AlphaForge: A Framework to Mine and Dynamically Combine Formulaic Alpha Factors

0

Sign in to get full access

Overview

- This paper presents a framework called "AlphaForge" that combines multiple formulaic alpha factors to dynamically forecast stock market trends.

- The key idea is to leverage a deep neural network to automatically mine and integrate various alpha factors, which are quantitative signals that can predict future stock returns.

- By dynamically combining these alpha factors, the framework aims to improve the accuracy and robustness of stock trend forecasting compared to using individual factors alone.

Plain English Explanation

Stock market investing is a complex endeavor, and investors often rely on various quantitative signals, known as "alpha factors," to try to predict future stock prices and trends. These alpha factors can be based on things like a company's financial metrics, market sentiment, or technical trading patterns.

The researchers behind this paper recognized that while individual alpha factors can be useful, combining multiple factors together can potentially lead to even more accurate forecasts. However, manually selecting and combining these factors is a challenging task.

To address this, the researchers developed a framework called "AlphaForge" that uses a deep neural network to automatically mine and integrate a wide range of alpha factors. The neural network is trained to dynamically discover the most relevant factors and determine how best to combine them to predict future stock market behavior.

By automatically finding and blending multiple alpha factors, AlphaForge aims to improve upon the predictive power of using individual factors alone. This could potentially help investors make more informed decisions and achieve better investment outcomes.

Technical Explanation

The key components of the AlphaForge framework are:

-

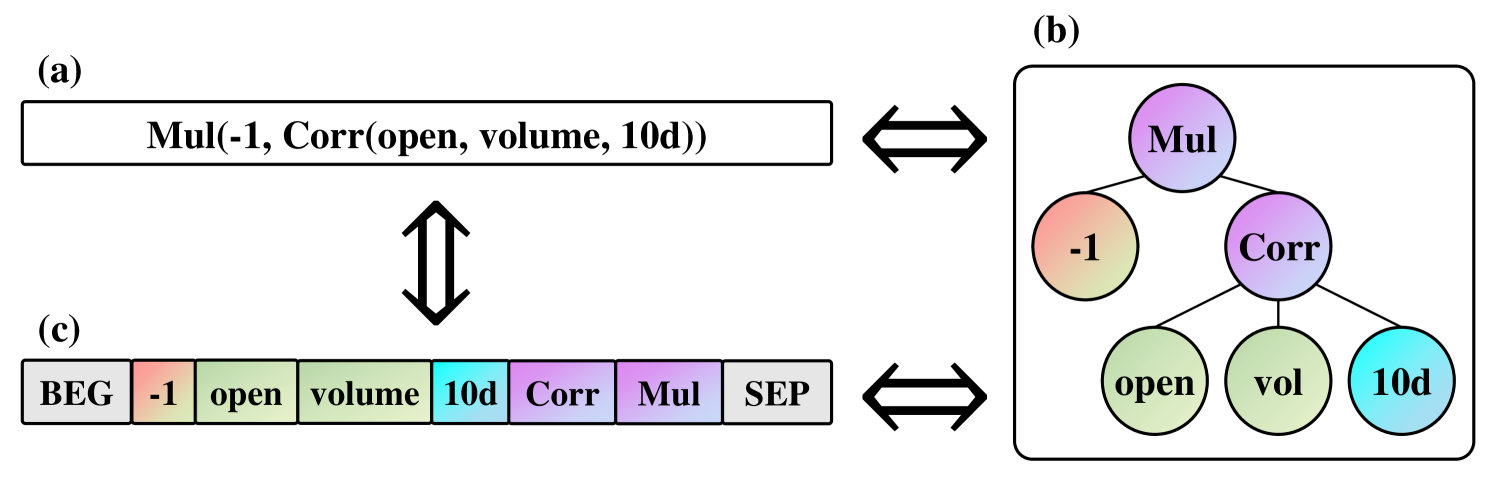

Alpha Factor Mining: The system uses a deep neural network to automatically discover a diverse set of formulaic alpha factors from large-scale market data. This allows the framework to capture a wide range of signals that may be predictive of future stock returns.

