Prediction Risk and Estimation Risk of the Ridgeless Least Squares Estimator under General Assumptions on Regression Errors

2305.12883

0

0

🔮

Abstract

In recent years, there has been a significant growth in research focusing on minimum $ell_2$ norm (ridgeless) interpolation least squares estimators. However, the majority of these analyses have been limited to an unrealistic regression error structure, assuming independent and identically distributed errors with zero mean and common variance. In this paper, we explore prediction risk as well as estimation risk under more general regression error assumptions, highlighting the benefits of overparameterization in a more realistic setting that allows for clustered or serial dependence. Notably, we establish that the estimation difficulties associated with the variance components of both risks can be summarized through the trace of the variance-covariance matrix of the regression errors. Our findings suggest that the benefits of overparameterization can extend to time series, panel and grouped data.

Create account to get full access

Overview

- This paper explores the prediction and estimation risk of minimum ℓ₂ norm (ridgeless) interpolation least squares estimators under more general regression error assumptions, such as clustered or serial dependence.

- The authors highlight the benefits of overparameterization in this more realistic setting, as opposed to the commonly studied scenario of independent and identically distributed errors with zero mean and common variance.

- The key finding is that the estimation difficulties associated with the variance components of both risks can be summarized through the trace of the variance-covariance matrix of the regression errors.

- The paper suggests that the benefits of overparameterization can extend to time series, panel, and grouped data.

Plain English Explanation

In recent years, there has been a lot of research on a type of statistical model called "minimum ℓ₂ norm (ridgeless) interpolation least squares estimators." These models are useful for making predictions and estimating unknown quantities from data.

However, most of the previous research on these models has assumed an unrealistic structure for the errors (the differences between the predictions and the actual values). Specifically, they've assumed the errors are independent and have the same average and variance.

This new paper explores what happens when the errors have a more general structure, such as being clustered together or having a pattern over time (serial dependence). The authors find that the key to understanding the performance of these models in this more realistic setting is the trace of the variance-covariance matrix of the errors.

Importantly, the paper suggests that the benefits of using these overparameterized models (models with more variables than observations) can extend to a wider range of data types, including time series, panel data (repeated observations over time), and grouped data.

Technical Explanation

The paper Precise Analysis of Ridge Interpolators Under Heavy Correlations examines the prediction and estimation risk of minimum ℓ₂ norm (ridgeless) interpolation least squares estimators under more general regression error assumptions.

Unlike prior work, which focused on the unrealistic case of independent and identically distributed errors with zero mean and common variance, this research considers scenarios with clustered or serial dependence in the errors. The authors establish that the estimation difficulties associated with the variance components of both prediction and estimation risk can be summarized through the trace of the variance-covariance matrix of the regression errors.

The paper builds on previous research on the algebraic and statistical properties of ordinary least squares interpolators and the exact analysis of ridge interpolators in correlated factor regression models. It also connects to work on regression in extreme regions and learning with little mixing.

The key insight is that the benefits of overparameterization (using more variables than observations) can extend beyond the commonly studied setting of independent and identically distributed errors to a wider range of data types, including time series, panel data, and grouped data.

Critical Analysis

The paper provides a rigorous mathematical analysis of the prediction and estimation risk of minimum ℓ₂ norm (ridgeless) interpolation least squares estimators under more general regression error assumptions. The authors are careful to highlight the limitations of their analysis, noting that it relies on certain technical conditions and does not address the issue of model selection.

One potential concern is that the paper focuses solely on the theoretical properties of these estimators, without providing any empirical validation of the findings. It would be useful to see how the theoretical results hold up in practical applications with real-world data.

Additionally, the paper does not discuss the computational complexity or scalability of these methods, which could be an important consideration in large-scale or high-dimensional settings. Further research is needed to understand the practical tradeoffs and challenges in implementing these techniques.

Overall, the paper makes a valuable contribution to the literature by extending the analysis of ridgeless interpolation methods to more realistic error structures. The findings suggest promising directions for future research and applications of these techniques in a wider range of data analysis scenarios.

Conclusion

This paper presents a detailed theoretical analysis of minimum ℓ₂ norm (ridgeless) interpolation least squares estimators under more general regression error assumptions, such as clustered or serial dependence. The key finding is that the estimation difficulties associated with the variance components of both prediction and estimation risk can be summarized through the trace of the variance-covariance matrix of the regression errors.

