ReModels: Quantile Regression Averaging models

2405.11372

0

0

Abstract

Electricity price forecasts play a crucial role in making key business decisions within the electricity markets. A focal point in this domain are probabilistic predictions, which delineate future price values in a more comprehensive manner than simple point forecasts. The golden standard in probabilistic approaches to predict energy prices is the Quantile Regression Averaging (QRA) method. In this paper, we present a Python package that encompasses the implementation of QRA, along with modifications of this approach that have appeared in the literature over the past few years. The proposed package also facilitates the acquisition and preparation of data related to electricity markets, as well as the evaluation of model predictions.

Create account to get full access

Overview

- The paper introduces "ReModels", a framework for quantile regression averaging models

- Quantile regression averaging models are used for probabilistic forecasting, particularly in applications like short-term electricity price forecasting

- The ReModels framework provides a way to combine multiple quantile regression models to improve forecasting accuracy and reliability

Plain English Explanation

The paper introduces a new approach called "ReModels" for making probabilistic forecasts. Probabilistic forecasting is important in domains like electricity price forecasting, where it's useful to know not just the most likely future price, but the full range of possible prices and their likelihoods.

ReModels works by combining the results of multiple quantile regression models - models that can predict not just the average or median value, but the full probability distribution of possible outcomes. By averaging the results of these individual models, ReModels can produce more accurate and reliable probabilistic forecasts.

The key idea is that each individual quantile regression model may have its own strengths and weaknesses, and by combining them, the weaknesses of one model can be offset by the strengths of others. This type of model averaging approach has been shown to improve forecasting performance in a variety of applications, including electricity price forecasting and renewable energy forecasting.

Technical Explanation

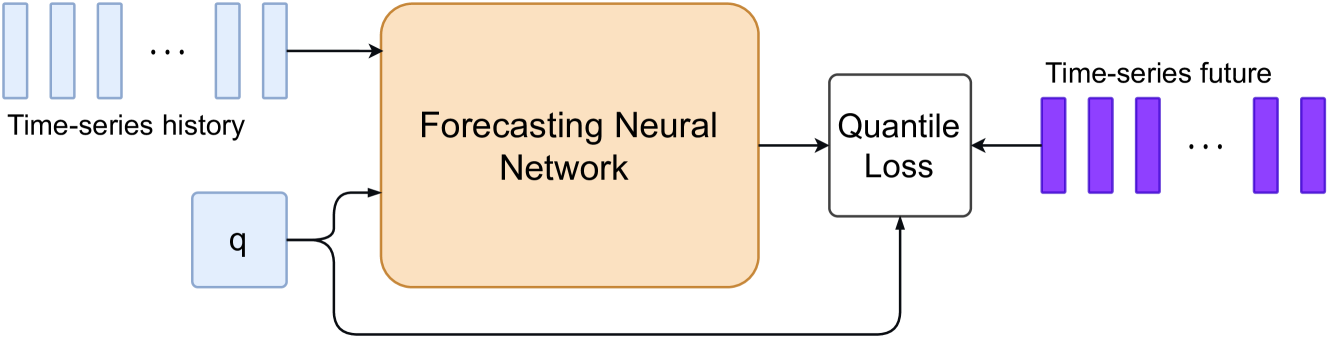

The ReModels framework is built on the idea of quantile regression, which is a statistical technique for estimating the conditional quantiles of a dependent variable given a set of independent variables. Unlike standard regression, which only estimates the conditional mean, quantile regression can estimate the full probability distribution of the dependent variable.

The key steps in the ReModels framework are:

- Fit multiple individual quantile regression models, each targeting a different quantile of the dependent variable.

- Combine the predictions of these individual models using a weighted average, where the weights are determined by the performance of each model on a validation dataset.

- Use the combined quantile regression model to make probabilistic forecasts, providing not just a point estimate but the full distribution of possible outcomes.

This approach has been shown to outperform individual quantile regression models, as well as other probabilistic forecasting methods like adaptive standardization and robust averaging, particularly in applications with high volatility and uncertainty, such as short-term electricity price forecasting and renewable energy forecasting.

Critical Analysis

The paper provides a thorough evaluation of the ReModels framework, including experiments on both simulated and real-world datasets. The results demonstrate the effectiveness of the approach, particularly in challenging forecasting scenarios.

However, the paper does not address some potential limitations or areas for further research. For example, the choice of individual quantile regression models and the weighting scheme used to combine them may have a significant impact on the overall performance, and the authors do not provide guidance on how to optimize these choices.

Additionally, the paper focuses on point-in-time forecasting, but in many real-world applications, there is a need for conformal prediction - the ability to provide reliable prediction intervals that guarantee a certain level of coverage. It would be interesting to see how the ReModels framework could be extended to provide this type of prediction guarantee.