-

Dynamic Alpha Factor Combination: AlphaForge then leverages the neural network to dynamically determine how to best combine the mined alpha factors to generate accurate stock trend forecasts. This allows the system to adapt to changing market conditions over time.

-

Ensemble-based Prediction: The framework employs an ensemble-based approach, where multiple neural network models are trained and their individual predictions are combined to improve the overall forecasting accuracy and robustness.

The researchers evaluate AlphaForge on real-world stock market data and demonstrate that it can outperform approaches that rely on individual alpha factors or static combinations. This suggests that the automatic mining and dynamic integration of multiple alpha factors can be a powerful technique for stock trend forecasting.

Critical Analysis

The paper provides a comprehensive technical description of the AlphaForge framework and presents strong empirical results to support its effectiveness. However, a few potential limitations and areas for further research are worth noting:

-

Interpretability: While the automatic alpha factor mining and combination capabilities of AlphaForge are powerful, the black-box nature of the deep neural network models may make it difficult to understand the specific factors and their relative importance. Enhancing the interpretability of the system could be valuable for investors seeking more transparency.

-

Robustness to Market Conditions: The paper's evaluation focuses on overall performance, but it would be useful to understand how AlphaForge behaves under different market conditions, such as periods of high volatility or market crashes. Assessing its robustness in these scenarios could provide additional insights.

-

Computational Complexity: The training and deployment of the deep neural network models in AlphaForge may require significant computational resources, which could be a practical consideration for some investors or portfolio managers. Exploring ways to improve the system's efficiency could broaden its applicability.

Despite these potential areas for improvement, the AlphaForge framework represents an innovative approach to leveraging the power of deep learning and ensemble methods for stock trend forecasting. The ability to automatically discover and dynamically combine multiple alpha factors is a promising direction for the field of quantitative finance.

Conclusion

The AlphaForge framework introduced in this paper offers a compelling solution for improving stock trend forecasting by automatically mining and dynamically combining a diverse set of formulaic alpha factors. By harnessing the power of deep neural networks, the system can adapt to changing market conditions and potentially outperform approaches that rely on individual factors or static combinations.

While the technical complexity of AlphaForge may present some practical challenges, the paper's findings suggest that the automatic discovery and integration of multiple alpha factors could be a valuable tool for investors and portfolio managers seeking to enhance their decision-making and investment strategies. Further research and refinement of the framework may lead to even more robust and accessible solutions for the quantitative finance community.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

AlphaForge: A Framework to Mine and Dynamically Combine Formulaic Alpha Factors

Hao Shi, Weili Song, Xinting Zhang, Jiahe Shi, Cuicui Luo, Xiang Ao, Hamid Arian, Luis Seco

The complexity of financial data, characterized by its variability and low signal-to-noise ratio, necessitates advanced methods in quantitative investment that prioritize both performance and interpretability.Transitioning from early manual extraction to genetic programming, the most advanced approach in the alpha factor mining domain currently employs reinforcement learning to mine a set of combination factors with fixed weights. However, the performance of resultant alpha factors exhibits inconsistency, and the inflexibility of fixed factor weights proves insufficient in adapting to the dynamic nature of financial markets. To address this issue, this paper proposes a two-stage formulaic alpha generating framework AlphaForge, for alpha factor mining and factor combination. This framework employs a generative-predictive neural network to generate factors, leveraging the robust spatial exploration capabilities inherent in deep learning while concurrently preserving diversity. The combination model within the framework incorporates the temporal performance of factors for selection and dynamically adjusts the weights assigned to each component alpha factor. Experiments conducted on real-world datasets demonstrate that our proposed model outperforms contemporary benchmarks in formulaic alpha factor mining. Furthermore, our model exhibits a notable enhancement in portfolio returns within the realm of quantitative investment and real money investment.

