Developing A Multi-Agent and Self-Adaptive Framework with Deep Reinforcement Learning for Dynamic Portfolio Risk Management

0

🤿

Sign in to get full access

Overview

- Researchers have explored using deep learning and reinforcement learning (RL) approaches as reactive agents to quickly adapt investment strategies for portfolio management in volatile financial markets.

- However, these agents can be biased towards maximizing returns while neglecting potential risks under changing market conditions.

- The researchers propose a multi-agent and self-adaptive (MASA) framework that uses a multi-agent RL approach to balance the tradeoff between portfolio returns and risks.

- The MASA framework also incorporates a proactive "market observer" agent to provide additional insights on market trends to help the RL agents adapt.

Plain English Explanation

The research paper discusses a new way to manage investment portfolios in turbulent financial markets. Deep learning and reinforcement learning techniques have been used to quickly adapt investment strategies in fast-moving markets. However, these approaches can become biased, focusing too much on maximizing returns while overlooking the potential risks.

To address this, the researchers developed a multi-agent system called MASA that uses multiple reinforcement learning agents working together. These agents cooperate to carefully balance the tradeoff between high returns and managing risk, based on the current market conditions.

The MASA framework also includes a special "market observer" agent that provides additional insights on market trends. This helps the reinforcement learning agents quickly adapt their strategies as the financial landscape changes. The researchers tested MASA on historical data from major stock indexes and found it outperformed other RL-based approaches.

Overall, the MASA framework demonstrates how a multi-agent, self-adaptive approach can be more effective than individual reinforcement learning agents for portfolio management in volatile markets. By incorporating diverse perspectives and a proactive monitoring component, MASA is better able to navigate the complexities of real-world finance.

Technical Explanation

The researchers propose a multi-agent and self-adaptive (MASA) framework that utilizes a sophisticated multi-agent reinforcement learning (RL) approach to dynamically balance the tradeoff between portfolio returns and risks in turbulent financial markets.

The MASA framework consists of two key components:

-

Cooperating and Reactive Agents: These are the main RL-based agents responsible for formulating and adapting the investment portfolio. They work together to optimize for both high returns and managed risk.

-

Proactive Market Observer Agent: This agent provides additional insights on estimated market trends to help the RL agents quickly adapt their strategies to changing conditions.

The researchers evaluated the MASA framework against other well-known RL-based approaches using historical data from major stock indexes like the CSI 300, Dow Jones Industrial Average, and S&P 500 over the past 10 years. The results demonstrate the potential strengths of the multi-agent RL approach in the MASA framework compared to individual RL agents.

Critical Analysis

The researchers acknowledge that in many cases, individual deep learning or RL agents can become biased towards maximizing returns while neglecting potential risks in volatile financial markets. This is an important limitation that the MASA framework aims to address.

One potential area for further research is exploring how the MASA framework could be extended to incorporate other types of agents or information sources beyond just the market observer. For example, agents that specialize in risk modeling or macroeconomic analysis could provide additional valuable inputs.

Additionally, while the MASA framework shows promising results, the researchers note that more work is needed to fully understand its behavior and limitations, especially when faced with highly complex or rapidly changing market conditions. Rigorous testing and validation across a broader range of scenarios would help establish the robustness and generalizability of the approach.

Conclusion

The MASA framework presented in this research paper demonstrates how a multi-agent, self-adaptive approach can be more effective than individual reinforcement learning agents for portfolio management in volatile financial markets. By incorporating cooperative RL agents and a proactive market observer, the framework is able to better balance the tradeoff between maximizing returns and controlling risks.

