Survey of Data-driven Newsvendor: Unified Analysis and Spectrum of Achievable Regrets

0

🌐

Sign in to get full access

Overview

- The paper provides a comprehensive survey of data-driven newsvendor models, analyzing a spectrum of achievable regrets.

- It presents a unified analysis framework and new results, improving understanding of the newsvendor problem.

- Key insights include quantifying the value of additional data and identifying optimal models for different problem settings.

Plain English Explanation

The newsvendor problem is a classic business challenge where a retailer must decide how much inventory to order before knowing the exact future demand. This paper offers a detailed analysis of data-driven approaches to solving this problem.

The authors establish a unified framework for understanding different data-driven newsvendor models. They compare the performance of these models, quantifying the benefits of having more data. This helps retailers make more informed decisions about how much data they need to collect and what modeling techniques to use.

For example, the paper shows that a simple "sample average approximation" approach can perform well when data is limited, while more advanced techniques like "upper confidence bounds" deliver better results as more data becomes available. The analysis provides guidance on choosing the right model for the problem at hand.

The researchers also identify the limits of what can be achieved with data-driven newsvendor models, characterizing the "spectrum of achievable regrets." This gives retailers a sense of the best-case performance they can expect, informing their inventory planning and risk management strategies.

Overall, the paper advances the state of the art in data-driven newsvendor research, offering insights that can help businesses make more effective inventory decisions.

Technical Explanation

The newsvendor problem is a classic operations research challenge that models the decision of how much inventory to order before uncertain future demand is realized. This paper provides a comprehensive survey of data-driven approaches to the newsvendor problem, analyzing a unified framework and spectrum of achievable regrets.

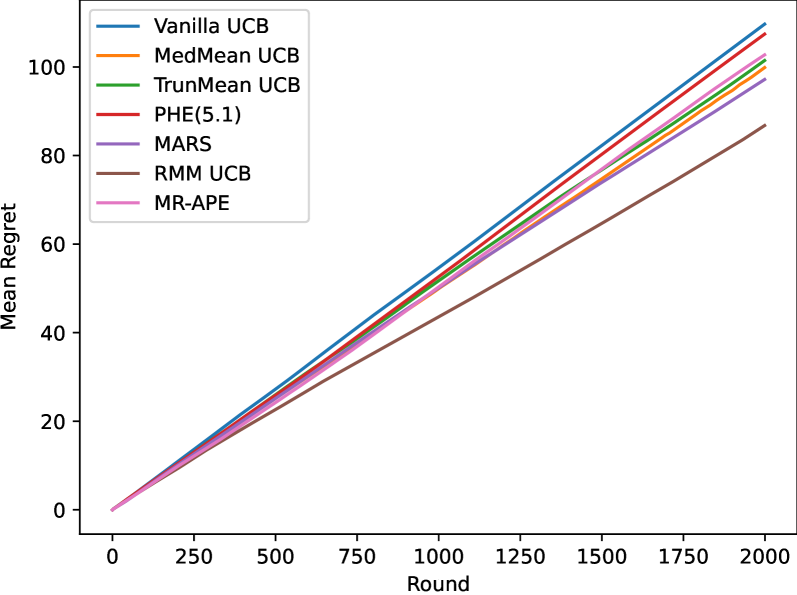

The authors begin by establishing a general model for data-driven newsvendor problems. They then review and unify the analysis of several classes of data-driven newsvendor policies, including sample average approximation, upper confidence bounds, and swap regret minimization. For each policy, they characterize the achievable regret as a function of the available data.

Key results include quantifying the value of additional data and identifying the optimal models for different problem settings. For example, the analysis shows that simple sample average approximation can perform well with limited data, while more advanced techniques like upper confidence bounds deliver better results as more data becomes available.

The paper also identifies fundamental limits on the performance of data-driven newsvendor policies, characterizing the "spectrum of achievable regrets." This provides retailers with a sense of the best-case performance they can expect, informing their inventory planning and risk management strategies.

The unified analysis framework and new insights presented in this work advance the state of the art in data-driven newsvendor research. The findings can help businesses make more effective inventory decisions by guiding their choice of modeling approach and data collection efforts.

Critical Analysis

The paper provides a comprehensive and rigorous analysis of data-driven newsvendor models, addressing an important practical problem. The authors' unified framework and characterization of the spectrum of achievable regrets are valuable contributions that improve our understanding of the newsvendor problem.

However, the analysis does not consider some real-world complexities that could affect the applicability of the results. For instance, the paper assumes demand follows a known probability distribution, whereas in practice, demand forecasting often involves significant uncertainty. Further research could explore the performance of these models under more realistic demand scenarios.

Additionally, the paper focuses on single-product newsvendor problems. Extensions to multi-product or network-level inventory decisions could provide additional insights for larger-scale retail operations.

Finally, the analysis is primarily theoretical, and more empirical studies comparing the practical performance of these data-driven policies would help validate the findings and guide real-world implementation.

Overall, this paper makes an important contribution to the literature on data-driven newsvendor models. The insights provided can inform inventory management practices, but further research is needed to address some of the limitations and expand the applicability of the results.

