Precise analysis of ridge interpolators under heavy correlations -- a Random Duality Theory view

0

Sign in to get full access

Overview

- This research paper presents a precise analysis of ridge interpolators, which are a type of machine learning model, in the context of heavily correlated factor regression models.

- The authors use a "Random Duality Theory" approach to provide a rigorous mathematical analysis of the properties and performance of ridge interpolators in this challenging setting.

- The findings have implications for understanding the behavior of ridge regression and related methods in high-dimensional, correlated data scenarios.

Plain English Explanation

The paper examines a machine learning technique called "ridge interpolation" and how it performs when the input features (or "factors") are highly correlated with each other. This is a common challenge in real-world datasets, where variables tend to be interconnected.

The researchers use a mathematical framework called "Random Duality Theory" to analyze ridge interpolation models in depth. This allows them to precisely characterize the behavior of these models and understand their strengths and limitations when working with heavily correlated data.

The key insights from this work can help researchers and practitioners make better use of ridge regression and related methods, which are widely used for tasks like predicting outcomes and dimensionality reduction. By accounting for the effects of high correlations, the findings could lead to improved model performance and more reliable statistical inferences in a variety of applications.

Technical Explanation

The paper formalizes the problem of ridge interpolation in the context of high-dimensional, factor regression models where the input features exhibit strong correlations. Using the Random Duality Theory framework, the authors derive precise, deterministic equivalents that characterize the behavior of the ridge interpolator.

Specifically, they analyze the statistical properties of the ridge interpolator, including its prediction risk and effective degrees of freedom. The analysis reveals how these key quantities depend on the correlation structure of the input features and the regularization parameter of the ridge interpolator.

The theoretical results provide a rigorous understanding of the algebraic and statistical properties of ridge interpolation in the presence of heavy correlations. This, in turn, can inform the design and application of ridge-based methods for high-dimensional regression problems.

Critical Analysis

The paper provides a comprehensive and technically sound analysis of ridge interpolators under heavy correlations. The authors' use of the Random Duality Theory framework allows them to derive exact, deterministic expressions for the key properties of the ridge interpolator, which is a significant theoretical contribution.

One potential limitation of the study is that it focuses solely on the ridge interpolator and does not consider other regularization methods, such as the lasso or elastic net. Extending the analysis to these alternative regularization techniques could provide a more complete understanding of how different approaches perform in highly correlated settings.

Additionally, while the paper offers insights into the statistical properties of the ridge interpolator, it does not directly address practical considerations, such as the choice of the regularization parameter or the sensitivity of the results to model assumptions. Exploring these aspects could further enhance the applicability of the theoretical findings.

Conclusion

This research paper presents a rigorous mathematical analysis of ridge interpolators in the context of high-dimensional, factor regression models with heavy correlations. The authors' use of the Random Duality Theory framework allows them to derive precise, deterministic equivalents for key statistical properties of the ridge interpolator, such as its prediction risk and effective degrees of freedom.

The findings from this work contribute to a deeper understanding of the behavior of ridge-based methods in challenging, real-world settings where input features are highly correlated. This knowledge can inform the design and application of ridge regression and related techniques, ultimately leading to improved model performance and more reliable statistical inferences across a variety of domains.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Precise analysis of ridge interpolators under heavy correlations -- a Random Duality Theory view

