Correlating Time Series with Interpretable Convolutional Kernels

0

Sign in to get full access

Overview

- Time series data is common in many fields, but analyzing and interpreting these complex datasets can be challenging.

- This paper proposes a novel approach called "Correlating Time Series with Interpretable Convolutional Kernels" to address this challenge.

- The key ideas are to use interpretable convolutional kernels and sparse regression to model time series data in an efficient and transparent way.

Plain English Explanation

The researchers developed a new method to analyze time series data, which is data collected over time like stock prices, weather measurements, or medical readings. Time series data can be complex and difficult to understand, but this new approach aims to make it more interpretable.

At the core of the method are convolutional kernels - these are essentially patterns or templates that are matched against the time series data. The key innovation is that these kernels are interpretable, meaning they can be easily understood by humans. This is achieved through a sparse regression technique that selects only the most relevant kernels to model the data.

By using these interpretable convolutional kernels, the method can identify the important patterns in the time series and explain how they relate to the overall signal. This can provide valuable insights that are difficult to obtain with traditional black-box models.

The researchers demonstrate the effectiveness of their approach on several real-world time series datasets, showing that it outperforms other methods in terms of accuracy and interpretability.

Technical Explanation

The paper introduces a new time series analysis framework that leverages interpretable convolutional kernels and sparse regression. The core idea is to model the time series data as a linear combination of a small number of learned convolutional kernels.

The convolutional kernels are optimized to capture the most relevant patterns in the data, and the sparse regression technique selects only the most important kernels to include in the model. This results in a compact and interpretable representation of the time series, where the selected kernels can be directly examined to understand the driving factors behind the data.

The researchers formulate the problem as a joint optimization of the convolutional kernels and the sparse regression coefficients. They propose an efficient algorithm based on the Subspace Pursuit method to solve this optimization problem.

Experimental results on several real-world time series datasets demonstrate the effectiveness of the proposed approach. Compared to other methods, the interpretable convolutional kernels achieve superior performance in terms of both accuracy and interpretability.

Critical Analysis

The paper presents a compelling approach to time series analysis that addresses the important challenge of interpretability. By using interpretable convolutional kernels and sparse regression, the method is able to provide insights into the driving factors behind the time series data.

One potential limitation is the assumption that the time series can be well-approximated by a linear combination of a small number of convolutional kernels. While this assumption may hold for many practical applications, there could be scenarios where the data exhibits more complex nonlinear patterns that cannot be easily captured by this model.

Additionally, the paper does not provide a thorough analysis of the computational complexity of the proposed algorithm. As the dimensionality of the time series data increases, the optimization problem may become more challenging, and the scalability of the method should be further investigated.

Overall, the paper presents a promising approach that could have significant impact in a wide range of time series analysis applications, particularly where interpretability is a key requirement. Further research could explore extensions to handle more complex nonlinear patterns and investigate the scalability of the method to large-scale datasets.

Conclusion

This paper introduces a novel time series analysis framework that leverages interpretable convolutional kernels and sparse regression to provide a compact and transparent representation of the data. By identifying the most relevant patterns in the time series, the proposed approach can offer valuable insights that are difficult to obtain with traditional black-box models.

The experimental results demonstrate the effectiveness of the method, and the interpretability of the selected convolutional kernels could have significant implications for applications in fields like finance, healthcare, and environmental monitoring, where understanding the driving factors behind the data is crucial. Further research to address the potential limitations and explore extensions to handle more complex time series patterns could further enhance the usefulness of this approach.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Correlating Time Series with Interpretable Convolutional Kernels

