Revitalizing Multivariate Time Series Forecasting: Learnable Decomposition with Inter-Series Dependencies and Intra-Series Variations Modeling

0

Sign in to get full access

Overview

- The paper proposes a novel "learnable decomposition" approach to improve multivariate time series forecasting.

- The method models inter-series dependencies and intra-series variations to capture complex patterns in the data.

- Experiments show the proposed model outperforms various state-of-the-art time series forecasting techniques.

Plain English Explanation

The paper tackles the challenge of forecasting multivariate time series data, which means predicting future values for multiple related variables over time. Traditional forecasting methods often struggle to capture the complex relationships and patterns in this type of data.

The researchers introduce a new "learnable decomposition" strategy that aims to address this problem. Their approach breaks down the time series data into different components, allowing the model to separately learn and model the dependencies between the various data streams (inter-series dependencies) as well as the unique patterns within each individual data stream (intra-series variations).

By decomposing the data in this way and using neural networks to learn the underlying structures, the model is able to make more accurate forecasts compared to other state-of-the-art time series prediction techniques. The method can be applied to a wide range of multivariate time series datasets, from things like sales figures and stock prices to sensor measurements and energy consumption data.

Technical Explanation

The key innovation in this paper is the "learnable decomposition" strategy for multivariate time series forecasting. Traditional approaches [https://aimodels.fyi/papers/arxiv/unitst-effectively-modeling-inter-series-intra-series] often struggle to capture the complex relationships between the different data streams, as well as the unique patterns within each individual stream.

To address this, the proposed model [https://aimodels.fyi/papers/arxiv/focuslearn-fully-interpretable-high-performance-modular-neural] decomposes the multivariate time series into several components, including:

- Inter-series dependencies: Modeling the relationships and interactions between the different data streams.

- Intra-series variations: Capturing the unique patterns and dynamics within each individual data stream.

The decomposition is "learnable" in the sense that the model learns the optimal way to break down the data, rather than using a predefined or static decomposition. This allows the model to flexibly adapt to the specific characteristics of the input data.

The overall architecture [https://aimodels.fyi/papers/arxiv/parsimony-or-capability-decomposition-delivers-both-long] combines various neural network modules to handle the different aspects of the decomposition and forecasting process. Experiments [https://aimodels.fyi/papers/arxiv/combination-model-based-sequential-general-variational-mode] on several benchmark datasets demonstrate the superior performance of this approach compared to other state-of-the-art time series forecasting methods.

Critical Analysis

The paper presents a well-designed and effective solution for multivariate time series forecasting, but it is important to consider some potential limitations and areas for further research:

The authors acknowledge that the proposed model may not be as interpretable as some other time series forecasting techniques [https://aimodels.fyi/papers/arxiv/adaptive-multi-scale-decomposition-framework-time-series]. While the decomposition strategy provides useful insights, the inner workings of the neural network modules may still be difficult to fully understand.

Additionally, the paper only evaluates the model on a limited set of benchmark datasets. More research is needed to assess its performance on a wider range of real-world multivariate time series problems, which may have unique characteristics and challenges.

Finally, the computational complexity of the model could be a concern, especially for large-scale or high-frequency time series data. The authors do not provide a detailed analysis of the model's scalability and runtime efficiency.

Overall, the paper presents a promising approach to multivariate time series forecasting, but further research and validation would be beneficial to fully understand the strengths, limitations, and practical implications of the proposed method.

Conclusion

The paper introduces a novel "learnable decomposition" strategy for multivariate time series forecasting, which outperforms various state-of-the-art techniques. By separately modeling the inter-series dependencies and intra-series variations, the model is able to capture the complex patterns and relationships in the data more effectively.

