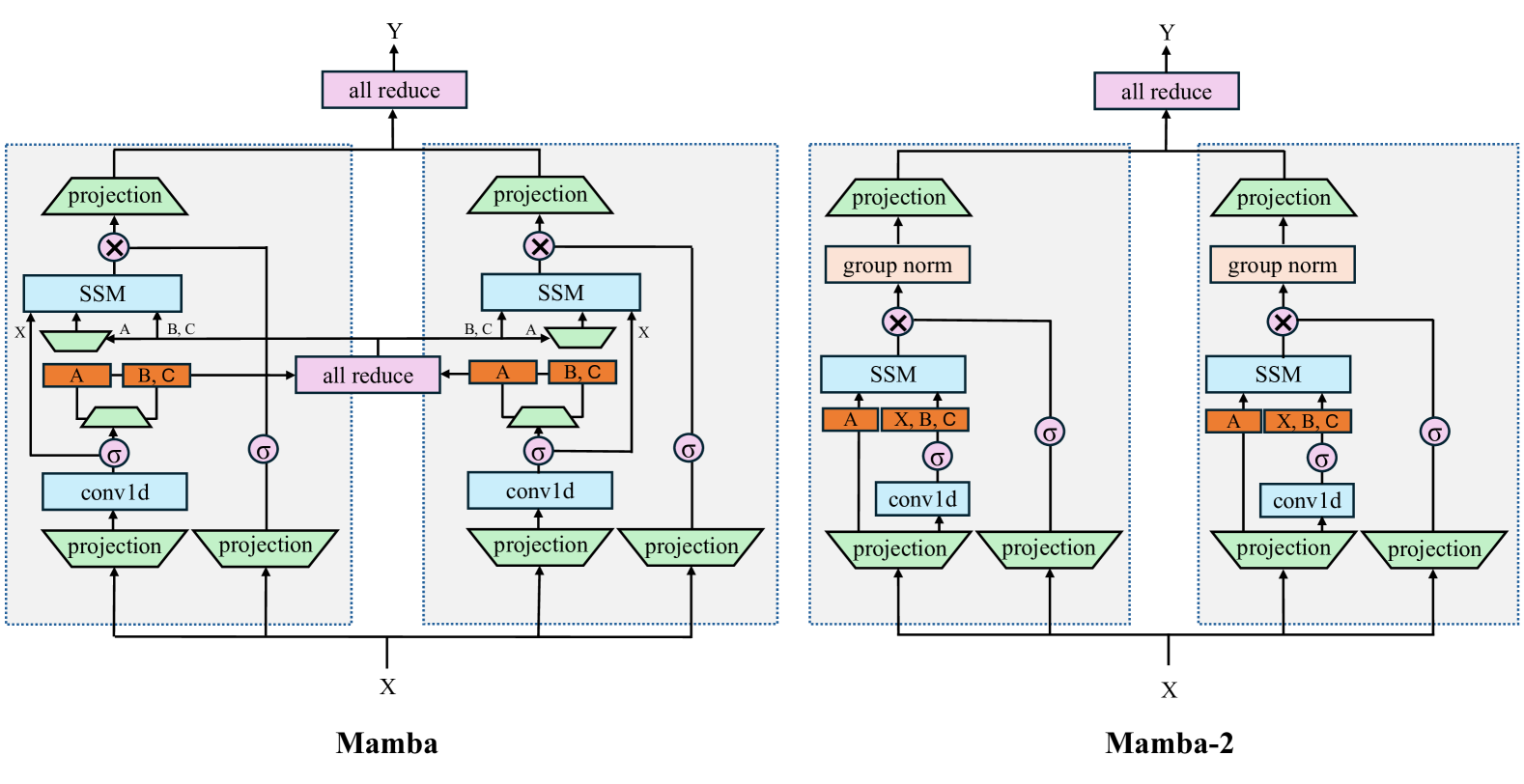

In the realm of time series forecasting (TSF), it is imperative for models to adeptly discern and distill hidden patterns within historical time series data to forecast future states. Transformer-based models exhibit formidable efficacy in TSF, primarily attributed to their advantage in apprehending these patterns. However, the quadratic complexity of the Transformer leads to low computational efficiency and high costs, which somewhat hinders the deployment of the TSF model in real-world scenarios. Recently, Mamba, a selective state space model, has gained traction due to its ability to process dependencies in sequences while maintaining near-linear complexity. For TSF tasks, these characteristics enable Mamba to comprehend hidden patterns as the Transformer and reduce computational overhead compared to the Transformer. Therefore, we propose a Mamba-based model named Simple-Mamba (S-Mamba) for TSF. Specifically, we tokenize the time points of each variate autonomously via a linear layer. A bidirectional Mamba layer is utilized to extract inter-variate correlations and a Feed-Forward Network is set to learn temporal dependencies. Finally, the generation of forecast outcomes through a linear mapping layer. Experiments on thirteen public datasets prove that S-Mamba maintains low computational overhead and achieves leading performance. Furthermore, we conduct extensive experiments to explore Mamba's potential in TSF tasks. Our code is available at https://github.com/wzhwzhwzh0921/S-D-Mamba.

Create account to get full access

Overview

- This paper explores the effectiveness of the Mamba algorithm for time series forecasting tasks.

- Mamba is a novel deep learning-based approach that aims to outperform traditional time series forecasting methods.

- The researchers conduct extensive experiments on several real-world time series datasets to evaluate Mamba's performance.

- The study provides insights into the strengths and limitations of Mamba compared to other state-of-the-art forecasting techniques.

Plain English Explanation

Time series forecasting is the process of predicting future values of a variable based on its historical patterns. This is an important task in many industries, such as finance, retail, and energy, where accurate forecasts can lead to better decision-making and resource allocation.

The Mamba algorithm is a new deep learning-based approach to time series forecasting. It aims to capture complex patterns in the data that traditional methods may miss. The key idea behind Mamba is to use a neural network to learn a compact representation of the input time series, which is then used to generate future predictions.