Xinyu Chen, HanQin Cai, Fuqiang Liu, Jinhua Zhao

This study addresses the problem of convolutional kernel learning in univariate, multivariate, and multidimensional time series data, which is crucial for interpreting temporal patterns in time series and supporting downstream machine learning tasks. First, we propose formulating convolutional kernel learning for univariate time series as a sparse regression problem with a non-negative constraint, leveraging the properties of circular convolution and circulant matrices. Second, to generalize this approach to multivariate and multidimensional time series data, we use tensor computations, reformulating the convolutional kernel learning problem in the form of tensors. This is further converted into a standard sparse regression problem through vectorization and tensor unfolding operations. In the proposed methodology, the optimization problem is addressed using the existing non-negative subspace pursuit method, enabling the convolutional kernel to capture temporal correlations and patterns. To evaluate the proposed model, we apply it to several real-world time series datasets. On the multidimensional rideshare and taxi trip data from New York City and Chicago, the convolutional kernels reveal interpretable local correlations and cyclical patterns, such as weekly seasonality. In the context of multidimensional fluid flow data, both local and nonlocal correlations captured by the convolutional kernels can reinforce tensor factorization, leading to performance improvements in fluid flow reconstruction tasks. Thus, this study lays an insightful foundation for automatically learning convolutional kernels from time series data, with an emphasis on interpretability through sparsity and non-negativity constraints.

Read more9/4/2024

0

Learned Kernels for Sparse, Interpretable, and Efficient Medical Time Series Processing

Sully F. Chen, Zhicheng Guo, Cheng Ding, Xiao Hu, Cynthia Rudin

Background: Rapid, reliable, and accurate interpretation of medical signals is crucial for high-stakes clinical decision-making. The advent of deep learning allowed for an explosion of new models that offered unprecedented performance in medical time series processing but at a cost: deep learning models are often compute-intensive and lack interpretability. Methods: We propose Sparse Mixture of Learned Kernels (SMoLK), an interpretable architecture for medical time series processing. The method learns a set of lightweight flexible kernels to construct a single-layer neural network, providing not only interpretability, but also efficiency and robustness. We introduce novel parameter reduction techniques to further reduce the size of our network. We demonstrate the power of our architecture on two important tasks: photoplethysmography (PPG) artifact detection and atrial fibrillation detection from single-lead electrocardiograms (ECGs). Our approach has performance similar to the state-of-the-art deep neural networks with several orders of magnitude fewer parameters, allowing for deep neural network level performance with extremely low-power wearable devices. Results: Our interpretable method achieves greater than 99% of the performance of the state-of-the-art methods on the PPG artifact detection task, and even outperforms the state-of-the-art on a challenging out-of-distribution test set, while using dramatically fewer parameters (2% of the parameters of Segade, and about half of the parameters of Tiny-PPG). On single lead atrial fibrillation detection, our method matches the performance of a 1D-residual convolutional network, at less than 1% the parameter count, while exhibiting considerably better performance in the low-data regime, even when compared to a parameter-matched control deep network.