Read more8/29/2024

0

Synergistic Formulaic Alpha Generation for Quantitative Trading based on Reinforcement Learning

Hong-Gi Shin, Sukhyun Jeong, Eui-Yeon Kim, Sungho Hong, Young-Jin Cho, Yong-Hoon Choi

Mining of formulaic alpha factors refers to the process of discovering and developing specific factors or indicators (referred to as alpha factors) for quantitative trading in stock market. To efficiently discover alpha factors in vast search space, reinforcement learning (RL) is commonly employed. This paper proposes a method to enhance existing alpha factor mining approaches by expanding a search space and utilizing pretrained formulaic alpha set as initial seed values to generate synergistic formulaic alpha. We employ information coefficient (IC) and rank information coefficient (Rank IC) as performance evaluation metrics for the model. Using CSI300 market data, we conducted real investment simulations and observed significant performance improvement compared to existing techniques.

Read more7/9/2024

0

QuantFactor REINFORCE: Mining Steady Formulaic Alpha Factors with Variance-bounded REINFORCE

Junjie Zhao, Chengxi Zhang, Min Qin, Peng Yang

The goal of alpha factor mining is to discover indicative signals of investment opportunities from the historical financial market data of assets. Deep learning based alpha factor mining methods have shown to be powerful, which, however, lack of the interpretability, making them unacceptable in the risk-sensitive real markets. Alpha factors in formulaic forms are more interpretable and therefore favored by market participants, while the search space is complex and powerful explorative methods are urged. Recently, a promising framework is proposed for generating formulaic alpha factors using deep reinforcement learning, and quickly gained research focuses from both academia and industries. This paper first argues that the originally employed policy training method, i.e., Proximal Policy Optimization (PPO), faces several important issues in the context of alpha factors mining, making it ineffective to explore the search space of the formula. Herein, a novel reinforcement learning based on the well-known REINFORCE algorithm is proposed. Given that the underlying state transition function adheres to the Dirac distribution, the Markov Decision Process within this framework exhibit minimal environmental variability, making REINFORCE algorithm more appropriate than PPO. A new dedicated baseline is designed to theoretically reduce the commonly suffered high variance of REINFORCE. Moreover, the information ratio is introduced as a reward shaping mechanism to encourage the generation of steady alpha factors that can better adapt to changes in market volatility. Experimental evaluations on various real assets data show that the proposed algorithm can increase the correlation with asset returns by 3.83%, and a stronger ability to obtain excess returns compared to the latest alpha factors mining methods, which meets the theoretical results well.

Read more9/10/2024

0

Automate Strategy Finding with LLM in Quant investment

Zhizhuo Kou, Holam Yu, Jingshu Peng, Lei Chen

Despite significant progress in deep learning for financial trading, existing models often face instability and high uncertainty, hindering their practical application. Leveraging advancements in Large Language Models (LLMs) and multi-agent architectures, we propose a novel framework for quantitative stock investment in portfolio management and alpha mining. Our framework addresses these issues by integrating LLMs to generate diversified alphas and employing a multi-agent approach to dynamically evaluate market conditions. This paper proposes a framework where large language models (LLMs) mine alpha factors from multimodal financial data, ensuring a comprehensive understanding of market dynamics. The first module extracts predictive signals by integrating numerical data, research papers, and visual charts. The second module uses ensemble learning to construct a diverse pool of trading agents with varying risk preferences, enhancing strategy performance through a broader market analysis. In the third module, a dynamic weight-gating mechanism selects and assigns weights to the most relevant agents based on real-time market conditions, enabling the creation of an adaptive and context-aware composite alpha formula. Extensive experiments on the Chinese stock markets demonstrate that this framework significantly outperforms state-of-the-art baselines across multiple financial metrics. The results underscore the efficacy of combining LLM-generated alphas with a multi-agent architecture to achieve superior trading performance and stability. This work highlights the potential of AI-driven approaches in enhancing quantitative investment strategies and sets a new benchmark for integrating advanced machine learning techniques in financial trading can also be applied on diverse markets.

Read more9/11/2024