This research represents an important step forward in addressing the challenges of multivariate time series prediction, which has numerous real-world applications, from business forecasting to sensor data analysis. The insights and techniques presented in this paper could inspire further advancements in the field and lead to more accurate and reliable forecasting models for a wide range of practical use cases.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Revitalizing Multivariate Time Series Forecasting: Learnable Decomposition with Inter-Series Dependencies and Intra-Series Variations Modeling

Guoqi Yu, Jing Zou, Xiaowei Hu, Angelica I. Aviles-Rivero, Jing Qin, Shujun Wang

Predicting multivariate time series is crucial, demanding precise modeling of intricate patterns, including inter-series dependencies and intra-series variations. Distinctive trend characteristics in each time series pose challenges, and existing methods, relying on basic moving average kernels, may struggle with the non-linear structure and complex trends in real-world data. Given that, we introduce a learnable decomposition strategy to capture dynamic trend information more reasonably. Additionally, we propose a dual attention module tailored to capture inter-series dependencies and intra-series variations simultaneously for better time series forecasting, which is implemented by channel-wise self-attention and autoregressive self-attention. To evaluate the effectiveness of our method, we conducted experiments across eight open-source datasets and compared it with the state-of-the-art methods. Through the comparison results, our Leddam (LEarnable Decomposition and Dual Attention Module) not only demonstrates significant advancements in predictive performance, but also the proposed decomposition strategy can be plugged into other methods with a large performance-boosting, from 11.87% to 48.56% MSE error degradation.

Read more7/8/2024

0

UniTST: Effectively Modeling Inter-Series and Intra-Series Dependencies for Multivariate Time Series Forecasting

Juncheng Liu, Chenghao Liu, Gerald Woo, Yiwei Wang, Bryan Hooi, Caiming Xiong, Doyen Sahoo

Transformer-based models have emerged as powerful tools for multivariate time series forecasting (MTSF). However, existing Transformer models often fall short of capturing both intricate dependencies across variate and temporal dimensions in MTS data. Some recent models are proposed to separately capture variate and temporal dependencies through either two sequential or parallel attention mechanisms. However, these methods cannot directly and explicitly learn the intricate inter-series and intra-series dependencies. In this work, we first demonstrate that these dependencies are very important as they usually exist in real-world data. To directly model these dependencies, we propose a transformer-based model UniTST containing a unified attention mechanism on the flattened patch tokens. Additionally, we add a dispatcher module which reduces the complexity and makes the model feasible for a potentially large number of variates. Although our proposed model employs a simple architecture, it offers compelling performance as shown in our extensive experiments on several datasets for time series forecasting.

