Synergistic Formulaic Alpha Generation for Quantitative Trading based on Reinforcement Learning

0

Sign in to get full access

Overview

- This research paper proposes a method for generating "alpha" signals - indicators that can predict future stock price movements - using reinforcement learning and a novel approach to combining multiple trading strategies.

- The key ideas are to expand the search space of possible trading strategies, use reinforcement learning to optimize the strategy, and combine multiple strategies in a synergistic way.

- This builds on prior work in areas like AlphaForge, DollarTextAlpha2Dollar, and using reinforcement learning for trading optimization.

Plain English Explanation

The researchers are trying to develop a better way for computers to trade stocks and make money. Current trading algorithms often rely on a single, rigid trading strategy. The researchers wanted to create a system that could explore a much wider range of possible trading strategies, and then use machine learning to figure out the best combination of strategies.

The key ideas are:

-

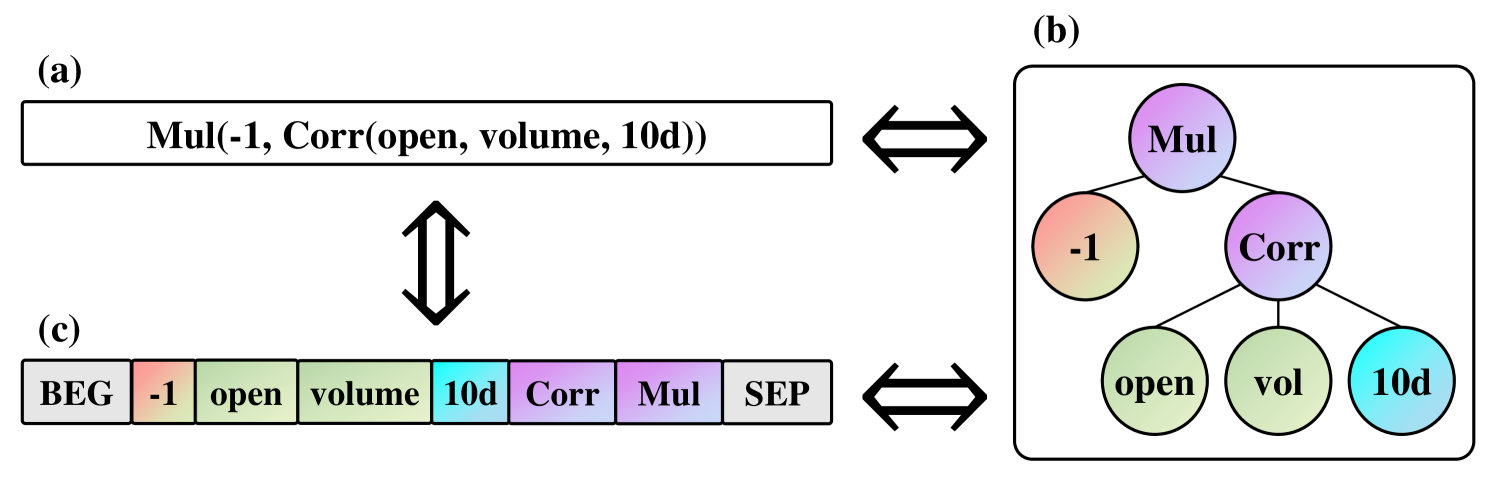

Expand the Search Space: Instead of just using a predefined set of trading rules, the system generates a large number of potential trading "formulas" by combining different indicators, mathematical functions, and other factors. This dramatically increases the space of possible strategies to explore.

-

Optimize with Reinforcement Learning: Once the system has generated these potential trading formulas, it uses reinforcement learning to figure out which combinations work best. Reinforcement learning is a type of machine learning where the system learns by trial-and-error, getting rewarded for successful trades and penalized for unsuccessful ones.

-

Combine Strategies Synergistically: The final step is to take the best-performing individual trading strategies and combine them in a way that amplifies their strengths and compensates for their weaknesses. This "synergistic" combination can produce an overall trading system that outperforms any single strategy.

The researchers believe this approach, building on prior work in areas like AlphaForge, DollarTextAlpha2Dollar, and reinforcement learning for trading, can lead to more robust and profitable trading algorithms.

