Risk Sensitivity in Markov Games and Multi-Agent Reinforcement Learning: A Systematic Review

0

Sign in to get full access

Overview

- This paper provides a systematic review of research on risk sensitivity in Markov games and multi-agent reinforcement learning.

- It examines how agents can learn to make decisions that balance risk and reward in competitive or collaborative multi-agent settings.

- The review covers a range of techniques, including risk-sensitive reinforcement learning, robust multi-agent learning, and meta-game evaluation frameworks.

Plain English Explanation

In many real-world situations, such as financial markets or strategic decision-making, agents need to carefully balance the potential risks and rewards of their actions. This is particularly true in multi-agent settings, where the decisions of one agent can directly impact the outcomes of others.

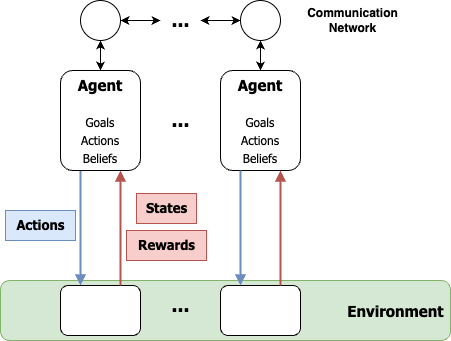

The research reviewed in this paper explores how artificial agents can learn to make risk-sensitive decisions in Markov games - a mathematical model of sequential, strategic interaction between multiple players. The key idea is to develop reinforcement learning algorithms that don't just maximize expected rewards, but also consider the variability or riskiness of those rewards.

For example, an agent trading in a financial market might prefer an investment strategy that provides steady, moderate returns over one that promises higher average returns but also higher volatility and risk of large losses. By incorporating risk-sensitivity into the learning process, the agent can find policies that balance profitability and safety.

The paper covers a range of different approaches to this challenge, including techniques like risk-sensitive reinforcement learning, robust multi-agent learning, and meta-game evaluation frameworks. These methods allow agents to learn policies that are not only high-performing on average, but also resilient to unexpected events or adversarial behavior from other agents.

Technical Explanation

The paper begins by introducing Markov games as a general framework for modeling multi-agent interactions, and discusses how standard reinforcement learning approaches that focus solely on maximizing expected rewards may be insufficient in these settings. The authors then provide an overview of various techniques that have been proposed to incorporate risk sensitivity into multi-agent reinforcement learning.

One key approach is risk-sensitive reinforcement learning, which modifies the reward function to account for not just the expected payoff, but also measures of risk or variability, such as variance or conditional value-at-risk. This can lead to more conservative, risk-averse policies that prioritize reliability over pure performance.

Another line of work explores robust multi-agent learning techniques, which aim to find policies that perform well even in the face of uncertainty about the other agents' behavior or the environment dynamics. This can involve minimax optimization, regret minimization, or other approaches to designing agents that are resilient to adversarial conditions.

The paper also discusses meta-game evaluation frameworks that can be used to assess the performance of risk-sensitive multi-agent policies in complex, competitive scenarios. These frameworks allow researchers to analyze not just the individual agents' rewards, but also higher-level properties like the stability of the overall system and the emergence of cooperative or adversarial dynamics.

Critical Analysis

The review highlights several important limitations and open challenges in this area of research. One key issue is the difficulty of defining appropriate risk measures and incorporating them into the learning process in a principled way. Different risk metrics can lead to very different agent behaviors, and there is often no clear "right" choice.

Another concern is the computational complexity of many of the proposed risk-sensitive algorithms, which can make them challenging to scale to real-world, large-scale problems. The authors note that more efficient and sample-efficient techniques are needed to make these methods practical.

Additionally, the review points out that most of the existing work has focused on relatively simple, stylized multi-agent environments. Applying these risk-sensitive approaches to more realistic, high-stakes domains like finance, cybersecurity, or autonomous vehicle coordination remains an important area for future research.

Finally, the paper raises questions about the broader societal implications of developing risk-sensitive multi-agent systems. While these techniques may lead to more reliable and robust decision-making, they could also amplify existing biases or create new forms of inequality if not carefully designed and deployed.

Conclusion

This systematic review provides a valuable overview of the current state of research on risk sensitivity in Markov games and multi-agent reinforcement learning. The authors have done an excellent job of synthesizing a wide range of techniques and highlighting both the promise and the challenges of this important area of study.