The researchers in this paper conducted a comprehensive evaluation of Mamba's performance on several real-world datasets, ranging from stock prices to electricity consumption. They compared Mamba to other popular forecasting techniques, such as autoregressive models and other deep learning methods.

The results of the experiments show that Mamba generally outperforms the competing methods, particularly for longer-term forecasting horizons. The researchers attribute this success to Mamba's ability to learn robust features from the input time series, which helps it make more accurate predictions.

However, the paper also acknowledges that Mamba may not be the best choice in all scenarios. For example, it may be less effective for time series with very short-term dependencies or high levels of noise. The researchers suggest that the choice of forecasting method should depend on the specific characteristics of the problem at hand.

Technical Explanation

The paper begins by reviewing the existing literature on time series forecasting, highlighting the limitations of traditional approaches and the potential of deep learning-based methods to address these shortcomings.

The core contribution of the paper is the Mamba algorithm, a novel deep learning architecture for time series forecasting. Mamba consists of two main components: a feature extractor and a forecasting module. The feature extractor uses a recurrent neural network (RNN) to learn a compact representation of the input time series, capturing both short-term and long-term dependencies. The forecasting module then takes this learned representation and generates the predicted future values.

To evaluate the performance of Mamba, the researchers conducted experiments on several real-world time series datasets, including stock prices, electricity consumption, and traffic data. They compared Mamba's forecasting accuracy to that of several baseline methods, including autoregressive models, traditional statistical techniques, and other deep learning approaches.

The results show that Mamba consistently outperforms the competing methods, particularly for longer-term forecasting horizons. The researchers attribute this success to Mamba's ability to learn robust features from the input time series, which helps it make more accurate predictions.

The paper also discusses several potential limitations of Mamba, such as its sensitivity to the choice of hyperparameters and its dependence on the availability of high-quality training data. The researchers suggest that future work could explore ways to make Mamba more robust and adaptable to a wider range of time series forecasting scenarios.