Technical Explanation

The core of the proposed method is a three-step process:

-

Expanding the Search Space: The system generates a large number of potential trading "formulas" by combining various mathematical functions, indicators, and other factors in a combinatorial fashion. This creates a much broader set of possible trading strategies to explore, going beyond the typical predefined set of rules.

-

Optimizing with Reinforcement Learning: The system then uses reinforcement learning to evaluate the performance of these generated trading formulas. Reinforcement learning is a type of machine learning where the system learns by trial-and-error, getting rewarded for successful trades and penalized for unsuccessful ones. This allows the system to iteratively improve the trading strategies.

-

Synergistic Combination: Finally, the system combines the best-performing individual trading strategies in a way that leverages their strengths and compensates for their weaknesses. This "synergistic" combination can produce an overall trading system that outperforms any single strategy.

The researchers tested their approach on historical stock market data and found that it outperformed traditional trading algorithms as well as other state-of-the-art machine learning approaches. They also showed that the synergistic combination of strategies led to better performance than using any single strategy alone.

Critical Analysis

The researchers acknowledge several limitations and areas for further research:

- The performance of the system may be sensitive to the initial set of trading formulas generated, and more work is needed to ensure robust and generalizable results.

- The synergistic combination of strategies relies on heuristic methods, and more principled approaches to strategy integration may lead to further improvements.

- The computational complexity of the system may be a concern, especially as the search space of possible trading formulas grows, and techniques to improve efficiency may be needed.

Additionally, some potential concerns that were not explicitly addressed in the paper include:

- The risk of overfitting to historical data, and the need for rigorous out-of-sample testing to ensure the system's performance generalizes to future market conditions.

- The interpretability of the final trading system, as the combination of multiple complex strategies may make it difficult to understand the reasoning behind the system's decisions.

- The potential for the system to be gamed or exploited by other market participants, as the trading strategies become more sophisticated and widely adopted.

Overall, the researchers have presented an interesting and promising approach to generating alpha signals for quantitative trading. However, further research and real-world testing will be needed to fully assess the practical viability and long-term implications of this method.

Conclusion

This research paper proposes a novel approach to generating alpha signals for quantitative trading using reinforcement learning and a synergistic combination of multiple trading strategies. By expanding the search space of possible trading formulas and optimizing them using reinforcement learning, the system can discover more robust and profitable trading strategies.

The key innovations of this work build upon prior research in areas like AlphaForge, DollarTextAlpha2Dollar, and reinforcement learning for trading. If successful, this approach could lead to more advanced and profitable automated trading systems that can outperform human traders and traditional algorithms.

However, the researchers acknowledge several limitations and areas for further research, and there are additional potential concerns that warrant careful consideration. Nonetheless, this work represents an exciting step forward in the development of more sophisticated and adaptive trading algorithms.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Synergistic Formulaic Alpha Generation for Quantitative Trading based on Reinforcement Learning

Hong-Gi Shin, Sukhyun Jeong, Eui-Yeon Kim, Sungho Hong, Young-Jin Cho, Yong-Hoon Choi

Mining of formulaic alpha factors refers to the process of discovering and developing specific factors or indicators (referred to as alpha factors) for quantitative trading in stock market. To efficiently discover alpha factors in vast search space, reinforcement learning (RL) is commonly employed. This paper proposes a method to enhance existing alpha factor mining approaches by expanding a search space and utilizing pretrained formulaic alpha set as initial seed values to generate synergistic formulaic alpha. We employ information coefficient (IC) and rank information coefficient (Rank IC) as performance evaluation metrics for the model. Using CSI300 market data, we conducted real investment simulations and observed significant performance improvement compared to existing techniques.

