DLFormer: Enhancing Explainability in Multivariate Time Series Forecasting using Distributed Lag Embedding

0

🔄

Sign in to get full access

Overview

- Real-world variables are often influenced by past values and other factors, making them multivariate time series data.

- Predicting these time series using artificial intelligence is an ongoing challenge.

- In fields like healthcare and finance, where reliability is crucial, having understandable explanations for predictions is essential.

- Balancing high prediction accuracy and intuitive explainability has proven difficult.

- Attention-based models have limitations in representing individual variable influences, but can capture temporal dependencies and magnitudes.

Plain English Explanation

The paper introduces DLFormer, an attention-based architecture that integrates distributed lag embedding to temporally embed individual variables and capture their temporal influence. This addresses the challenge of achieving both high prediction accuracy and intuitive explainability when working with complex, multivariate time series data.

Real-world data, such as in healthcare or finance, often consists of multiple variables that are influenced by their past values and other factors. Predicting the future values of these variables using AI is an important but difficult problem. Crucially, in sensitive domains, it's not enough to just make accurate predictions - the reasoning behind those predictions must also be clear and understandable.

Existing attention-based models can capture the temporal dependencies in time series data and the relative importance of individual variables. However, they struggle to fully represent how each variable independently influences the overall prediction. DLFormer aims to address this by explicitly embedding the temporal relationships of individual variables, enhancing both the model's performance and its ability to explain its decisions.

Through testing on real-world datasets, the authors show that DLFormer outperforms other high-performing attention-based models. Importantly, the improved explainability also helps strengthen the reliability of the predictions.

Technical Explanation

The DLFormer architecture combines attention mechanisms with distributed lag embedding, a technique that learns to temporally embed the individual influence of each input variable. This allows the model to capture both the temporal dependencies in the time series data and the specific impact of each variable over time.

The core components of DLFormer include:

- Distributed Lag Embedding: This module learns a set of learnable lag weights for each input variable, which are then used to construct a temporally-embedded representation of that variable.

- Attention Mechanism: The attention layer is used to model the interdependencies between the temporally-embedded variable representations, capturing the complex dynamics in the time series data.

- Prediction Head: The final prediction is made by feeding the attention-based representations through a feedforward network.

The authors evaluate DLFormer on several real-world multivariate time series datasets, comparing its performance to state-of-the-art attention-based models. The results show that DLFormer achieves superior predictive accuracy while also providing more intuitive explanations of the individual variable influences.

Critical Analysis

The paper makes a compelling case for the importance of balancing predictive performance and model explainability, particularly in high-stakes domains. The authors' approach of integrating distributed lag embedding with attention mechanisms is a novel and promising solution to this challenge.

One potential limitation of the study is the reliance on a relatively small number of real-world datasets for evaluation. While the authors demonstrate consistent performance improvements, it would be valuable to see the model tested on a wider range of multivariate time series problems to further validate its effectiveness.

Additionally, the paper does not delve deeply into the specific interpretability and explainability benefits of the DLFormer architecture. A more thorough analysis of how the model's explanations compare to other approaches, and how users might leverage these explanations in practice, could strengthen the overall contribution.

Despite these minor caveats, the DLFormer model represents a meaningful advance in the field of explainable AI for multivariate time series prediction. Further research and real-world deployment of this approach could have significant implications for decision-making in critical domains.

Conclusion

This paper introduces DLFormer, an attention-based architecture that integrates distributed lag embedding to enhance both the predictive performance and explainability of multivariate time series models. By explicitly capturing the temporal influence of individual variables, DLFormer achieves superior results compared to other high-performing attention-based models, while also providing more intuitive explanations of its predictions.

The ability to balance accuracy and interpretability is crucial in domains like healthcare and finance, where reliable and transparent decision-making is paramount. The DLFormer approach represents an important step forward in addressing this challenge and could have far-reaching implications for the practical application of AI in sensitive real-world settings.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

🔄

0

DLFormer: Enhancing Explainability in Multivariate Time Series Forecasting using Distributed Lag Embedding

Younghwi Kim, Dohee Kim, Sunghyun Sim

. Most real-world variables are multivariate time series influenced by past values and explanatory factors. Consequently, predicting these time series data using artificial intelligence is ongoing. In particular, in fields such as healthcare and finance, where reliability is crucial, having understandable explanations for predictions is essential. However, achieving a balance between high prediction accuracy and intuitive explainability has proven challenging. Although attention-based models have limitations in representing the individual influences of each variable, these models can influence the temporal dependencies in time series prediction and the magnitude of the influence of individual variables. To address this issue, this study introduced DLFormer, an attention-based architecture integrated with distributed lag embedding, to temporally embed individual variables and capture their temporal influence. Through validation against various real-world datasets, DLFormer showcased superior performance improvements compared to existing attention-based high-performance models. Furthermore, comparing the relationships between variables enhanced the reliability of explainability.