Conclusion

This survey paper offers a unified analysis of data-driven newsvendor models, quantifying the value of additional data and identifying optimal modeling approaches for different problem settings. The characterization of the spectrum of achievable regrets provides retailers with a benchmark for evaluating their inventory planning strategies.

The findings can help businesses make more effective inventory decisions by guiding their choice of data-driven modeling techniques and data collection efforts. While the analysis has some limitations, the paper represents a significant advancement in our understanding of the newsvendor problem and points the way for future research in this area.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

🌐

0

Survey of Data-driven Newsvendor: Unified Analysis and Spectrum of Achievable Regrets

Zhuoxin Chen, Will Ma

In the Newsvendor problem, the goal is to guess the number that will be drawn from some distribution, with asymmetric consequences for guessing too high vs. too low. In the data-driven version, the distribution is unknown, and one must work with samples from the distribution. Data-driven Newsvendor has been studied under many variants: additive vs. multiplicative regret, high probability vs. expectation bounds, and different distribution classes. This paper studies all combinations of these variants, filling in many gaps in the literature and simplifying many proofs. In particular, we provide a unified analysis based on the notion of clustered distributions, which in conjunction with our new lower bounds, shows that the entire spectrum of regrets between $1/sqrt{n}$ and $1/n$ can be possible.

Read more9/18/2024

0

Closing the Gaps: Optimality of Sample Average Approximation for Data-Driven Newsvendor Problems

Jiameng Lyu, Shilin Yuan, Bingkun Zhou, Yuan Zhou

We study the regret performance of Sample Average Approximation (SAA) for data-driven newsvendor problems with general convex inventory costs. In literature, the optimality of SAA has not been fully established under both alpha-global strong convexity and (alpha,beta)-local strong convexity (alpha-strongly convex within the beta-neighborhood of the optimal quantity) conditions. This paper closes the gaps between regret upper and lower bounds for both conditions. Under the (alpha,beta)-local strong convexity condition, we prove the optimal regret bound of Theta(log T/alpha + 1/ (alphabeta)) for SAA. This upper bound result demonstrates that the regret performance of SAA is only influenced by alpha and not by beta in the long run, enhancing our understanding about how local properties affect the long-term regret performance of decision-making strategies. Under the alpha-global strong convexity condition, we demonstrate that the worst-case regret of any data-driven method is lower bounded by Omega(log T/alpha), which is the first lower bound result that matches the existing upper bound with respect to both parameter alpha and time horizon T. Along the way, we propose to analyze the SAA regret via a new gradient approximation technique, as well as a new class of smooth inverted-hat-shaped hard problem instances that might be of independent interest for the lower bounds of broader data-driven problems.

Read more7/9/2024

0

Data-Driven Upper Confidence Bounds with Near-Optimal Regret for Heavy-Tailed Bandits

Ambrus Tam'as, Szabolcs Szentp'eteri, Bal'azs Csan'ad Cs'aji

Stochastic multi-armed bandits (MABs) provide a fundamental reinforcement learning model to study sequential decision making in uncertain environments. The upper confidence bounds (UCB) algorithm gave birth to the renaissance of bandit algorithms, as it achieves near-optimal regret rates under various moment assumptions. Up until recently most UCB methods relied on concentration inequalities leading to confidence bounds which depend on moment parameters, such as the variance proxy, that are usually unknown in practice. In this paper, we propose a new distribution-free, data-driven UCB algorithm for symmetric reward distributions, which needs no moment information. The key idea is to combine a refined, one-sided version of the recently developed resampled median-of-means (RMM) method with UCB. We prove a near-optimal regret bound for the proposed anytime, parameter-free RMM-UCB method, even for heavy-tailed distributions.

Read more6/11/2024

🤖

0

Forecasting for Swap Regret for All Downstream Agents

Aaron Roth, Mirah Shi

We study the problem of making predictions so that downstream agents who best respond to them will be guaranteed diminishing swap regret, no matter what their utility functions are. It has been known since Foster and Vohra (1997) that agents who best-respond to calibrated forecasts have no swap regret. Unfortunately, the best known algorithms for guaranteeing calibrated forecasts in sequential adversarial environments do so at rates that degrade exponentially with the dimension of the prediction space. In this work, we show that by making predictions that are not calibrated, but are unbiased subject to a carefully selected collection of events, we can guarantee arbitrary downstream agents diminishing swap regret at rates that substantially improve over the rates that result from calibrated forecasts -- while maintaining the appealing property that our forecasts give guarantees for any downstream agent, without our forecasting algorithm needing to know their utility function. We give separate results in the ``low'' (1 or 2) dimensional setting and the ``high'' ($> 2$) dimensional setting. In the low dimensional setting, we show how to make predictions such that all agents who best respond to our predictions have diminishing swap regret -- in 1 dimension, at the optimal $O(sqrt{T})$ rate. In the high dimensional setting we show how to make forecasts that guarantee regret scaling at a rate of $O(T^{2/3})$ (crucially, a dimension independent exponent), under the assumption that downstream agents smoothly best respond. Our results stand in contrast to rates that derive from agents who best respond to calibrated forecasts, which have an exponential dependence on the dimension of the prediction space.

Read more6/18/2024