Mihailo Stojnic

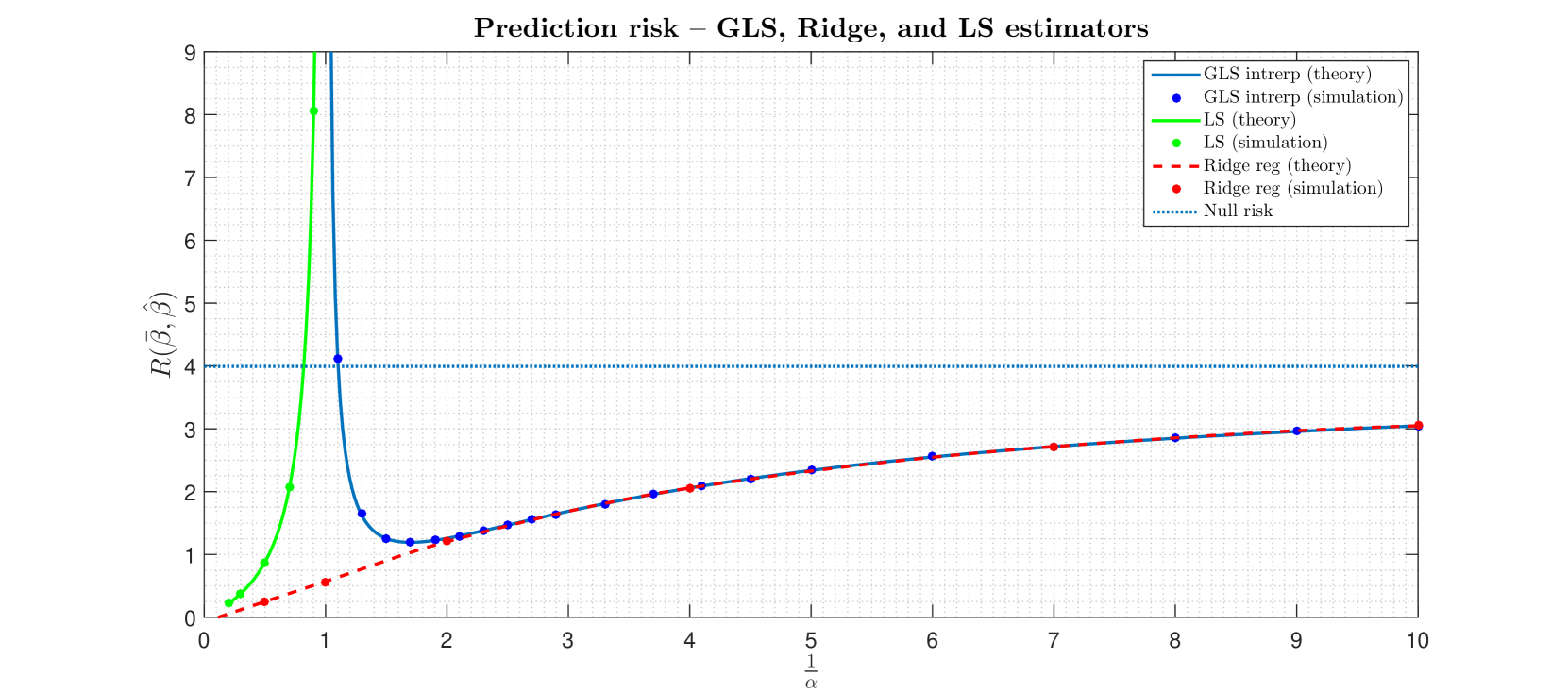

We consider fully row/column-correlated linear regression models and study several classical estimators (including minimum norm interpolators (GLS), ordinary least squares (LS), and ridge regressors). We show that emph{Random Duality Theory} (RDT) can be utilized to obtain precise closed form characterizations of all estimators related optimizing quantities of interest, including the emph{prediction risk} (testing or generalization error). On a qualitative level out results recover the risk's well known non-monotonic (so-called double-descent) behavior as the number of features/sample size ratio increases. On a quantitative level, our closed form results show how the risk explicitly depends on all key model parameters, including the problem dimensions and covariance matrices. Moreover, a special case of our results, obtained when intra-sample (or time-series) correlations are not present, precisely match the corresponding ones obtained via spectral methods in [6,16,17,24].

Read more6/14/2024

0

Ridge interpolators in correlated factor regression models -- exact risk analysis

Mihailo Stojnic

We consider correlated emph{factor} regression models (FRM) and analyze the performance of classical ridge interpolators. Utilizing powerful emph{Random Duality Theory} (RDT) mathematical engine, we obtain emph{precise} closed form characterizations of the underlying optimization problems and all associated optimizing quantities. In particular, we provide emph{excess prediction risk} characterizations that clearly show the dependence on all key model parameters, covariance matrices, loadings, and dimensions. As a function of the over-parametrization ratio, the generalized least squares (GLS) risk also exhibits the well known emph{double-descent} (non-monotonic) behavior. Similarly to the classical linear regression models (LRM), we demonstrate that such FRM phenomenon can be smoothened out by the optimally tuned ridge regularization. The theoretical results are supplemented by numerical simulations and an excellent agrement between the two is observed. Moreover, we note that ``ridge smootenhing'' is often of limited effect already for over-parametrization ratios above $5$ and of virtually no effect for those above $10$. This solidifies the notion that one of the recently most popular neural networks paradigms -- emph{zero-training (interpolating) generalizes well} -- enjoys wider applicability, including the one within the FRM estimation/prediction context.

Read more6/14/2024

🔮

0

Prediction Risk and Estimation Risk of the Ridgeless Least Squares Estimator under General Assumptions on Regression Errors

Sungyoon Lee, Sokbae Lee

In recent years, there has been a significant growth in research focusing on minimum $ell_2$ norm (ridgeless) interpolation least squares estimators. However, the majority of these analyses have been limited to an unrealistic regression error structure, assuming independent and identically distributed errors with zero mean and common variance. In this paper, we explore prediction risk as well as estimation risk under more general regression error assumptions, highlighting the benefits of overparameterization in a more realistic setting that allows for clustered or serial dependence. Notably, we establish that the estimation difficulties associated with the variance components of both risks can be summarized through the trace of the variance-covariance matrix of the regression errors. Our findings suggest that the benefits of overparameterization can extend to time series, panel and grouped data.

Read more6/14/2024

0

Risk and cross validation in ridge regression with correlated samples

Alexander Atanasov, Jacob A. Zavatone-Veth, Cengiz Pehlevan

Recent years have seen substantial advances in our understanding of high-dimensional ridge regression, but existing theories assume that training examples are independent. By leveraging recent techniques from random matrix theory and free probability, we provide sharp asymptotics for the in- and out-of-sample risks of ridge regression when the data points have arbitrary correlations. We demonstrate that in this setting, the generalized cross validation estimator (GCV) fails to correctly predict the out-of-sample risk. However, in the case where the noise residuals have the same correlations as the data points, one can modify the GCV to yield an efficiently-computable unbiased estimator that concentrates in the high-dimensional limit, which we dub CorrGCV. We further extend our asymptotic analysis to the case where the test point has nontrivial correlations with the training set, a setting often encountered in time series forecasting. Assuming knowledge of the correlation structure of the time series, this again yields an extension of the GCV estimator, and sharply characterizes the degree to which such test points yield an overly optimistic prediction of long-time risk. We validate the predictions of our theory across a variety of high dimensional data.

Read more8/13/2024