The authors demonstrate that the benefits of overparameterization (using more variables than observations) can extend beyond the commonly studied setting of independent and identically distributed errors to a wider range of data types, including time series, panel data, and grouped data. This suggests that these techniques may have broader applicability in real-world data analysis scenarios.

While the paper provides a rigorous theoretical foundation, further research is needed to validate the findings empirically and address practical considerations such as computational complexity and model selection. Nevertheless, this work represents an important step forward in understanding the properties and potential applications of ridgeless interpolation methods in more realistic settings.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

Precise analysis of ridge interpolators under heavy correlations -- a Random Duality Theory view

Mihailo Stojnic

0

0

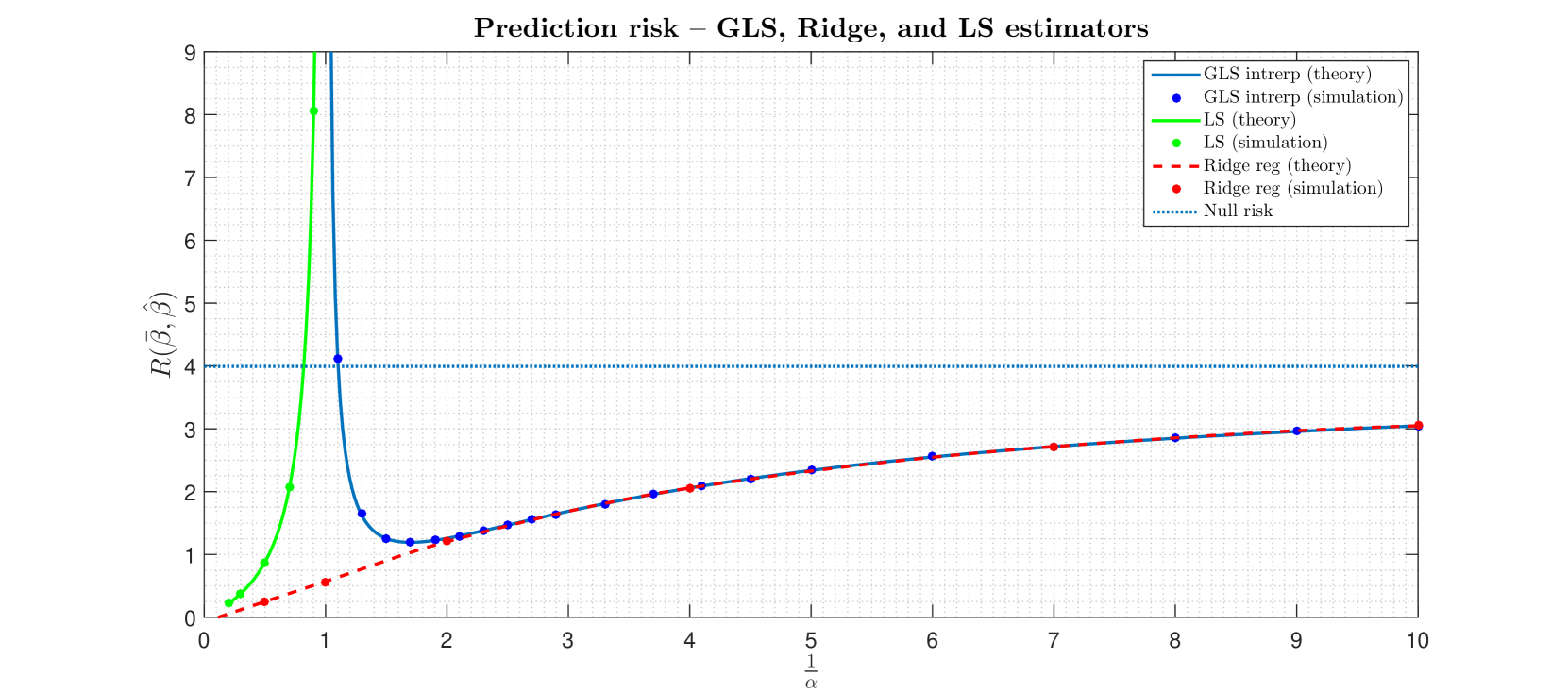

We consider fully row/column-correlated linear regression models and study several classical estimators (including minimum norm interpolators (GLS), ordinary least squares (LS), and ridge regressors). We show that emph{Random Duality Theory} (RDT) can be utilized to obtain precise closed form characterizations of all estimators related optimizing quantities of interest, including the emph{prediction risk} (testing or generalization error). On a qualitative level out results recover the risk's well known non-monotonic (so-called double-descent) behavior as the number of features/sample size ratio increases. On a quantitative level, our closed form results show how the risk explicitly depends on all key model parameters, including the problem dimensions and covariance matrices. Moreover, a special case of our results, obtained when intra-sample (or time-series) correlations are not present, precisely match the corresponding ones obtained via spectral methods in [6,16,17,24].

6/14/2024

🏅

Algebraic and Statistical Properties of the Ordinary Least Squares Interpolator

Dennis Shen, Dogyoon Song, Peng Ding, Jasjeet S. Sekhon

0

0

Deep learning research has uncovered the phenomenon of benign overfitting for overparameterized statistical models, which has drawn significant theoretical interest in recent years. Given its simplicity and practicality, the ordinary least squares (OLS) interpolator has become essential to gain foundational insights into this phenomenon. While properties of OLS are well established in classical, underparameterized settings, its behavior in high-dimensional, overparameterized regimes is less explored (unlike for ridge or lasso regression) though significant progress has been made of late. We contribute to this growing literature by providing fundamental algebraic and statistical results for the minimum $ell_2$-norm OLS interpolator. In particular, we provide algebraic equivalents of (i) the leave-$k$-out residual formula, (ii) Cochran's formula, and (iii) the Frisch-Waugh-Lovell theorem in the overparameterized regime. These results aid in understanding the OLS interpolator's ability to generalize and have substantive implications for causal inference. Under the Gauss-Markov model, we present statistical results such as an extension of the Gauss-Markov theorem and an analysis of variance estimation under homoskedastic errors for the overparameterized regime. To substantiate our theoretical contributions, we conduct simulations that further explore the stochastic properties of the OLS interpolator.

