Learning Multi-Frequency Partial Correlation Graphs

0

Sign in to get full access

Overview

- Proposes a method for learning multi-frequency partial correlation graphs

- Introduces a nonconvex optimization approach to estimate a block-sparse inverse covariance matrix

- Demonstrates the technique on both synthetic and real-world data, including applications in brain connectivity analysis

Plain English Explanation

The paper presents a new way to analyze the relationships between different variables or features, particularly in situations where those relationships may operate at multiple frequencies or time scales. The key idea is to model the inverse covariance matrix - which encodes the partial correlations between variables - as a block-sparse matrix, where certain groups of variables are connected at some frequencies but not others.

This block-sparse structure allows the method to uncover patterns of conditional linear independence, where two variables may be uncorrelated after accounting for the influence of other variables, but only within specific frequency bands. <a href="https://aimodels.fyi/papers/arxiv/learning-sparse-high-dimensional-matrix-valued-graphical">By learning these multi-frequency partial correlation graphs</a>, the researchers argue that we can gain a richer understanding of the underlying system dynamics.

The method uses a nonconvex optimization approach to estimate this block-sparse inverse covariance matrix from data. The authors show that this technique performs well on both synthetic benchmarks and real-world applications, such as analyzing brain connectivity based on neuroimaging data.

Technical Explanation

The paper proposes a novel approach for learning a multi-frequency partial correlation graph from data. The key idea is to model the inverse covariance matrix, which encodes the conditional linear relationships between variables, as a block-sparse matrix.

This block-sparsity structure allows the model to capture the notion of conditional linear independence over frequency bands. That is, two variables may be uncorrelated after accounting for the influence of other variables, but only within specific frequency ranges. <a href="https://aimodels.fyi/papers/arxiv/new-reliable-parsimonious-learning-strategy-comprising-two">The authors argue that this can provide a richer characterization of the underlying system dynamics compared to standard partial correlation graphs</a>.

To estimate the block-sparse inverse covariance matrix, the paper introduces a nonconvex optimization approach. This involves solving a regularized maximum likelihood problem with a novel block-sparse penalty term. The authors show that this formulation leads to consistent estimation guarantees under appropriate technical conditions.

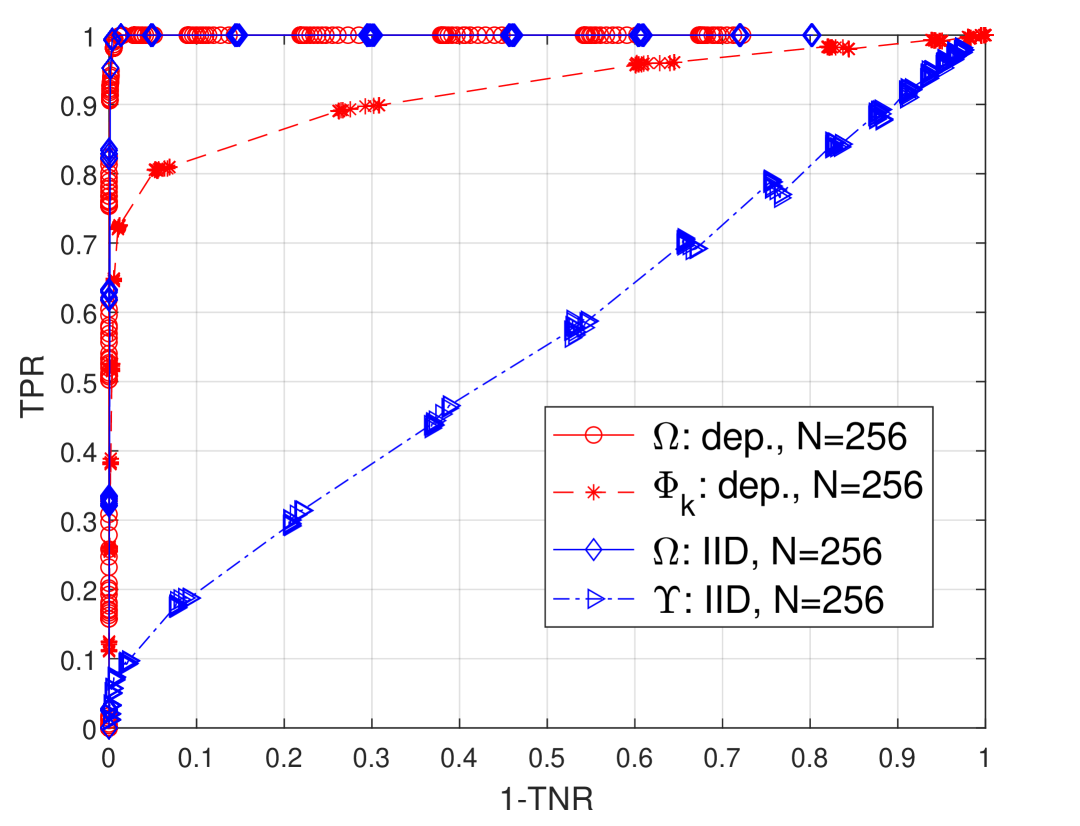

The effectiveness of the proposed method is demonstrated on both synthetic benchmarks and real-world applications, such as analyzing brain connectivity from neuroimaging data. The results indicate that the multi-frequency partial correlation graphs can uncover meaningful patterns that would be missed by traditional approaches.

Critical Analysis

One potential limitation of the proposed method is the reliance on a nonconvex optimization problem, which can be challenging to solve in practice and may be sensitive to initialization. <a href="https://aimodels.fyi/papers/arxiv/multilayer-correlation-clustering">While the authors provide theoretical guarantees, the convergence and scalability properties of the algorithm could be an area for further investigation</a>.