Read more4/3/2024

0

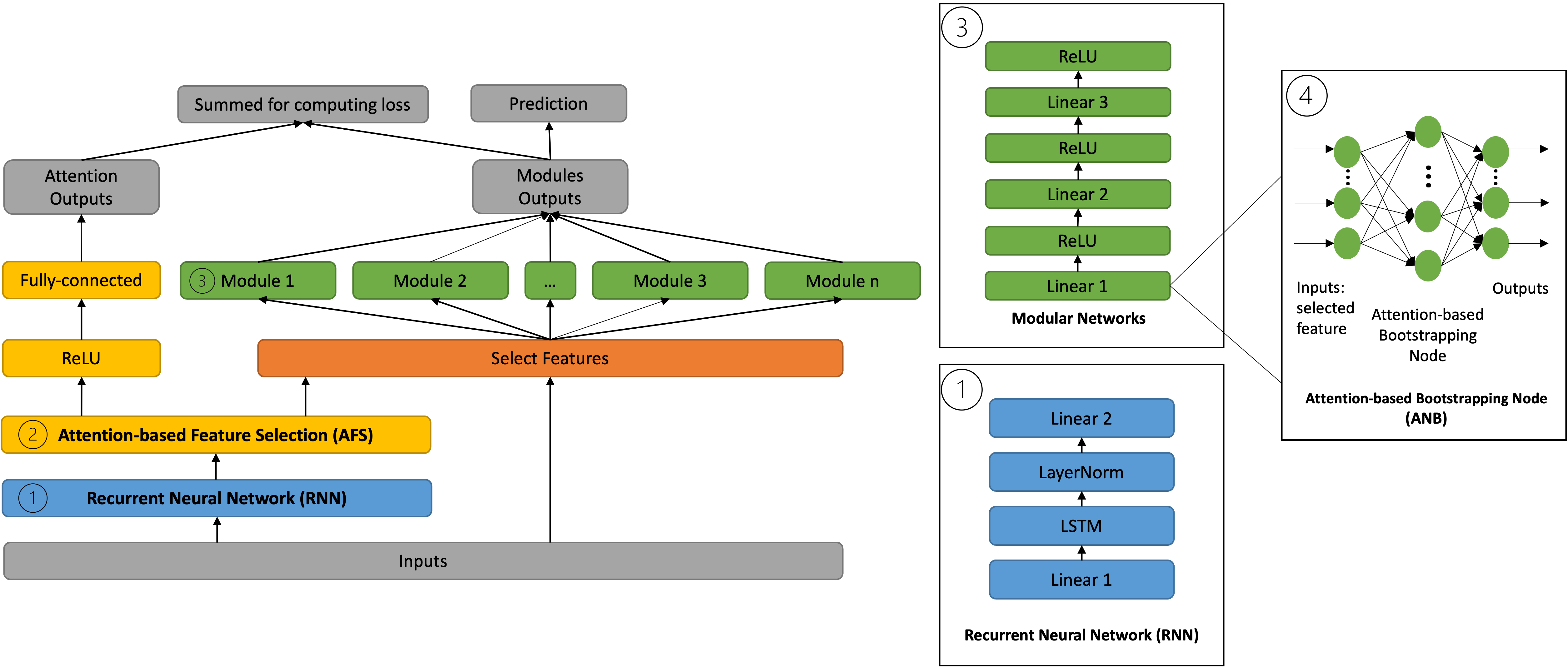

FocusLearn: Fully-Interpretable, High-Performance Modular Neural Networks for Time Series

Qiqi Su, Christos Kloukinas, Artur d'Avila Garcez

Multivariate time series have many applications, from healthcare and meteorology to life science. Although deep learning models have shown excellent predictive performance for time series, they have been criticised for being black-boxes or non-interpretable. This paper proposes a novel modular neural network model for multivariate time series prediction that is interpretable by construction. A recurrent neural network learns the temporal dependencies in the data while an attention-based feature selection component selects the most relevant features and suppresses redundant features used in the learning of the temporal dependencies. A modular deep network is trained from the selected features independently to show the users how features influence outcomes, making the model interpretable. Experimental results show that this approach can outperform state-of-the-art interpretable Neural Additive Models (NAM) and variations thereof in both regression and classification of time series tasks, achieving a predictive performance that is comparable to the top non-interpretable methods for time series, LSTM and XGBoost.

Read more5/6/2024

0

Causal Discovery from Time-Series Data with Short-Term Invariance-Based Convolutional Neural Networks

Rujia Shen, Boran Wang, Chao Zhao, Yi Guan, Jingchi Jiang

Causal discovery from time-series data aims to capture both intra-slice (contemporaneous) and inter-slice (time-lagged) causality between variables within the temporal chain, which is crucial for various scientific disciplines. Compared to causal discovery from non-time-series data, causal discovery from time-series data necessitates more serialized samples with a larger amount of observed time steps. To address the challenges, we propose a novel gradient-based causal discovery approach STIC, which focuses on textbf{S}hort-textbf{T}erm textbf{I}nvariance using textbf{C}onvolutional neural networks to uncover the causal relationships from time-series data. Specifically, STIC leverages both the short-term time and mechanism invariance of causality within each window observation, which possesses the property of independence, to enhance sample efficiency. Furthermore, we construct two causal convolution kernels, which correspond to the short-term time and mechanism invariance respectively, to estimate the window causal graph. To demonstrate the necessity of convolutional neural networks for causal discovery from time-series data, we theoretically derive the equivalence between convolution and the underlying generative principle of time-series data under the assumption that the additive noise model is identifiable. Experimental evaluations conducted on both synthetic and FMRI benchmark datasets demonstrate that our STIC outperforms baselines significantly and achieves the state-of-the-art performance, particularly when the datasets contain a limited number of observed time steps. Code is available at url{https://github.com/HITshenrj/STIC}.

Read more8/16/2024