5/31/2024

Ridge interpolators in correlated factor regression models -- exact risk analysis

Mihailo Stojnic

0

0

We consider correlated emph{factor} regression models (FRM) and analyze the performance of classical ridge interpolators. Utilizing powerful emph{Random Duality Theory} (RDT) mathematical engine, we obtain emph{precise} closed form characterizations of the underlying optimization problems and all associated optimizing quantities. In particular, we provide emph{excess prediction risk} characterizations that clearly show the dependence on all key model parameters, covariance matrices, loadings, and dimensions. As a function of the over-parametrization ratio, the generalized least squares (GLS) risk also exhibits the well known emph{double-descent} (non-monotonic) behavior. Similarly to the classical linear regression models (LRM), we demonstrate that such FRM phenomenon can be smoothened out by the optimally tuned ridge regularization. The theoretical results are supplemented by numerical simulations and an excellent agrement between the two is observed. Moreover, we note that ``ridge smootenhing'' is often of limited effect already for over-parametrization ratios above $5$ and of virtually no effect for those above $10$. This solidifies the notion that one of the recently most popular neural networks paradigms -- emph{zero-training (interpolating) generalizes well} -- enjoys wider applicability, including the one within the FRM estimation/prediction context.

6/14/2024

↗️

On Regression in Extreme Regions

Nathan Huet, Stephan Cl'emenc{c}on, Anne Sabourin

0

0

The statistical learning problem consists in building a predictive function $hat{f}$ based on independent copies of $(X,Y)$ so that $Y$ is approximated by $hat{f}(X)$ with minimum (squared) error. Motivated by various applications, special attention is paid here to the case of extreme (i.e. very large) observations $X$. Because of their rarity, the contributions of such observations to the (empirical) error is negligible, and the predictive performance of empirical risk minimizers can be consequently very poor in extreme regions. In this paper, we develop a general framework for regression on extremes. Under appropriate regular variation assumptions regarding the pair $(X,Y)$, we show that an asymptotic notion of risk can be tailored to summarize appropriately predictive performance in extreme regions. It is also proved that minimization of an empirical and nonasymptotic version of this 'extreme risk', based on a fraction of the largest observations solely, yields good generalization capacity. In addition, numerical results providing strong empirical evidence of the relevance of the approach proposed are displayed.

4/11/2024