Ensembling Portfolio Strategies for Long-Term Investments: A Distribution-Free Preference Framework for Decision-Making and Algorithms

0

Sign in to get full access

Overview

- This paper proposes a distribution-free preference framework for decision-making and algorithms in the context of long-term investment portfolio management.

- The authors introduce an ensemble approach that combines multiple portfolio strategies to improve long-term investment performance.

- The framework aims to make investment decisions without relying on specific assumptions about the underlying probability distributions of asset returns.

Plain English Explanation

When it comes to long-term investing, making the right decisions can be challenging. Traditional investment strategies often rely on assumptions about the future behavior of financial markets, which can be difficult to predict accurately. This research paper presents a novel approach that tries to overcome this limitation.

The key idea is to use an "ensemble" of different portfolio strategies, rather than relying on a single strategy. Just like an ensemble of machine learning models can often outperform a single model, the authors suggest that combining multiple investment strategies can lead to better long-term investment performance. This approach is designed to be "distribution-free," meaning it doesn't require making specific assumptions about the probability distributions of asset returns.

By using a diverse set of investment strategies and combining their strengths, the proposed framework aims to make more robust and informed decisions, even in the face of uncertainty and unpredictable market conditions. This can be particularly valuable for investors with long-term investment horizons, who need to navigate various economic and market cycles over time.

Technical Explanation

The paper introduces a distribution-free preference framework for decision-making and algorithms in the context of long-term investment portfolio management. The authors propose an ensemble approach that combines multiple portfolio strategies to improve long-term investment performance.

The framework is designed to make investment decisions without relying on specific assumptions about the underlying probability distributions of asset returns. This is an important feature, as traditional investment strategies often rely on such assumptions, which can be difficult to verify in practice.

The authors formalize the problem of portfolio selection as a multi-objective optimization task, where the goal is to find a set of portfolio weights that simultaneously optimize various investment objectives, such as expected return, risk, and drawdown. They introduce a novel preference framework that allows for a flexible and holistic evaluation of investment strategies, without requiring the specification of a single utility function.

The ensemble approach involves combining the outputs of multiple portfolio strategies, each with its own unique characteristics and perspectives. The authors explore various ensemble methods, such as weighted averaging and rank-based aggregation, to integrate the insights from the individual strategies.

The proposed framework is evaluated using both synthetic and real-world financial data, with the authors demonstrating its ability to outperform traditional portfolio optimization methods in terms of long-term investment performance and robustness to market conditions. The results suggest that the ensemble approach can effectively capture the complementary strengths of different investment strategies, leading to more reliable and adaptive decision-making in the context of long-term investments.

Critical Analysis

The research presented in this paper addresses an important challenge in long-term investment management, namely the need for decision-making frameworks that can handle uncertainty and avoid reliance on restrictive assumptions about asset return distributions.

One of the key strengths of the proposed approach is its distribution-free nature, which allows it to be more broadly applicable than traditional portfolio optimization methods. By combining multiple investment strategies, the ensemble approach can potentially capture a wider range of market dynamics and investment objectives, potentially leading to more robust and adaptable decision-making.

However, the paper does not delve deeply into the specific ensemble methods used or the criteria for selecting the individual portfolio strategies that make up the ensemble. More detailed discussion of these design choices and their impact on the overall performance of the framework would be valuable for readers interested in implementing or extending this research.

Additionally, the authors do not extensively explore the potential limitations or drawbacks of the ensemble approach. For example, the computational complexity of the framework and the challenges of interpreting and explaining the ensemble's decision-making process could be important considerations for real-world applications.

Further research could also investigate the performance of the ensemble approach under more diverse market conditions, including periods of extreme volatility or structural shifts in financial markets. Evaluating the robustness and generalizability of the framework would be crucial for assessing its practical utility.

Conclusion

This paper presents a novel distribution-free preference framework for decision-making and algorithms in the context of long-term investment portfolio management. By employing an ensemble approach that combines multiple portfolio strategies, the authors aim to improve the robustness and adaptability of investment decisions, even in the face of uncertainty and unpredictable market conditions.

The key contribution of this research is the development of a flexible and holistic decision-making framework that does not rely on restrictive assumptions about asset return distributions. This approach has the potential to be more broadly applicable than traditional portfolio optimization methods, making it a valuable tool for long-term investors seeking to navigate the complexities of financial markets.

