Event Detection via Probability Density Function Regression

0

Sign in to get full access

Overview

- Proposes a novel method for event detection using probability density function (PDF) regression

- Aims to accurately identify the occurrence of events in time series data

- Developed as an alternative to traditional event detection approaches that may struggle with complex, nonlinear data

Plain English Explanation

Event detection is the task of identifying significant occurrences or changes in time series data, such as stock prices, sensor readings, or network traffic. This paper presents a new approach to event detection that uses probability density function (PDF) regression.

The key idea is to model the underlying distribution of the data using a PDF, and then detect events as points where the PDF changes significantly. This is different from traditional methods that may rely on thresholds, change point detection, or other heuristics that may not work well for complex, nonlinear data.

By using PDF regression, the method can capture more nuanced changes in the data distribution and identify events that may be missed by other techniques. The authors demonstrate the effectiveness of their approach on several real-world datasets, showing that it can outperform existing event detection methods.

Technical Explanation

The paper proposes a PDF regression-based event detection framework that models the underlying data distribution and identifies events as points where the PDF changes significantly. Specifically, the method involves:

- Modeling the time series data using a PDF regression model, such as a kernel density estimator or a Gaussian mixture model.

- Continuously monitoring the PDF and detecting events when the PDF changes beyond a certain threshold, indicating a significant change in the data distribution.

- Incorporating a significance testing procedure to distinguish between genuine events and random fluctuations in the data.

The authors evaluate their approach on synthetic and real-world datasets, including stock prices, network traffic, and sensor measurements. They compare the performance of their PDF regression-based method to several baseline event detection techniques, such as change point detection and sliding window approaches.

The results demonstrate that the proposed method can effectively identify events in complex, nonlinear data, outperforming the baselines in terms of precision, recall, and F1-score. The authors also highlight the ability of their approach to handle noisy and irregular data, which can be a challenge for traditional event detection methods.

Critical Analysis

The paper presents a compelling approach to event detection that addresses some of the limitations of existing techniques. By modeling the data distribution using PDF regression, the method can capture more nuanced changes in the data and identify events that may be missed by simpler thresholding or change point detection methods.

However, the authors acknowledge that the performance of the method can be sensitive to the choice of PDF regression model and the selection of appropriate significance testing thresholds. Additionally, the paper does not provide extensive comparisons to more advanced event detection methods, such as those based on deep learning or other modern techniques.

Further research could explore ways to make the method more robust to model selection and parameter tuning, as well as investigate its performance on a wider range of datasets and applications. Comparing the approach to state-of-the-art event detection methods would also help to better understand its strengths and limitations.

Conclusion

This paper presents a novel event detection method based on probability density function regression. By modeling the underlying data distribution and detecting significant changes in the PDF, the approach can effectively identify events in complex, nonlinear time series data.

The results demonstrate the potential of this technique to outperform traditional event detection methods, particularly in scenarios with noisy or irregular data. While the method has some limitations that require further investigation, it represents an interesting and promising direction for improving event detection in a wide range of applications.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Event Detection via Probability Density Function Regression