Additionally, the interpretation of the learned block-sparse structure may not always be straightforward, especially in high-dimensional settings. <a href="https://aimodels.fyi/papers/arxiv/k-band-self-supervised-mri-reconstruction-via">Careful validation and domain-specific knowledge may be required to ensure the meaningful interpretation of the multi-frequency partial correlation patterns</a>.

Finally, the paper focuses on the estimation of the inverse covariance matrix and its block-sparse structure, but does not delve into the potential downstream applications or decision-making processes that could leverage this information. <a href="https://aimodels.fyi/papers/arxiv/causal-representation-learning-from-multiple-distributions-general">Exploring how the learned multi-frequency partial correlation graphs can be used to inform scientific understanding, guide interventions, or improve predictive modeling could be a fruitful direction for future research</a>.

Conclusion

The proposed method for learning multi-frequency partial correlation graphs represents an interesting and potentially impactful contribution to the field of high-dimensional statistical modeling and network analysis. By capturing the nuanced patterns of conditional linear independence across frequency bands, the technique can provide a richer characterization of complex systems, with promising applications in domains such as neuroscience, finance, and beyond.

While the nonconvex optimization approach and interpretation challenges present some areas for further investigation, the paper demonstrates the potential value of this line of research and encourages the community to continue exploring how to best leverage the rich information encoded in multi-scale, heterogeneous data structures.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Learning Multi-Frequency Partial Correlation Graphs

Gabriele D'Acunto, Paolo Di Lorenzo, Francesco Bonchi, Stefania Sardellitti, Sergio Barbarossa

Despite the large research effort devoted to learning dependencies between time series, the state of the art still faces a major limitation: existing methods learn partial correlations but fail to discriminate across distinct frequency bands. Motivated by many applications in which this differentiation is pivotal, we overcome this limitation by learning a block-sparse, frequency-dependent, partial correlation graph, in which layers correspond to different frequency bands, and partial correlations can occur over just a few layers. To this aim, we formulate and solve two nonconvex learning problems: the first has a closed-form solution and is suitable when there is prior knowledge about the number of partial correlations; the second hinges on an iterative solution based on successive convex approximation, and is effective for the general case where no prior knowledge is available. Numerical results on synthetic data show that the proposed methods outperform the current state of the art. Finally, the analysis of financial time series confirms that partial correlations exist only within a few frequency bands, underscoring how our methods enable the gaining of valuable insights that would be undetected without discriminating along the frequency domain.

Read more5/14/2024

📈

0

On Sparse High-Dimensional Graphical Model Learning For Dependent Time Series

Jitendra K. Tugnait

We consider the problem of inferring the conditional independence graph (CIG) of a sparse, high-dimensional stationary multivariate Gaussian time series. A sparse-group lasso-based frequency-domain formulation of the problem based on frequency-domain sufficient statistic for the observed time series is presented. We investigate an alternating direction method of multipliers (ADMM) approach for optimization of the sparse-group lasso penalized log-likelihood. We provide sufficient conditions for convergence in the Frobenius norm of the inverse PSD estimators to the true value, jointly across all frequencies, where the number of frequencies are allowed to increase with sample size. This results also yields a rate of convergence. We also empirically investigate selection of the tuning parameters based on Bayesian information criterion, and illustrate our approach using numerical examples utilizing both synthetic and real data.

Read more6/6/2024

0

Learning Sparse High-Dimensional Matrix-Valued Graphical Models From Dependent Data

Jitendra K Tugnait

We consider the problem of inferring the conditional independence graph (CIG) of a sparse, high-dimensional, stationary matrix-variate Gaussian time series. All past work on high-dimensional matrix graphical models assumes that independent and identically distributed (i.i.d.) observations of the matrix-variate are available. Here we allow dependent observations. We consider a sparse-group lasso-based frequency-domain formulation of the problem with a Kronecker-decomposable power spectral density (PSD), and solve it via an alternating direction method of multipliers (ADMM) approach. The problem is bi-convex which is solved via flip-flop optimization. We provide sufficient conditions for local convergence in the Frobenius norm of the inverse PSD estimators to the true value. This result also yields a rate of convergence. We illustrate our approach using numerical examples utilizing both synthetic and real data.

Read more5/1/2024

0

Correlating Time Series with Interpretable Convolutional Kernels

Xinyu Chen, HanQin Cai, Fuqiang Liu, Jinhua Zhao

This study addresses the problem of convolutional kernel learning in univariate, multivariate, and multidimensional time series data, which is crucial for interpreting temporal patterns in time series and supporting downstream machine learning tasks. First, we propose formulating convolutional kernel learning for univariate time series as a sparse regression problem with a non-negative constraint, leveraging the properties of circular convolution and circulant matrices. Second, to generalize this approach to multivariate and multidimensional time series data, we use tensor computations, reformulating the convolutional kernel learning problem in the form of tensors. This is further converted into a standard sparse regression problem through vectorization and tensor unfolding operations. In the proposed methodology, the optimization problem is addressed using the existing non-negative subspace pursuit method, enabling the convolutional kernel to capture temporal correlations and patterns. To evaluate the proposed model, we apply it to several real-world time series datasets. On the multidimensional rideshare and taxi trip data from New York City and Chicago, the convolutional kernels reveal interpretable local correlations and cyclical patterns, such as weekly seasonality. In the context of multidimensional fluid flow data, both local and nonlocal correlations captured by the convolutional kernels can reinforce tensor factorization, leading to performance improvements in fluid flow reconstruction tasks. Thus, this study lays an insightful foundation for automatically learning convolutional kernels from time series data, with an emphasis on interpretability through sparsity and non-negativity constraints.

Read more9/4/2024