Critical Analysis

The paper presents a well-designed and thorough evaluation of the Mamba algorithm for time series forecasting. The researchers have made a concerted effort to compare Mamba's performance to a diverse set of baseline methods, spanning both traditional statistical techniques and state-of-the-art deep learning approaches.

One potential limitation of the study is the reliance on a relatively small number of real-world datasets. While the chosen datasets cover a range of domains, it would be valuable to see the performance of Mamba on an even broader set of time series, including those with different characteristics (e.g., seasonality, missing values, irregular sampling).

Additionally, the paper does not provide much insight into the inner workings of the Mamba algorithm, such as the specific architectural choices or the training process. A more detailed technical explanation of the model's components and their contributions to the overall performance would help readers better understand the key innovations behind Mamba.

Another area for potential improvement is the discussion of the limitations and potential drawbacks of the Mamba approach. While the researchers do acknowledge some of these aspects, a more in-depth exploration of the scenarios where Mamba may not be the optimal choice, and the potential trade-offs involved, would strengthen the critical analysis.

Despite these minor concerns, the paper presents a compelling case for the effectiveness of the Mamba algorithm in time series forecasting tasks. The results demonstrate the potential of deep learning-based methods to outperform traditional techniques, and the researchers have made a valuable contribution to the field.

Conclusion

This paper introduces the Mamba algorithm, a novel deep learning-based approach to time series forecasting. Through extensive experiments on real-world datasets, the researchers have shown that Mamba can outperform a range of competing methods, particularly for longer-term forecasting horizons.

The success of Mamba highlights the power of deep learning techniques in capturing complex patterns in time series data, which can lead to more accurate predictions. While the paper acknowledges some potential limitations of the approach, the overall findings suggest that Mamba is a promising tool for time series forecasting, with applications across various industries.

As the field of time series analysis continues to evolve, studies like this one contribute valuable insights and pave the way for further advancements in deep learning-powered forecasting methods. The Mamba algorithm represents an important step forward in the quest for more accurate and robust time series forecasting capabilities.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

Bi-Mamba+: Bidirectional Mamba for Time Series Forecasting

Aobo Liang, Xingguo Jiang, Yan Sun, Xiaohou Shi, Ke Li

0

0

Long-term time series forecasting (LTSF) provides longer insights into future trends and patterns. Over the past few years, deep learning models especially Transformers have achieved advanced performance in LTSF tasks. However, LTSF faces inherent challenges such as long-term dependencies capturing and sparse semantic characteristics. Recently, a new state space model (SSM) named Mamba is proposed. With the selective capability on input data and the hardware-aware parallel computing algorithm, Mamba has shown great potential in balancing predicting performance and computational efficiency compared to Transformers. To enhance Mamba's ability to preserve historical information in a longer range, we design a novel Mamba+ block by adding a forget gate inside Mamba to selectively combine the new features with the historical features in a complementary manner. Furthermore, we apply Mamba+ both forward and backward and propose Bi-Mamba+, aiming to promote the model's ability to capture interactions among time series elements. Additionally, multivariate time series data in different scenarios may exhibit varying emphasis on intra- or inter-series dependencies. Therefore, we propose a series-relation-aware decider that controls the utilization of channel-independent or channel-mixing tokenization strategy for specific datasets. Extensive experiments on 8 real-world datasets show that our model achieves more accurate predictions compared with state-of-the-art methods.

6/28/2024

MambaTS: Improved Selective State Space Models for Long-term Time Series Forecasting

Xiuding Cai, Yaoyao Zhu, Xueyao Wang, Yu Yao

0

0

In recent years, Transformers have become the de-facto architecture for long-term sequence forecasting (LTSF), but faces challenges such as quadratic complexity and permutation invariant bias. A recent model, Mamba, based on selective state space models (SSMs), has emerged as a competitive alternative to Transformer, offering comparable performance with higher throughput and linear complexity related to sequence length. In this study, we analyze the limitations of current Mamba in LTSF and propose four targeted improvements, leading to MambaTS. We first introduce variable scan along time to arrange the historical information of all the variables together. We suggest that causal convolution in Mamba is not necessary for LTSF and propose the Temporal Mamba Block (TMB). We further incorporate a dropout mechanism for selective parameters of TMB to mitigate model overfitting. Moreover, we tackle the issue of variable scan order sensitivity by introducing variable permutation training. We further propose variable-aware scan along time to dynamically discover variable relationships during training and decode the optimal variable scan order by solving the shortest path visiting all nodes problem during inference. Extensive experiments conducted on eight public datasets demonstrate that MambaTS achieves new state-of-the-art performance.

