Stochastic Optimization Algorithms for Instrumental Variable Regression with Streaming Data

2405.19463

0

0

Abstract

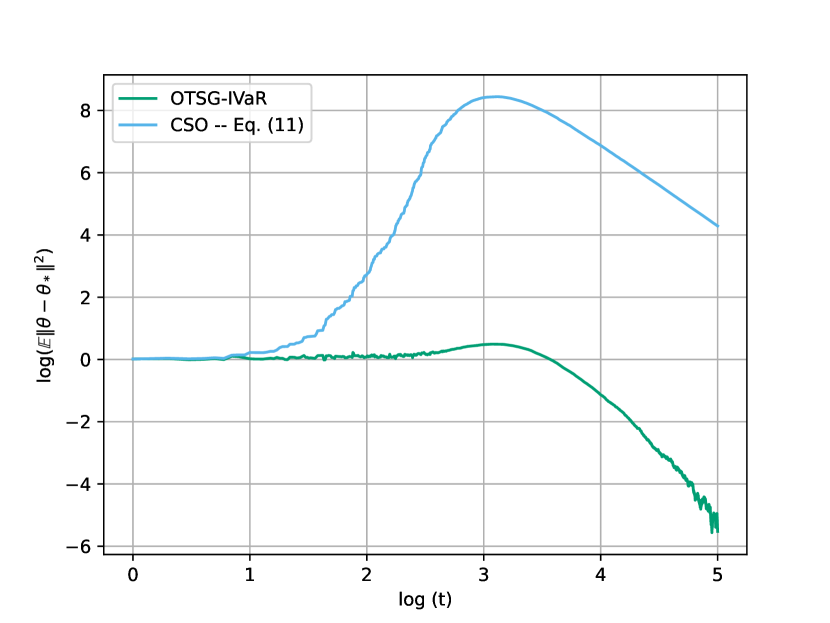

We develop and analyze algorithms for instrumental variable regression by viewing the problem as a conditional stochastic optimization problem. In the context of least-squares instrumental variable regression, our algorithms neither require matrix inversions nor mini-batches and provides a fully online approach for performing instrumental variable regression with streaming data. When the true model is linear, we derive rates of convergence in expectation, that are of order $mathcal{O}(log T/T)$ and $mathcal{O}(1/T^{1-iota})$ for any $iota>0$, respectively under the availability of two-sample and one-sample oracles, respectively, where $T$ is the number of iterations. Importantly, under the availability of the two-sample oracle, our procedure avoids explicitly modeling and estimating the relationship between confounder and the instrumental variables, demonstrating the benefit of the proposed approach over recent works based on reformulating the problem as minimax optimization problems. Numerical experiments are provided to corroborate the theoretical results.

Create account to get full access

Overview

- This paper presents stochastic optimization algorithms for instrumental variable (IV) regression with streaming data.

- The authors develop two new algorithms, Stochastic Approximate Instrumental Variable (SAIV) and Adaptive Debiased Stochastic Gradient Descent (ADSGD), and provide convergence analysis for both.

- The proposed algorithms are designed to handle high-dimensional settings and streaming data, making them applicable to a wide range of real-world problems.

Plain English Explanation

Instrumental variable (IV) regression is a powerful statistical technique used to estimate causal relationships, even in the presence of confounding factors. However, traditional IV regression methods can be computationally expensive and struggle with high-dimensional data or streaming data (data that arrives continuously over time).

The researchers in this paper have developed new algorithms, SAIV and ADSGD, that address these challenges. These algorithms use stochastic optimization techniques to efficiently estimate the IV regression model, even when dealing with large numbers of variables or data that is constantly being updated.

The key innovations of these algorithms are:

- Scalability: The algorithms can handle high-dimensional data, making them suitable for modern, data-rich applications.

- Streaming data: The algorithms can continuously update the model as new data becomes available, without the need to re-process the entire dataset.

- Convergence guarantees: The researchers have proven that their algorithms will converge to the optimal solution, even in these challenging settings.

By overcoming the limitations of traditional IV regression methods, these new algorithms have the potential to significantly expand the application of causal inference techniques in fields like economics, epidemiology, and social science, where understanding causal relationships is crucial.

Technical Explanation

The paper introduces two new stochastic optimization algorithms for instrumental variable (IV) regression with streaming data: Stochastic Approximate Instrumental Variable (SAIV) and Adaptive Debiased Stochastic Gradient Descent (ADSGD).

The SAIV algorithm is a nonparametric approach that uses kernel functions to estimate the IV regression model. It updates the model parameters using stochastic approximation, which allows it to efficiently handle high-dimensional data and streaming data. The authors prove that SAIV converges to the optimal solution under suitable conditions.

The ADSGD algorithm, on the other hand, is a debiased stochastic gradient descent method designed for high-dimensional generalized linear models, including IV regression. By incorporating an adaptive debiasing step, ADSGD is able to provide accurate estimates even in settings with a large number of variables. The authors establish convergence guarantees for ADSGD in the streaming data setting.

Both algorithms are evaluated on simulated data and real-world datasets, demonstrating their effectiveness in handling high-dimensional and streaming data challenges. The results show that the proposed methods outperform traditional IV regression techniques, particularly in terms of computational efficiency and scalability.

Critical Analysis

The paper presents a well-designed and rigorous study, with solid theoretical foundations and extensive empirical evaluation. The authors have addressed important practical challenges in IV regression, such as high-dimensionality and streaming data, which are crucial for many real-world applications.