Read more6/10/2024

0

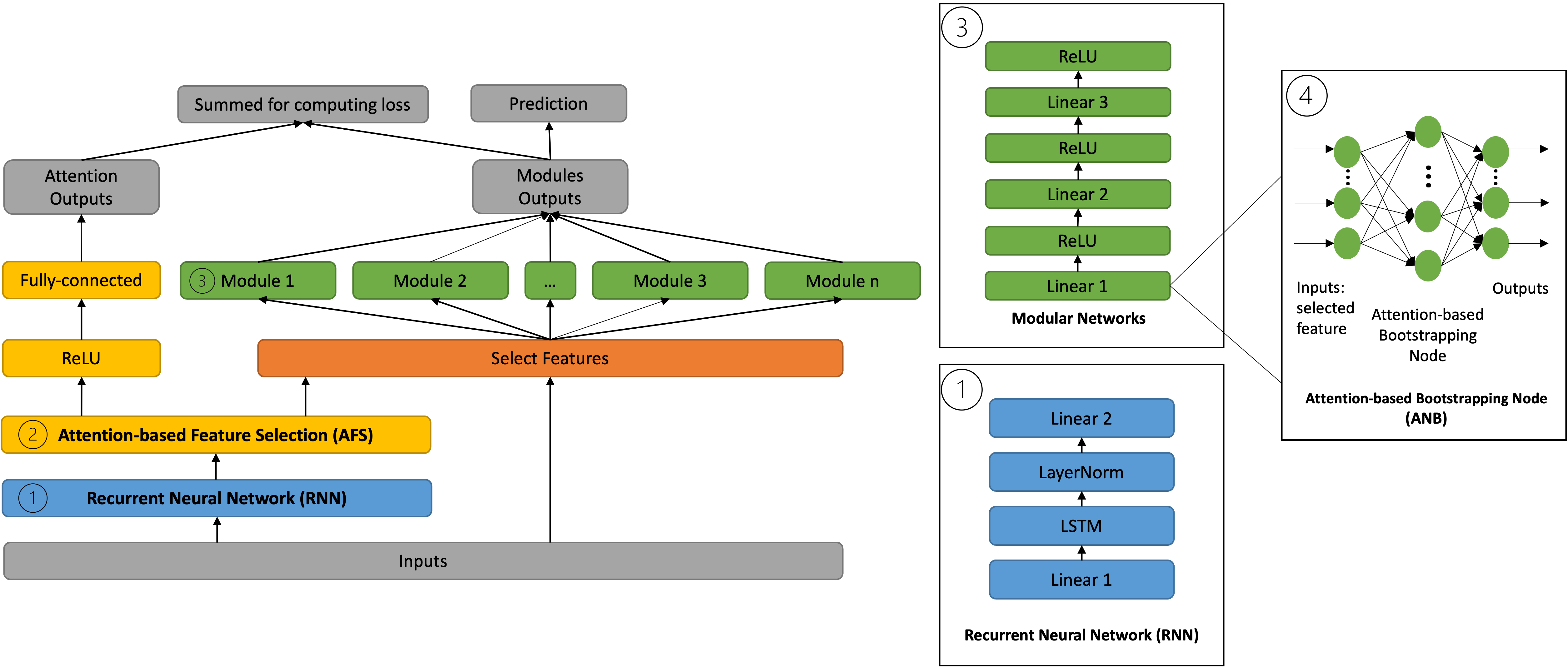

FocusLearn: Fully-Interpretable, High-Performance Modular Neural Networks for Time Series

Qiqi Su, Christos Kloukinas, Artur d'Avila Garcez

Multivariate time series have many applications, from healthcare and meteorology to life science. Although deep learning models have shown excellent predictive performance for time series, they have been criticised for being black-boxes or non-interpretable. This paper proposes a novel modular neural network model for multivariate time series prediction that is interpretable by construction. A recurrent neural network learns the temporal dependencies in the data while an attention-based feature selection component selects the most relevant features and suppresses redundant features used in the learning of the temporal dependencies. A modular deep network is trained from the selected features independently to show the users how features influence outcomes, making the model interpretable. Experimental results show that this approach can outperform state-of-the-art interpretable Neural Additive Models (NAM) and variations thereof in both regression and classification of time series tasks, achieving a predictive performance that is comparable to the top non-interpretable methods for time series, LSTM and XGBoost.

Read more5/6/2024

🏷️

0

Parsimony or Capability? Decomposition Delivers Both in Long-term Time Series Forecasting

Jinliang Deng, Feiyang Ye, Du Yin, Xuan Song, Ivor W. Tsang, Hui Xiong

Long-term time series forecasting (LTSF) represents a critical frontier in time series analysis, characterized by extensive input sequences, as opposed to the shorter spans typical of traditional approaches. While longer sequences inherently offer richer information for enhanced predictive precision, prevailing studies often respond by escalating model complexity. These intricate models can inflate into millions of parameters, resulting in prohibitive parameter scales. Our study demonstrates, through both analytical and empirical evidence, that decomposition is key to containing excessive model inflation while achieving uniformly superior and robust results across various datasets. Remarkably, by tailoring decomposition to the intrinsic dynamics of time series data, our proposed model outperforms existing benchmarks, using over 99 % fewer parameters than the majority of competing methods. Through this work, we aim to unleash the power of a restricted set of parameters by capitalizing on domain characteristics--a timely reminder that in the realm of LTSF, bigger is not invariably better.

Read more5/27/2024