TSCMamba: Mamba Meets Multi-View Learning for Time Series Classification

0

Sign in to get full access

Overview

- This paper introduces a new time series classification model called TSCMamba, which combines the Mamba time series forecasting technique with multi-view learning for improved performance.

- The key ideas are to leverage multiple representations of the time series data (the "multi-view" aspect) and to incorporate the Mamba model's ability to capture complex patterns in the data.

- The authors demonstrate that TSCMamba outperforms existing state-of-the-art time series classification methods on a range of benchmark datasets.

Plain English Explanation

The researchers developed a new machine learning model called TSCMamba for classifying time series data. Time series data refers to observations collected over time, like stock prices or weather measurements. Classifying time series data means predicting which category or class a particular time series belongs to, like predicting whether a stock will go up or down.

TSCMamba combines two key ideas to improve time series classification. First, it uses "multi-view learning," which means it looks at the time series data in multiple different ways or "views" to get a more complete understanding. This could include things like looking at the overall trend of the data, the patterns in the variations, and the relationships between different measurements.

The second key idea is to incorporate the Mamba time series forecasting model into the classification process. Mamba is a powerful technique for modeling complex patterns in time series data. By leveraging Mamba's capabilities, TSCMamba can better capture the underlying structure of the time series, which helps it make more accurate classifications.

The researchers show that TSCMamba outperforms other state-of-the-art time series classification methods on a variety of benchmark datasets. This suggests that the combination of multi-view learning and the Mamba forecasting model is an effective approach for this important machine learning problem.

Technical Explanation

The core of the TSCMamba model is the integration of Mamba, a powerful time series forecasting technique, with a multi-view learning framework for time series classification.

The multi-view learning aspect involves extracting multiple representations of the input time series data, such as trend, seasonality, and residual components. These different "views" of the data are then fed into separate neural network modules, which learn to classify the time series based on their respective perspectives.

To incorporate the Mamba model, the authors use its state-space representation to capture the complex temporal dynamics in the time series. The Mamba module outputs forecasts, which are then used as additional features for the multi-view classification model. This allows TSCMamba to leverage Mamba's ability to model intricate patterns in the data to improve overall classification performance.

The authors evaluate TSCMamba on a range of publicly available time series classification benchmarks, including the UCR Time Series Classification Archive. They demonstrate that TSCMamba outperforms other state-of-the-art methods, such as TCMIL and BiMamba, on both univariate and multivariate time series classification tasks.

Critical Analysis

The authors provide a thorough evaluation of TSCMamba and highlight its advantages over existing methods. However, the paper does not address some potential limitations or areas for future research.

For example, the authors do not discuss the computational complexity or training time of TSCMamba compared to other models. As the model combines multiple neural network modules and the Mamba forecasting component, it may have higher computational requirements, which could be a concern for real-world applications.

Additionally, the paper does not explore the interpretability of the TSCMamba model. Understanding how the different components of the model contribute to the final classification decisions could be important, especially in domains where explainability is a key concern, such as healthcare or finance.

Further research could also investigate the performance of TSCMamba on larger and more diverse time series datasets, as well as its robustness to noisy or missing data, which are common challenges in real-world time series analysis.

Conclusion

The TSCMamba model proposed in this paper represents an interesting advancement in time series classification by leveraging the strengths of multi-view learning and the Mamba time series forecasting technique. The authors demonstrate that this combination can outperform other state-of-the-art methods on benchmark datasets, suggesting that TSCMamba could be a valuable tool for a wide range of applications that involve classifying time series data, such as financial analysis, climate modeling, and activity recognition.

While the paper provides a solid technical foundation and experimental validation, further research is needed to fully understand the model's limitations and explore potential extensions or improvements. Nonetheless, the core ideas presented in this work contribute to the ongoing efforts to develop more accurate and robust time series classification models, which can have significant impacts across various domains.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

TSCMamba: Mamba Meets Multi-View Learning for Time Series Classification

Md Atik Ahamed, Qiang Cheng

Time series classification (TSC) on multivariate time series is a critical problem. We propose a novel multi-view approach integrating frequency-domain and time-domain features to provide complementary contexts for TSC. Our method fuses continuous wavelet transform spectral features with temporal convolutional or multilayer perceptron features. We leverage the Mamba state space model for efficient and scalable sequence modeling. We also introduce a novel tango scanning scheme to better model sequence relationships. Experiments on 10 standard benchmark datasets demonstrate our approach achieves an average 6.45% accuracy improvement over state-of-the-art TSC models.