While the paper demonstrates promising results, further research is needed to address potential limitations and explore the framework's performance under a wider range of market conditions. Nonetheless, this work represents an important step towards developing more sophisticated and adaptive investment decision-making systems, with potential implications for the field of portfolio management using deep reinforcement learning and model ensembling for constrained optimization.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Ensembling Portfolio Strategies for Long-Term Investments: A Distribution-Free Preference Framework for Decision-Making and Algorithms

Duy Khanh Lam

This paper investigates the problem of ensembling multiple strategies for sequential portfolios to outperform individual strategies in terms of long-term wealth. Due to the uncertainty of strategies' performances in the future market, which are often based on specific models and statistical assumptions, investors often mitigate risk and enhance robustness by combining multiple strategies, akin to common approaches in collective learning prediction. However, the absence of a distribution-free and consistent preference framework complicates decisions of combination due to the ambiguous objective. To address this gap, we introduce a novel framework for decision-making in combining strategies, irrespective of market conditions, by establishing the investor's preference between decisions and then forming a clear objective. Through this framework, we propose a combinatorial strategy construction, free from statistical assumptions, for any scale of component strategies, even infinite, such that it meets the determined criterion. Finally, we test the proposed strategy along with its accelerated variant and some other multi-strategies. The numerical experiments show results in favor of the proposed strategies, albeit with small tradeoffs in their Sharpe ratios, in which their cumulative wealths eventually exceed those of the best component strategies while the accelerated strategy significantly improves performance.

Read more6/7/2024

🖼️

0

Mean-Variance Portfolio Selection in Long-Term Investments with Unknown Distribution: Online Estimation, Risk Aversion under Ambiguity, and Universality of Algorithms

Duy Khanh Lam

The standard approach for constructing a Mean-Variance portfolio involves estimating parameters for the model using collected samples. However, since the distribution of future data may not resemble that of the training set, the out-of-sample performance of the estimated portfolio is worse than one derived with true parameters, which has prompted several innovations for better estimation. Instead of treating the data without a timing aspect as in the common training-backtest approach, this paper adopts a perspective where data gradually and continuously reveal over time. The original model is recast into an online learning framework, which is free from any statistical assumptions, to propose a dynamic strategy of sequential portfolios such that its empirical utility, Sharpe ratio, and growth rate asymptotically achieve those of the true portfolio, derived with perfect knowledge of the future data. When the distribution of future data has a normal shape, the growth rate of wealth is shown to increase by lifting the portfolio along the efficient frontier through the calibration of risk aversion. Since risk aversion cannot be appropriately predetermined, another proposed algorithm updating this coefficient over time forms a dynamic strategy approaching the optimal empirical Sharpe ratio or growth rate associated with the true coefficient. The performance of these proposed strategies is universally guaranteed under specific stochastic markets. Furthermore, in stationary and ergodic markets, the so-called Bayesian strategy utilizing true conditional distributions, based on observed past market information during investment, almost surely does not perform better than the proposed strategies in terms of empirical utility, Sharpe ratio, or growth rate, which, in contrast, do not rely on conditional distributions.