Read more9/2/2024

0

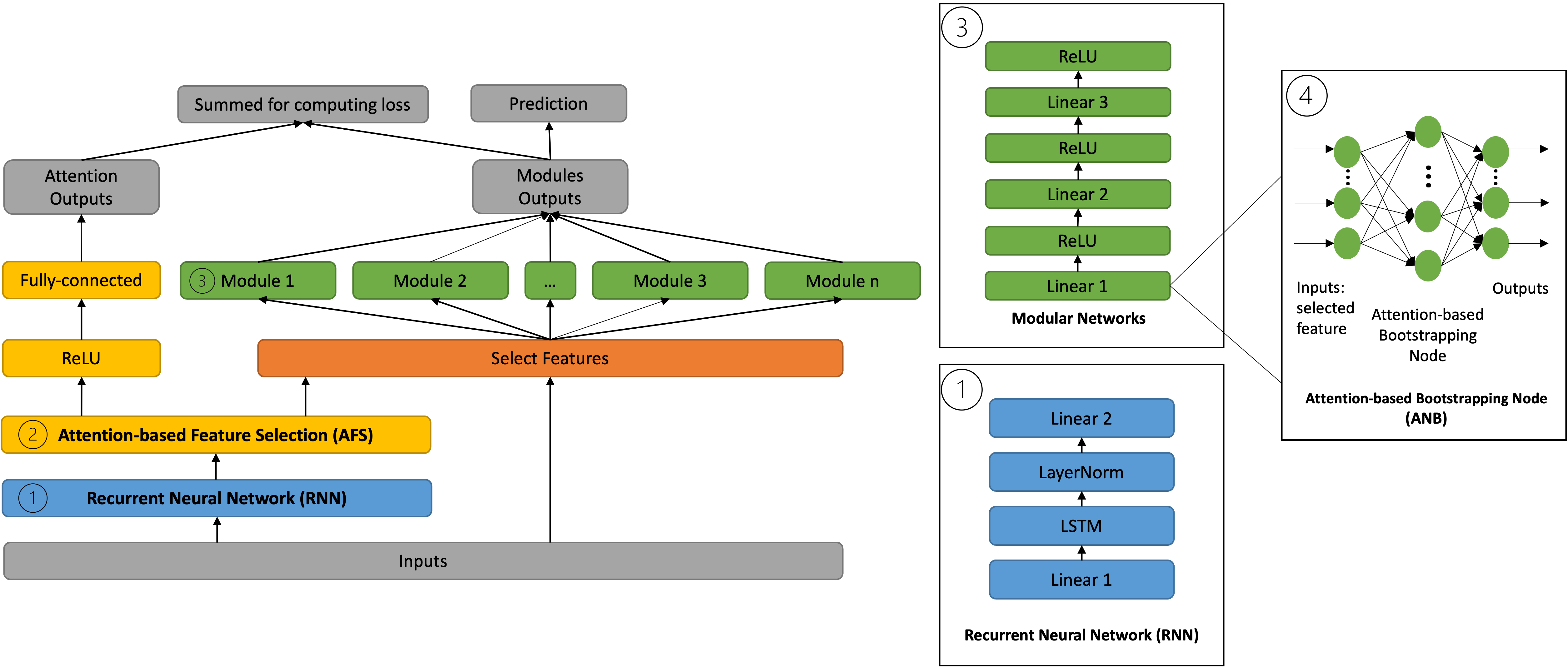

FocusLearn: Fully-Interpretable, High-Performance Modular Neural Networks for Time Series

Qiqi Su, Christos Kloukinas, Artur d'Avila Garcez

Multivariate time series have many applications, from healthcare and meteorology to life science. Although deep learning models have shown excellent predictive performance for time series, they have been criticised for being black-boxes or non-interpretable. This paper proposes a novel modular neural network model for multivariate time series prediction that is interpretable by construction. A recurrent neural network learns the temporal dependencies in the data while an attention-based feature selection component selects the most relevant features and suppresses redundant features used in the learning of the temporal dependencies. A modular deep network is trained from the selected features independently to show the users how features influence outcomes, making the model interpretable. Experimental results show that this approach can outperform state-of-the-art interpretable Neural Additive Models (NAM) and variations thereof in both regression and classification of time series tasks, achieving a predictive performance that is comparable to the top non-interpretable methods for time series, LSTM and XGBoost.

Read more5/6/2024

🤿

0

DGCformer: Deep Graph Clustering Transformer for Multivariate Time Series Forecasting

Qinshuo Liu, Yanwen Fang, Pengtao Jiang, Guodong Li

Multivariate time series forecasting tasks are usually conducted in a channel-dependent (CD) way since it can incorporate more variable-relevant information. However, it may also involve a lot of irrelevant variables, and this even leads to worse performance than the channel-independent (CI) strategy. This paper combines the strengths of both strategies and proposes the Deep Graph Clustering Transformer (DGCformer) for multivariate time series forecasting. Specifically, it first groups these relevant variables by a graph convolutional network integrated with an autoencoder, and a former-latter masked self-attention mechanism is then considered with the CD strategy being applied to each group of variables while the CI one for different groups. Extensive experimental results on eight datasets demonstrate the superiority of our method against state-of-the-art models, and our code will be publicly available upon acceptance.

Read more5/15/2024

0

Multi-variable Adversarial Time-Series Forecast Model

Xiaoqiao Chen

Short-term industrial enterprises power system forecasting is an important issue for both load control and machine protection. Scientists focus on load forecasting but ignore other valuable electric-meters which should provide guidance of power system protection. We propose a new framework, multi-variable adversarial time-series forecasting model, which regularizes Long Short-term Memory (LSTM) models via an adversarial process. The novel model forecasts all variables (may in different type, such as continue variables, category variables, etc.) in power system at the same time and helps trade-off process between forecasting accuracy of single variable and variable-variable relations. Experiments demonstrate the potential of the framework through qualitative and quantitative evaluation of the generated samples. The predict results of electricity consumption of industrial enterprises by multi-variable adversarial time-series forecasting model show that the proposed approach is able to achieve better prediction accuracy. We also applied this model to real industrial enterprises power system data we gathered from several large industrial enterprises via advanced power monitors, and got impressed forecasting results.

Read more6/4/2024