Read more6/10/2024

0

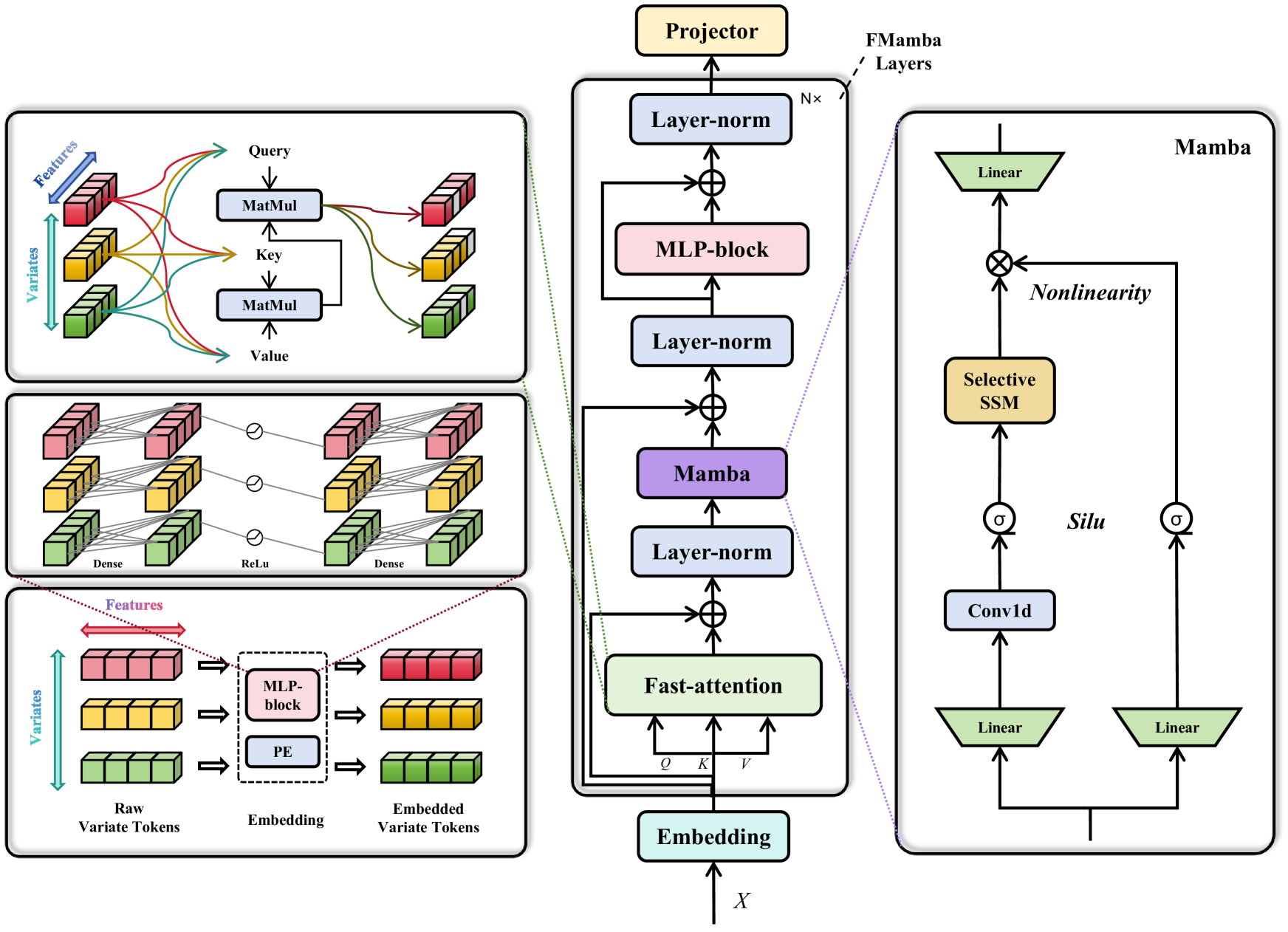

FMamba: Mamba based on Fast-attention for Multivariate Time-series Forecasting

Shusen Ma, Yu Kang, Peng Bai, Yun-Bo Zhao

In multivariate time-series forecasting (MTSF), extracting the temporal correlations of the input sequences is crucial. While popular Transformer-based predictive models can perform well, their quadratic computational complexity results in inefficiency and high overhead. The recently emerged Mamba, a selective state space model, has shown promising results in many fields due to its strong temporal feature extraction capabilities and linear computational complexity. However, due to the unilateral nature of Mamba, channel-independent predictive models based on Mamba cannot attend to the relationships among all variables in the manner of Transformer-based models. To address this issue, we combine fast-attention with Mamba to introduce a novel framework named FMamba for MTSF. Technically, we first extract the temporal features of the input variables through an embedding layer, then compute the dependencies among input variables via the fast-attention module. Subsequently, we use Mamba to selectively deal with the input features and further extract the temporal dependencies of the variables through the multi-layer perceptron block (MLP-block). Finally, FMamba obtains the predictive results through the projector, a linear layer. Experimental results on eight public datasets demonstrate that FMamba can achieve state-of-the-art performance while maintaining low computational overhead.

Read more7/23/2024

0

Bi-Mamba+: Bidirectional Mamba for Time Series Forecasting

Aobo Liang, Xingguo Jiang, Yan Sun, Xiaohou Shi, Ke Li

Long-term time series forecasting (LTSF) provides longer insights into future trends and patterns. Over the past few years, deep learning models especially Transformers have achieved advanced performance in LTSF tasks. However, LTSF faces inherent challenges such as long-term dependencies capturing and sparse semantic characteristics. Recently, a new state space model (SSM) named Mamba is proposed. With the selective capability on input data and the hardware-aware parallel computing algorithm, Mamba has shown great potential in balancing predicting performance and computational efficiency compared to Transformers. To enhance Mamba's