One potential limitation of the research is the assumption of linear or generalized linear models. While these are commonly used in practice, there may be situations where more flexible nonparametric models are required. The authors acknowledge this and suggest extending their work to more general function classes as a future research direction.

Additionally, the paper does not consider the impact of data quality or potential violations of the instrumental variable assumptions, such as weak instruments or the presence of unmeasured confounders. These issues can significantly affect the validity of the causal inferences drawn from IV regression and should be carefully examined in real-world applications.

Finally, the paper focuses on the computational and statistical properties of the proposed algorithms, but does not delve into their practical implementation or computational complexity. A more detailed discussion of the practical considerations and scalability of these methods would be valuable for researchers and practitioners looking to apply them in their work.

Conclusion

This paper presents two novel stochastic optimization algorithms, SAIV and ADSGD, for instrumental variable regression with high-dimensional and streaming data. The proposed methods address important limitations of traditional IV regression techniques, such as computational efficiency and scalability, making them well-suited for modern, data-rich applications.

The theoretical analysis and empirical evaluations demonstrate the effectiveness of the algorithms in handling challenging data settings. By expanding the capabilities of causal inference techniques, this research has the potential to significantly impact fields where understanding causal relationships is critical, such as economics, epidemiology, and social science.

As the authors suggest, future work could explore extensions to more flexible nonparametric models and address practical concerns related to data quality and the validity of instrumental variable assumptions. Overall, this paper represents an important contribution to the field of causal inference and stochastic optimization.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

↗️

Nonparametric Instrumental Variable Regression through Stochastic Approximate Gradients

Yuri Fonseca, Caio Peixoto, Yuri Saporito

0

0

Instrumental variables (IVs) provide a powerful strategy for identifying causal effects in the presence of unobservable confounders. Within the nonparametric setting (NPIV), recent methods have been based on nonlinear generalizations of Two-Stage Least Squares and on minimax formulations derived from moment conditions or duality. In a novel direction, we show how to formulate a functional stochastic gradient descent algorithm to tackle NPIV regression by directly minimizing the populational risk. We provide theoretical support in the form of bounds on the excess risk, and conduct numerical experiments showcasing our method's superior stability and competitive performance relative to current state-of-the-art alternatives. This algorithm enables flexible estimator choices, such as neural networks or kernel based methods, as well as non-quadratic loss functions, which may be suitable for structural equations beyond the setting of continuous outcomes and additive noise. Finally, we demonstrate this flexibility of our framework by presenting how it naturally addresses the important case of binary outcomes, which has received far less attention by recent developments in the NPIV literature.

5/27/2024

Adaptive debiased SGD in high-dimensional GLMs with steaming data

Ruijian Han, Lan Luo, Yuanhang Luo, Yuanyuan Lin, Jian Huang

0

0

Online statistical inference facilitates real-time analysis of sequentially collected data, making it different from traditional methods that rely on static datasets. This paper introduces a novel approach to online inference in high-dimensional generalized linear models, where we update regression coefficient estimates and their standard errors upon each new data arrival. In contrast to existing methods that either require full dataset access or large-dimensional summary statistics storage, our method operates in a single-pass mode, significantly reducing both time and space complexity. The core of our methodological innovation lies in an adaptive stochastic gradient descent algorithm tailored for dynamic objective functions, coupled with a novel online debiasing procedure. This allows us to maintain low-dimensional summary statistics while effectively controlling optimization errors introduced by the dynamically changing loss functions. We demonstrate that our method, termed the Approximated Debiased Lasso (ADL), not only mitigates the need for the bounded individual probability condition but also significantly improves numerical performance. Numerical experiments demonstrate that the proposed ADL method consistently exhibits robust performance across various covariance matrix structures.

6/4/2024

↗️

Convergence analysis of online algorithms for vector-valued kernel regression

Michael Griebel, Peter Oswald

0

0

We consider the problem of approximating the regression function from noisy vector-valued data by an online learning algorithm using an appropriate reproducing kernel Hilbert space (RKHS) as prior. In an online algorithm, i.i.d. samples become available one by one by a random process and are successively processed to build approximations to the regression function. We are interested in the asymptotic performance of such online approximation algorithms and show that the expected squared error in the RKHS norm can be bounded by $C^2 (m+1)^{-s/(2+s)}$, where $m$ is the current number of processed data, the parameter $0<sleq 1$ expresses an additional smoothness assumption on the regression function and the constant $C$ depends on the variance of the input noise, the smoothness of the regression function and further parameters of the algorithm.

4/30/2024

Geometry-Aware Instrumental Variable Regression

Heiner Kremer, Bernhard Scholkopf

0

0

Instrumental variable (IV) regression can be approached through its formulation in terms of conditional moment restrictions (CMR). Building on variants of the generalized method of moments, most CMR estimators are implicitly based on approximating the population data distribution via reweightings of the empirical sample. While for large sample sizes, in the independent identically distributed (IID) setting, reweightings can provide sufficient flexibility, they might fail to capture the relevant information in presence of corrupted data or data prone to adversarial attacks. To address these shortcomings, we propose the Sinkhorn Method of Moments, an optimal transport-based IV estimator that takes into account the geometry of the data manifold through data-derivative information. We provide a simple plug-and-play implementation of our method that performs on par with related estimators in standard settings but improves robustness against data corruption and adversarial attacks.

5/21/2024