The results suggest that this type of multi-agent system could be a valuable tool for investment managers and financial institutions looking to navigate the complexities of modern markets. The insights from this research also point to promising directions for future work in applying multi-agent systems to other challenging real-world problems.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

🤿

0

Developing A Multi-Agent and Self-Adaptive Framework with Deep Reinforcement Learning for Dynamic Portfolio Risk Management

Zhenglong Li, Vincent Tam, Kwan L. Yeung

Deep or reinforcement learning (RL) approaches have been adapted as reactive agents to quickly learn and respond with new investment strategies for portfolio management under the highly turbulent financial market environments in recent years. In many cases, due to the very complex correlations among various financial sectors, and the fluctuating trends in different financial markets, a deep or reinforcement learning based agent can be biased in maximising the total returns of the newly formulated investment portfolio while neglecting its potential risks under the turmoil of various market conditions in the global or regional sectors. Accordingly, a multi-agent and self-adaptive framework namely the MASA is proposed in which a sophisticated multi-agent reinforcement learning (RL) approach is adopted through two cooperating and reactive agents to carefully and dynamically balance the trade-off between the overall portfolio returns and their potential risks. Besides, a very flexible and proactive agent as the market observer is integrated into the MASA framework to provide some additional information on the estimated market trends as valuable feedbacks for multi-agent RL approach to quickly adapt to the ever-changing market conditions. The obtained empirical results clearly reveal the potential strengths of our proposed MASA framework based on the multi-agent RL approach against many well-known RL-based approaches on the challenging data sets of the CSI 300, Dow Jones Industrial Average and S&P 500 indexes over the past 10 years. More importantly, our proposed MASA framework shed lights on many possible directions for future investigation.

Read more9/11/2024

0

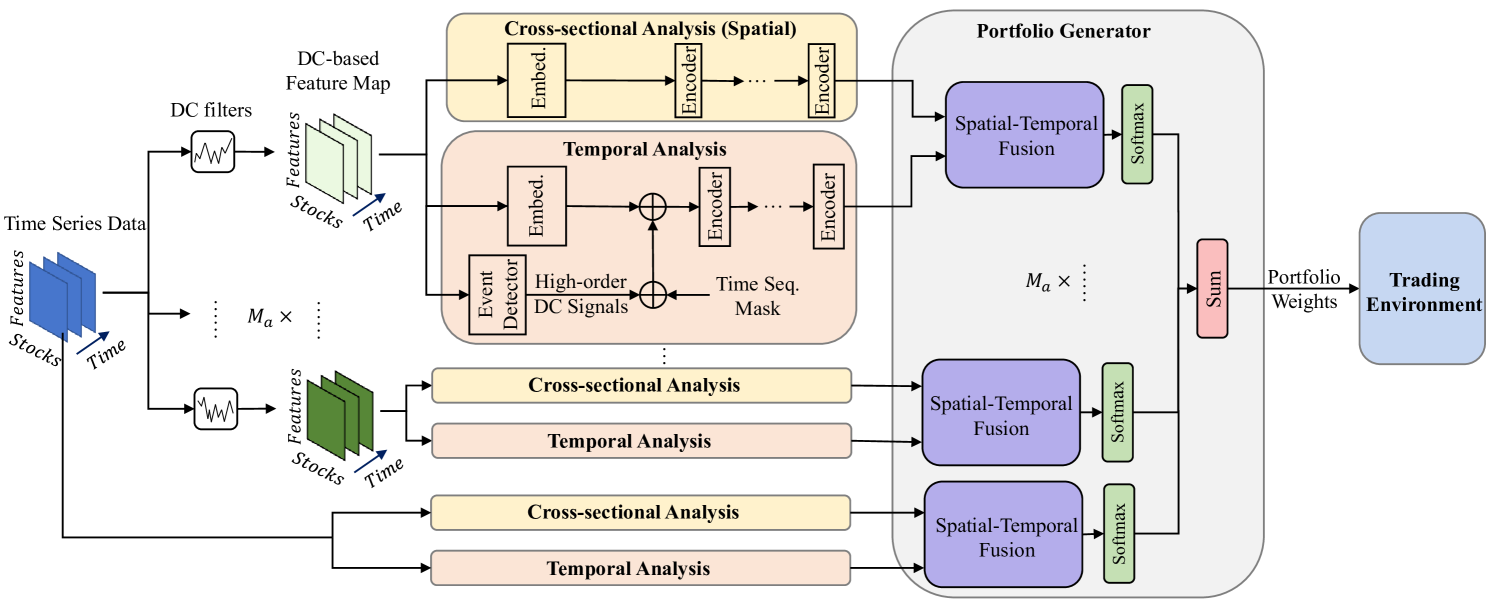

Developing An Attention-Based Ensemble Learning Framework for Financial Portfolio Optimisation