ability to preserve historical information in a longer range, we design a novel Mamba+ block by adding a forget gate inside Mamba to selectively combine the new features with the historical features in a complementary manner. Furthermore, we apply Mamba+ both forward and backward and propose Bi-Mamba+, aiming to promote the model's ability to capture interactions among time series elements. Additionally, multivariate time series data in different scenarios may exhibit varying emphasis on intra- or inter-series dependencies. Therefore, we propose a series-relation-aware decider that controls the utilization of channel-independent or channel-mixing tokenization strategy for specific datasets. Extensive experiments on 8 real-world datasets show that our model achieves more accurate predictions compared with state-of-the-art methods.

Read more6/28/2024

0

MambaTS: Improved Selective State Space Models for Long-term Time Series Forecasting

Xiuding Cai, Yaoyao Zhu, Xueyao Wang, Yu Yao

In recent years, Transformers have become the de-facto architecture for long-term sequence forecasting (LTSF), but faces challenges such as quadratic complexity and permutation invariant bias. A recent model, Mamba, based on selective state space models (SSMs), has emerged as a competitive alternative to Transformer, offering comparable performance with higher throughput and linear complexity related to sequence length. In this study, we analyze the limitations of current Mamba in LTSF and propose four targeted improvements, leading to MambaTS. We first introduce variable scan along time to arrange the historical information of all the variables together. We suggest that causal convolution in Mamba is not necessary for LTSF and propose the Temporal Mamba Block (TMB). We further incorporate a dropout mechanism for selective parameters of TMB to mitigate model overfitting. Moreover, we tackle the issue of variable scan order sensitivity by introducing variable permutation training. We further propose variable-aware scan along time to dynamically discover variable relationships during training and decode the optimal variable scan order by solving the shortest path visiting all nodes problem during inference. Extensive experiments conducted on eight public datasets demonstrate that MambaTS achieves new state-of-the-art performance.

Read more5/28/2024