Overall, the ReModels framework represents a promising approach to probabilistic forecasting, and the paper provides a solid foundation for further research and development in this area.

Conclusion

The ReModels framework introduced in this paper offers a novel and effective approach to quantile regression averaging for probabilistic forecasting. By combining the strengths of multiple individual quantile regression models, ReModels can produce more accurate and reliable forecasts, particularly in applications with high uncertainty and volatility, such as short-term electricity price forecasting and renewable energy forecasting.

The technical details and empirical evaluation provided in the paper demonstrate the potential of this approach, and suggest that it could have significant practical applications in a variety of domains. While the paper identifies some areas for further research, the core ideas of ReModels represent an important contribution to the field of probabilistic forecasting.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

Any-Quantile Probabilistic Forecasting of Short-Term Electricity Demand

Slawek Smyl, Boris N. Oreshkin, Pawe{l} Pe{l}ka, Grzegorz Dudek

0

0

Power systems operate under uncertainty originating from multiple factors that are impossible to account for deterministically. Distributional forecasting is used to control and mitigate risks associated with this uncertainty. Recent progress in deep learning has helped to significantly improve the accuracy of point forecasts, while accurate distributional forecasting still presents a significant challenge. In this paper, we propose a novel general approach for distributional forecasting capable of predicting arbitrary quantiles. We show that our general approach can be seamlessly applied to two distinct neural architectures leading to the state-of-the-art distributional forecasting results in the context of short-term electricity demand forecasting task. We empirically validate our method on 35 hourly electricity demand time-series for European countries. Our code is available here: https://github.com/boreshkinai/any-quantile.

4/29/2024

Stacking for Probabilistic Short-term Load Forecasting

Grzegorz Dudek

0

0

In this study, we delve into the realm of meta-learning to combine point base forecasts for probabilistic short-term electricity demand forecasting. Our approach encompasses the utilization of quantile linear regression, quantile regression forest, and post-processing techniques involving residual simulation to generate quantile forecasts. Furthermore, we introduce both global and local variants of meta-learning. In the local-learning mode, the meta-model is trained using patterns most similar to the query pattern.Through extensive experimental studies across 35 forecasting scenarios and employing 16 base forecasting models, our findings underscored the superiority of quantile regression forest over its competitors

6/18/2024

Optimizing Quantile-based Trading Strategies in Electricity Arbitrage

Ciaran O'Connor, Joseph Collins, Steven Prestwich, Andrea Visentin

0

0

Efficiently integrating renewable resources into electricity markets is vital for addressing the challenges of matching real-time supply and demand while reducing the significant energy wastage resulting from curtailments. To address this challenge effectively, the incorporation of storage devices can enhance the reliability and efficiency of the grid, improving market liquidity and reducing price volatility. In short-term electricity markets, participants navigate numerous options, each presenting unique challenges and opportunities, underscoring the critical role of the trading strategy in maximizing profits. This study delves into the optimization of day-ahead and balancing market trading, leveraging quantile-based forecasts. Employing three trading approaches with practical constraints, our research enhances forecast assessment, increases trading frequency, and employs flexible timestamp orders. Our findings underscore the profit potential of simultaneous participation in both day-ahead and balancing markets, especially with larger battery storage systems; despite increased costs and narrower profit margins associated with higher-volume trading, the implementation of high-frequency strategies plays a significant role in maximizing profits and addressing market challenges. Finally, we modelled four commercial battery storage systems and evaluated their economic viability through a scenario analysis, with larger batteries showing a shorter return on investment.

6/21/2024

Forecasting Electricity Market Signals via Generative AI

Xinyi Wang, Qing Zhao, Lang Tong

0

0

This paper presents a generative artificial intelligence approach to probabilistic forecasting of electricity market signals, such as real-time locational marginal prices and area control error signals. Inspired by the Wiener-Kallianpur innovation representation of nonparametric time series, we propose a weak innovation autoencoder architecture and a novel deep learning algorithm that extracts the canonical independent and identically distributed innovation sequence of the time series, from which future time series samples are generated. The validity of the proposed approach is established by proving that, under ideal training conditions, the generated samples have the same conditional probability distribution as that of the ground truth. Three applications involving highly dynamic and volatile time series in real-time market operations are considered: (i) locational marginal price forecasting for self-scheduled resources such as battery storage participants, (ii) interregional price spread forecasting for virtual bidders in interchange markets, and (iii) area control error forecasting for frequency regulations. Numerical studies based on market data from multiple independent system operators demonstrate the superior performance of the proposed generative forecaster over leading classical and modern machine learning techniques under both probabilistic and point forecasting metrics.

4/26/2024