As artificial intelligence systems become increasingly embedded in high-stakes, interactive domains, the ability to learn risk-sensitive policies will be crucial. The insights and open questions raised in this paper can help guide future research and ensure that these advanced AI systems are designed with safety, robustness, and societal impact in mind.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Risk Sensitivity in Markov Games and Multi-Agent Reinforcement Learning: A Systematic Review

Hafez Ghaemi, Shirin Jamshidi, Mohammad Mashreghi, Majid Nili Ahmadabadi, Hamed Kebriaei

Markov games (MGs) and multi-agent reinforcement learning (MARL) are studied to model decision making in multi-agent systems. Traditionally, the objective in MG and MARL has been risk-neutral, i.e., agents are assumed to optimize a performance metric such as expected return, without taking into account subjective or cognitive preferences of themselves or of other agents. However, ignoring such preferences leads to inaccurate models of decision making in many real-world scenarios in finance, operations research, and behavioral economics. Therefore, when these preferences are present, it is necessary to incorporate a suitable measure of risk into the optimization objective of agents, which opens the door to risk-sensitive MG and MARL. In this paper, we systemically review the literature on risk sensitivity in MG and MARL that has been growing in recent years alongside other areas of reinforcement learning and game theory. We define and mathematically describe different risk measures used in MG and MARL and individually for each measure, discuss articles that incorporate it. Finally, we identify recent trends in theoretical and applied works in the field and discuss possible directions of future research.

Read more6/11/2024

🏅

0

Taming Equilibrium Bias in Risk-Sensitive Multi-Agent Reinforcement Learning

Yingjie Fei, Ruitu Xu

We study risk-sensitive multi-agent reinforcement learning under general-sum Markov games, where agents optimize the entropic risk measure of rewards with possibly diverse risk preferences. We show that using the regret naively adapted from existing literature as a performance metric could induce policies with equilibrium bias that favor the most risk-sensitive agents and overlook the other agents. To address such deficiency of the naive regret, we propose a novel notion of regret, which we call risk-balanced regret, and show through a lower bound that it overcomes the issue of equilibrium bias. Furthermore, we develop a self-play algorithm for learning Nash, correlated, and coarse correlated equilibria in risk-sensitive Markov games. We prove that the proposed algorithm attains near-optimal regret guarantees with respect to the risk-balanced regret.

Read more5/7/2024

0

Multi-agent Reinforcement Learning: A Comprehensive Survey

Dom Huh, Prasant Mohapatra

Multi-agent systems (MAS) are widely prevalent and crucially important in numerous real-world applications, where multiple agents must make decisions to achieve their objectives in a shared environment. Despite their ubiquity, the development of intelligent decision-making agents in MAS poses several open challenges to their effective implementation. This survey examines these challenges, placing an emphasis on studying seminal concepts from game theory (GT) and machine learning (ML) and connecting them to recent advancements in multi-agent reinforcement learning (MARL), i.e. the research of data-driven decision-making within MAS. Therefore, the objective of this survey is to provide a comprehensive perspective along the various dimensions of MARL, shedding light on the unique opportunities that are presented in MARL applications while highlighting the inherent challenges that accompany this potential. Therefore, we hope that our work will not only contribute to the field by analyzing the current landscape of MARL but also motivate future directions with insights for deeper integration of concepts from related domains of GT and ML. With this in mind, this work delves into a detailed exploration of recent and past efforts of MARL and its related fields and describes prior solutions that were proposed and their limitations, as well as their applications.

Read more7/4/2024

0

Pessimism Meets Risk: Risk-Sensitive Offline Reinforcement Learning

Dake Zhang, Boxiang Lyu, Shuang Qiu, Mladen Kolar, Tong Zhang

We study risk-sensitive reinforcement learning (RL), a crucial field due to its ability to enhance decision-making in scenarios where it is essential to manage uncertainty and minimize potential adverse outcomes. Particularly, our work focuses on applying the entropic risk measure to RL problems. While existing literature primarily investigates the online setting, there remains a large gap in understanding how to efficiently derive a near-optimal policy based on this risk measure using only a pre-collected dataset. We center on the linear Markov Decision Process (MDP) setting, a well-regarded theoretical framework that has yet to be examined from a risk-sensitive standpoint. In response, we introduce two provably sample-efficient algorithms. We begin by presenting a risk-sensitive pessimistic value iteration algorithm, offering a tight analysis by leveraging the structure of the risk-sensitive performance measure. To further improve the obtained bounds, we propose another pessimistic algorithm that utilizes variance information and reference-advantage decomposition, effectively improving both the dependence on the space dimension $d$ and the risk-sensitivity factor. To the best of our knowledge, we obtain the first provably efficient risk-sensitive offline RL algorithms.

Read more7/11/2024