Zhenglong Li, Vincent Tam

In recent years, deep or reinforcement learning approaches have been applied to optimise investment portfolios through learning the spatial and temporal information under the dynamic financial market. Yet in most cases, the existing approaches may produce biased trading signals based on the conventional price data due to a lot of market noises, which possibly fails to balance the investment returns and risks. Accordingly, a multi-agent and self-adaptive portfolio optimisation framework integrated with attention mechanisms and time series, namely the MASAAT, is proposed in this work in which multiple trading agents are created to observe and analyse the price series and directional change data that recognises the significant changes of asset prices at different levels of granularity for enhancing the signal-to-noise ratio of price series. Afterwards, by reconstructing the tokens of financial data in a sequence, the attention-based cross-sectional analysis module and temporal analysis module of each agent can effectively capture the correlations between assets and the dependencies between time points. Besides, a portfolio generator is integrated into the proposed framework to fuse the spatial-temporal information and then summarise the portfolios suggested by all trading agents to produce a newly ensemble portfolio for reducing biased trading actions and balancing the overall returns and risks. The experimental results clearly demonstrate that the MASAAT framework achieves impressive enhancement when compared with many well-known portfolio optimsation approaches on three challenging data sets of DJIA, S&P 500 and CSI 300. More importantly, our proposal has potential strengths in many possible applications for future study.

Read more4/16/2024

0

New!A Deep Reinforcement Learning Framework For Financial Portfolio Management

Jinyang Li

In this research paper, we investigate into a paper named A Deep Reinforcement Learning Framework for the Financial Portfolio Management Problem [arXiv:1706.10059]. It is a portfolio management problem which is solved by deep learning techniques. The original paper proposes a financial-model-free reinforcement learning framework, which consists of the Ensemble of Identical Independent Evaluators (EIIE) topology, a Portfolio-Vector Memory (PVM), an Online Stochastic Batch Learning (OSBL) scheme, and a fully exploiting and explicit reward function. Three different instants are used to realize this framework, namely a Convolutional Neural Network (CNN), a basic Recurrent Neural Network (RNN), and a Long Short-Term Memory (LSTM). The performance is then examined by comparing to a number of recently reviewed or published portfolio-selection strategies. We have successfully replicated their implementations and evaluations. Besides, we further apply this framework in the stock market, instead of the cryptocurrency market that the original paper uses. The experiment in the cryptocurrency market is consistent with the original paper, which achieve superior returns. But it doesn't perform as well when applied in the stock market.

Read more9/16/2024

0

Portfolio Management using Deep Reinforcement Learning

Ashish Anil Pawar, Vishnureddy Prashant Muskawar, Ritesh Tiku

Algorithmic trading or Financial robots have been conquering the stock markets with their ability to fathom complex statistical trading strategies. But with the recent development of deep learning technologies, these strategies are becoming impotent. The DQN and A2C models have previously outperformed eminent humans in game-playing and robotics. In our work, we propose a reinforced portfolio manager offering assistance in the allocation of weights to assets. The environment proffers the manager the freedom to go long and even short on the assets. The weight allocation advisements are restricted to the choice of portfolio assets and tested empirically to knock benchmark indices. The manager performs financial transactions in a postulated liquid market without any transaction charges. This work provides the conclusion that the proposed portfolio manager with actions centered on weight allocations can surpass the risk-adjusted returns of conventional portfolio managers.

Read more5/6/2024