Text2TimeSeries: Enhancing Financial Forecasting through Time Series Prediction Updates with Event-Driven Insights from Large Language Models

0

Sign in to get full access

Overview

- Text2TimeSeries is a novel approach that enhances financial time series forecasting by integrating insights from large language models.

- It addresses the challenges of updating time series predictions based on real-world events and news.

- The system leverages the rich context and knowledge captured in large language models to provide event-driven updates to financial time series forecasts.

Plain English Explanation

The paper introduces Text2TimeSeries, a new technique that aims to improve financial forecasting by combining time series models with insights from large language models. Traditional time series forecasting methods can struggle to quickly adapt to real-world events and news that may impact the future trajectory of financial data.

Text2TimeSeries addresses this by using large language models, which are AI systems trained on vast amounts of text data. These models can understand the rich context and meaning behind news and events, and the paper shows how this knowledge can be used to dynamically update time series predictions. For example, if a significant news event occurs that is likely to affect a stock price, the language model can detect the importance of this event and feed that information back into the time series model to adjust the forecast.

By integrating these two complementary approaches - time series modeling and natural language processing - the researchers believe Text2TimeSeries can produce more accurate and up-to-date financial forecasts that are better able to adapt to the evolving business environment.

Technical Explanation

The core of the Text2TimeSeries approach is to leverage the event understanding capabilities of large language models to enhance time series forecasting. The system takes in both structured financial time series data as well as unstructured text data, such as news articles and social media posts.

The language model is used to extract relevant insights and events from the text data, which are then fed into the time series forecasting model to update and refine the predictions. This allows the system to quickly adapt the forecasts based on new information that may impact the future trajectory of the financial data.

The authors evaluate Text2TimeSeries on real-world financial datasets and find that it outperforms traditional time series models in terms of forecasting accuracy, especially when significant events occur that impact the data. The language model component is shown to be crucial in enabling the system to detect and respond to these event-driven changes.

Critical Analysis

The paper presents a compelling approach to improving financial forecasting by leveraging large language models. However, some potential limitations and areas for future work are worth noting:

- The authors focus on a specific financial use case, but the general principles of the Text2TimeSeries framework could potentially be applied to other time series forecasting domains beyond finance.

- The evaluation is conducted on a limited set of datasets, so further testing on a broader range of financial time series data would help validate the generalizability of the approach.

- While the language model component shows promise, the authors do not fully explore the potential limitations or biases that large language models may introduce into the forecasting process.

- Integrating the time series and language model components is a technical challenge, and the authors could provide more details on the specific architecture and training procedures used.

Overall, Text2TimeSeries represents an interesting and potentially impactful advancement in the field of time series forecasting, with the integration of large language models as a key innovative aspect. Further research and real-world deployment could shed light on the broader applicability and limitations of this approach.

Conclusion

The Text2TimeSeries paper presents a novel technique that aims to enhance financial time series forecasting by incorporating insights from large language models. By leveraging the rich contextual understanding of language models, the system can more effectively adapt time series predictions to account for relevant real-world events and news.

The key contribution of this research is demonstrating the potential benefits of combining structured time series modeling with unstructured text data analysis, which could have significant implications for improving the accuracy and responsiveness of financial forecasts. As large language models continue to advance, techniques like Text2TimeSeries may become increasingly important tools for making sense of complex, evolving data landscapes.

Future work exploring the broader applications of this approach, as well as addressing potential limitations, could further strengthen the impact of this research on the field of time series forecasting and beyond.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Text2TimeSeries: Enhancing Financial Forecasting through Time Series Prediction Updates with Event-Driven Insights from Large Language Models

Litton Jose Kurisinkel, Pruthwik Mishra, Yue Zhang

Time series models, typically trained on numerical data, are designed to forecast future values. These models often rely on weighted averaging techniques over time intervals. However, real-world time series data is seldom isolated and is frequently influenced by non-numeric factors. For instance, stock price fluctuations are impacted by daily random events in the broader world, with each event exerting a unique influence on price signals. Previously, forecasts in financial markets have been approached in two main ways: either as time-series problems over price sequence or sentiment analysis tasks. The sentiment analysis tasks aim to determine whether news events will have a positive or negative impact on stock prices, often categorizing them into discrete labels. Recognizing the need for a more comprehensive approach to accurately model time series prediction, we propose a collaborative modeling framework that incorporates textual information about relevant events for predictions. Specifically, we leverage the intuition of large language models about future changes to update real number time series predictions. We evaluated the effectiveness of our approach on financial market data.