Read more7/9/2024

0

QuantFactor REINFORCE: Mining Steady Formulaic Alpha Factors with Variance-bounded REINFORCE

Junjie Zhao, Chengxi Zhang, Min Qin, Peng Yang

The goal of alpha factor mining is to discover indicative signals of investment opportunities from the historical financial market data of assets. Deep learning based alpha factor mining methods have shown to be powerful, which, however, lack of the interpretability, making them unacceptable in the risk-sensitive real markets. Alpha factors in formulaic forms are more interpretable and therefore favored by market participants, while the search space is complex and powerful explorative methods are urged. Recently, a promising framework is proposed for generating formulaic alpha factors using deep reinforcement learning, and quickly gained research focuses from both academia and industries. This paper first argues that the originally employed policy training method, i.e., Proximal Policy Optimization (PPO), faces several important issues in the context of alpha factors mining, making it ineffective to explore the search space of the formula. Herein, a novel reinforcement learning based on the well-known REINFORCE algorithm is proposed. Given that the underlying state transition function adheres to the Dirac distribution, the Markov Decision Process within this framework exhibit minimal environmental variability, making REINFORCE algorithm more appropriate than PPO. A new dedicated baseline is designed to theoretically reduce the commonly suffered high variance of REINFORCE. Moreover, the information ratio is introduced as a reward shaping mechanism to encourage the generation of steady alpha factors that can better adapt to changes in market volatility. Experimental evaluations on various real assets data show that the proposed algorithm can increase the correlation with asset returns by 3.83%, and a stronger ability to obtain excess returns compared to the latest alpha factors mining methods, which meets the theoretical results well.

Read more9/10/2024

0

AlphaForge: A Framework to Mine and Dynamically Combine Formulaic Alpha Factors

Hao Shi, Weili Song, Xinting Zhang, Jiahe Shi, Cuicui Luo, Xiang Ao, Hamid Arian, Luis Seco

The complexity of financial data, characterized by its variability and low signal-to-noise ratio, necessitates advanced methods in quantitative investment that prioritize both performance and interpretability.Transitioning from early manual extraction to genetic programming, the most advanced approach in the alpha factor mining domain currently employs reinforcement learning to mine a set of combination factors with fixed weights. However, the performance of resultant alpha factors exhibits inconsistency, and the inflexibility of fixed factor weights proves insufficient in adapting to the dynamic nature of financial markets. To address this issue, this paper proposes a two-stage formulaic alpha generating framework AlphaForge, for alpha factor mining and factor combination. This framework employs a generative-predictive neural network to generate factors, leveraging the robust spatial exploration capabilities inherent in deep learning while concurrently preserving diversity. The combination model within the framework incorporates the temporal performance of factors for selection and dynamically adjusts the weights assigned to each component alpha factor. Experiments conducted on real-world datasets demonstrate that our proposed model outperforms contemporary benchmarks in formulaic alpha factor mining. Furthermore, our model exhibits a notable enhancement in portfolio returns within the realm of quantitative investment and real money investment.

Read more8/29/2024

0

$text{Alpha}^2$: Discovering Logical Formulaic Alphas using Deep Reinforcement Learning

Feng Xu, Yan Yin, Xinyu Zhang, Tianyuan Liu, Shengyi Jiang, Zongzhang Zhang

Alphas are pivotal in providing signals for quantitative trading. The industry highly values the discovery of formulaic alphas for their interpretability and ease of analysis, compared with the expressive yet overfitting-prone black-box alphas. In this work, we focus on discovering formulaic alphas. Prior studies on automatically generating a collection of formulaic alphas were mostly based on genetic programming (GP), which is known to suffer from the problems of being sensitive to the initial population, converting to local optima, and slow computation speed. Recent efforts employing deep reinforcement learning (DRL) for alpha discovery have not fully addressed key practical considerations such as alpha correlations and validity, which are crucial for their effectiveness. In this work, we propose a novel framework for alpha discovery using DRL by formulating the alpha discovery process as program construction. Our agent, $text{Alpha}^2$, assembles an alpha program optimized for an evaluation metric. A search algorithm guided by DRL navigates through the search space based on value estimates for potential alpha outcomes. The evaluation metric encourages both the performance and the diversity of alphas for a better final trading strategy. Our formulation of searching alphas also brings the advantage of pre-calculation dimensional analysis, ensuring the logical soundness of alphas, and pruning the vast search space to a large extent. Empirical experiments on real-world stock markets demonstrates $text{Alpha}^2$'s capability to identify a diverse set of logical and effective alphas, which significantly improves the performance of the final trading strategy. The code of our method is available at https://github.com/x35f/alpha2.

Read more6/27/2024