Read more6/21/2024

0

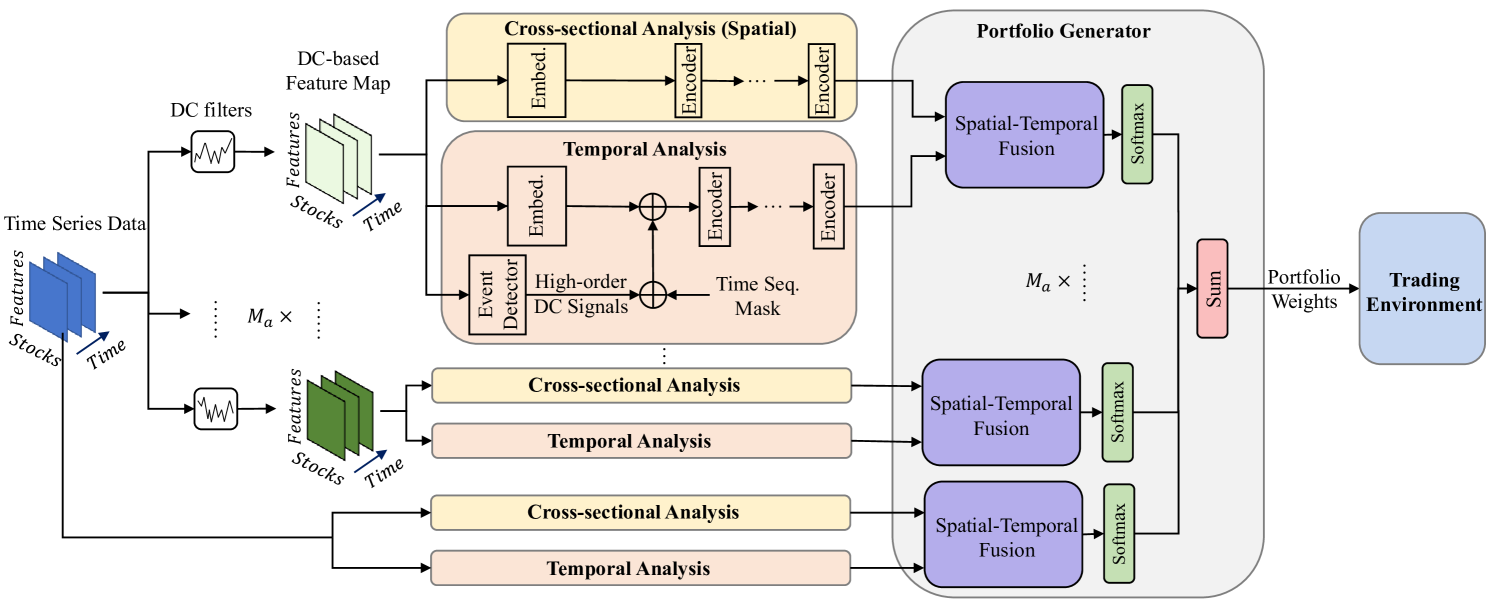

Developing An Attention-Based Ensemble Learning Framework for Financial Portfolio Optimisation

Zhenglong Li, Vincent Tam

In recent years, deep or reinforcement learning approaches have been applied to optimise investment portfolios through learning the spatial and temporal information under the dynamic financial market. Yet in most cases, the existing approaches may produce biased trading signals based on the conventional price data due to a lot of market noises, which possibly fails to balance the investment returns and risks. Accordingly, a multi-agent and self-adaptive portfolio optimisation framework integrated with attention mechanisms and time series, namely the MASAAT, is proposed in this work in which multiple trading agents are created to observe and analyse the price series and directional change data that recognises the significant changes of asset prices at different levels of granularity for enhancing the signal-to-noise ratio of price series. Afterwards, by reconstructing the tokens of financial data in a sequence, the attention-based cross-sectional analysis module and temporal analysis module of each agent can effectively capture the correlations between assets and the dependencies between time points. Besides, a portfolio generator is integrated into the proposed framework to fuse the spatial-temporal information and then summarise the portfolios suggested by all trading agents to produce a newly ensemble portfolio for reducing biased trading actions and balancing the overall returns and risks. The experimental results clearly demonstrate that the MASAAT framework achieves impressive enhancement when compared with many well-known portfolio optimsation approaches on three challenging data sets of DJIA, S&P 500 and CSI 300. More importantly, our proposal has potential strengths in many possible applications for future study.

Read more4/16/2024

🤯

0

Inference of Utilities and Time Preference in Sequential Decision-Making

Haoyang Cao, Zhengqi Wu, Renyuan Xu

This paper introduces a novel stochastic control framework to enhance the capabilities of automated investment managers, or robo-advisors, by accurately inferring clients' investment preferences from past activities. Our approach leverages a continuous-time model that incorporates utility functions and a generic discounting scheme of a time-varying rate, tailored to each client's risk tolerance, valuation of daily consumption, and significant life goals. We address the resulting time inconsistency issue through state augmentation and the establishment of the dynamic programming principle and the verification theorem. Additionally, we provide sufficient conditions for the identifiability of client investment preferences. To complement our theoretical developments, we propose a learning algorithm based on maximum likelihood estimation within a discrete-time Markov Decision Process framework, augmented with entropy regularization. We prove that the log-likelihood function is locally concave, facilitating the fast convergence of our proposed algorithm. Practical effectiveness and efficiency are showcased through two numerical examples, including Merton's problem and an investment problem with unhedgeable risks. Our proposed framework not only advances financial technology by improving personalized investment advice but also contributes broadly to other fields such as healthcare, economics, and artificial intelligence, where understanding individual preferences is crucial.

Read more6/5/2024