Read more7/8/2024

0

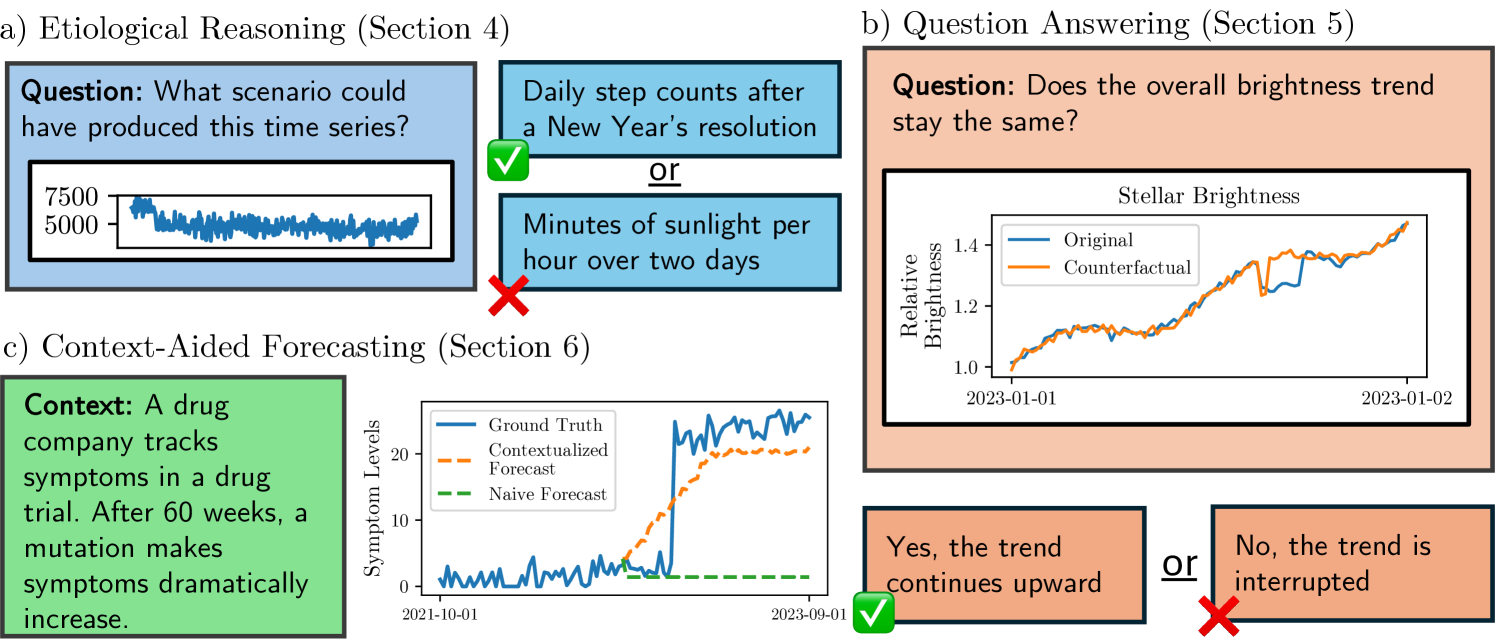

Language Models Still Struggle to Zero-shot Reason about Time Series

Mike A. Merrill, Mingtian Tan, Vinayak Gupta, Tom Hartvigsen, Tim Althoff

Time series are critical for decision-making in fields like finance and healthcare. Their importance has driven a recent influx of works passing time series into language models, leading to non-trivial forecasting on some datasets. But it remains unknown whether non-trivial forecasting implies that language models can reason about time series. To address this gap, we generate a first-of-its-kind evaluation framework for time series reasoning, including formal tasks and a corresponding dataset of multi-scale time series paired with text captions across ten domains. Using these data, we probe whether language models achieve three forms of reasoning: (1) Etiological Reasoning - given an input time series, can the language model identify the scenario that most likely created it? (2) Question Answering - can a language model answer factual questions about time series? (3) Context-Aided Forecasting - does highly relevant textual context improve a language model's time series forecasts? We find that otherwise highly-capable language models demonstrate surprisingly limited time series reasoning: they score marginally above random on etiological and question answering tasks (up to 30 percentage points worse than humans) and show modest success in using context to improve forecasting. These weakness showcase that time series reasoning is an impactful, yet deeply underdeveloped direction for language model research. We also make our datasets and code public at to support further research in this direction at https://github.com/behavioral-data/TSandLanguage

Read more4/19/2024

0

New!StockTime: A Time Series Specialized Large Language Model Architecture for Stock Price Prediction

Shengkun Wang, Taoran Ji, Linhan Wang, Yanshen Sun, Shang-Ching Liu, Amit Kumar, Chang-Tien Lu

The stock price prediction task holds a significant role in the financial domain and has been studied for a long time. Recently, large language models (LLMs) have brought new ways to improve these predictions. While recent financial large language models (FinLLMs) have shown considerable progress in financial NLP tasks compared to smaller pre-trained language models (PLMs), challenges persist in stock price forecasting. Firstly, effectively integrating the modalities of time series data and natural language to fully leverage these capabilities remains complex. Secondly, FinLLMs focus more on analysis and interpretability, which can overlook the essential features of time series data. Moreover, due to the abundance of false and redundant information in financial markets, models often produce less accurate predictions when faced with such input data. In this paper, we introduce StockTime, a novel LLM-based architecture designed specifically for stock price data. Unlike recent FinLLMs, StockTime is specifically designed for stock price time series data. It leverages the natural ability of LLMs to predict the next token by treating stock prices as consecutive tokens, extracting textual information such as stock correlations, statistical trends and timestamps directly from these stock prices. StockTime then integrates both textual and time series data into the embedding space. By fusing this multimodal data, StockTime effectively predicts stock prices across arbitrary look-back periods. Our experiments demonstrate that StockTime outperforms recent LLMs, as it gives more accurate predictions while reducing memory usage and runtime costs.

Read more9/16/2024

0

An Evaluation of Standard Statistical Models and LLMs on Time Series Forecasting

Rui Cao, Qiao Wang

This research examines the use of Large Language Models (LLMs) in predicting time series, with a specific focus on the LLMTIME model. Despite the established effectiveness of LLMs in tasks such as text generation, language translation, and sentiment analysis, this study highlights the key challenges that large language models encounter in the context of time series prediction. We assess the performance of LLMTIME across multiple datasets and introduce classical almost periodic functions as time series to gauge its effectiveness. The empirical results indicate that while large language models can perform well in zero-shot forecasting for certain datasets, their predictive accuracy diminishes notably when confronted with diverse time series data and traditional signals. The primary finding of this study is that the predictive capacity of LLMTIME, similar to other LLMs, significantly deteriorates when dealing with time series data that contain both periodic and trend components, as well as when the signal comprises complex frequency components.

Read more8/12/2024