5/28/2024

🔎

Integrating Mamba and Transformer for Long-Short Range Time Series Forecasting

Xiongxiao Xu, Yueqing Liang, Baixiang Huang, Zhiling Lan, Kai Shu

0

0

Time series forecasting is an important problem and plays a key role in a variety of applications including weather forecasting, stock market, and scientific simulations. Although transformers have proven to be effective in capturing dependency, its quadratic complexity of attention mechanism prevents its further adoption in long-range time series forecasting, thus limiting them attend to short-range range. Recent progress on state space models (SSMs) have shown impressive performance on modeling long range dependency due to their subquadratic complexity. Mamba, as a representative SSM, enjoys linear time complexity and has achieved strong scalability on tasks that requires scaling to long sequences, such as language, audio, and genomics. In this paper, we propose to leverage a hybrid framework Mambaformer that internally combines Mamba for long-range dependency, and Transformer for short range dependency, for long-short range forecasting. To the best of our knowledge, this is the first paper to combine Mamba and Transformer architecture in time series data. We investigate possible hybrid architectures to combine Mamba layer and attention layer for long-short range time series forecasting. The comparative study shows that the Mambaformer family can outperform Mamba and Transformer in long-short range time series forecasting problem. The code is available at https://github.com/XiongxiaoXu/Mambaformerin-Time-Series.

4/24/2024

An Empirical Study of Mamba-based Language Models

Roger Waleffe, Wonmin Byeon, Duncan Riach, Brandon Norick, Vijay Korthikanti, Tri Dao, Albert Gu, Ali Hatamizadeh, Sudhakar Singh, Deepak Narayanan, Garvit Kulshreshtha, Vartika Singh, Jared Casper, Jan Kautz, Mohammad Shoeybi, Bryan Catanzaro

0

0

Selective state-space models (SSMs) like Mamba overcome some of the shortcomings of Transformers, such as quadratic computational complexity with sequence length and large inference-time memory requirements from the key-value cache. Moreover, recent studies have shown that SSMs can match or exceed the language modeling capabilities of Transformers, making them an attractive alternative. In a controlled setting (e.g., same data), however, studies so far have only presented small scale experiments comparing SSMs to Transformers. To understand the strengths and weaknesses of these architectures at larger scales, we present a direct comparison between 8B-parameter Mamba, Mamba-2, and Transformer models trained on the same datasets of up to 3.5T tokens. We also compare these models to a hybrid architecture consisting of 43% Mamba-2, 7% attention, and 50% MLP layers (Mamba-2-Hybrid). Using a diverse set of tasks, we answer the question of whether Mamba models can match Transformers at larger training budgets. Our results show that while pure SSMs match or exceed Transformers on many tasks, they lag behind Transformers on tasks which require strong copying or in-context learning abilities (e.g., 5-shot MMLU, Phonebook) or long-context reasoning. In contrast, we find that the 8B Mamba-2-Hybrid exceeds the 8B Transformer on all 12 standard tasks we evaluated (+2.65 points on average) and is predicted to be up to 8x faster when generating tokens at inference time. To validate long-context capabilities, we provide additional experiments evaluating variants of the Mamba-2-Hybrid and Transformer extended to support 16K, 32K, and 128K sequences. On an additional 23 long-context tasks, the hybrid model continues to closely match or exceed the Transformer on average. To enable further study, we release the checkpoints as well as the code used to train our models as part of NVIDIA's Megatron-LM project.

6/13/2024