Clark Peng, Tolga Dinc{c}er

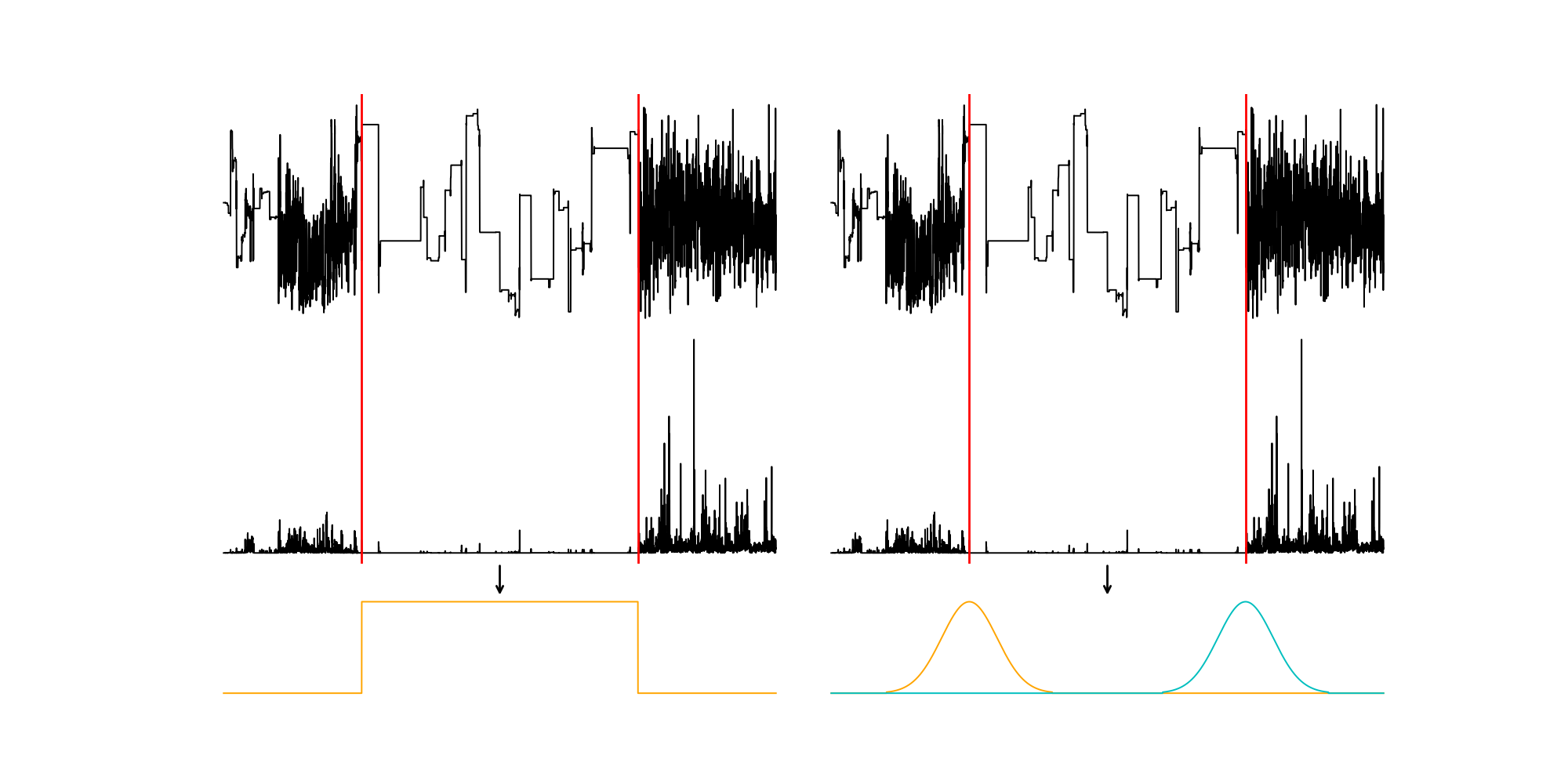

In the domain of time series analysis, particularly in event detection tasks, current methodologies predominantly rely on segmentation-based approaches, which predict the class label for each individual timesteps and use the changepoints of these labels to detect events. However, these approaches may not effectively detect the precise onset and offset of events within the data and suffer from class imbalance problems. This study introduces a generalized regression-based approach to reframe the time-interval-defined event detection problem. Inspired by heatmap regression techniques from computer vision, our approach aims to predict probability densities at event locations rather than class labels across the entire time series. The primary aim of this approach is to improve the accuracy of event detection methods, particularly for long-duration events where identifying the onset and offset is more critical than classifying individual event states. We demonstrate that regression-based approaches outperform segmentation-based methods across various state-of-the-art baseline networks and datasets, offering a more effective solution for specific event detection tasks.

Read more8/26/2024

0

New!Event Detection in Time Series: Universal Deep Learning Approach

Menouar Azib, Benjamin Renard, Philippe Garnier, Vincent G'enot, Nicolas Andr'e

Event detection in time series is a challenging task due to the prevalence of imbalanced datasets, rare events, and time interval-defined events. Traditional supervised deep learning methods primarily employ binary classification, where each time step is assigned a binary label indicating the presence or absence of an event. However, these methods struggle to handle these specific scenarios effectively. To address these limitations, we propose a novel supervised regression-based deep learning approach that offers several advantages over classification-based methods. Our approach, with a limited number of parameters, can effectively handle various types of events within a unified framework, including rare events and imbalanced datasets. We provide theoretical justifications for its universality and precision and demonstrate its superior performance across diverse domains, particularly for rare events and imbalanced datasets.

Read more9/16/2024

0

Event prediction and causality inference despite incomplete information

Harrison Lam, Yuanjie Chen, Noboru Kanazawa, Mohammad Chowdhury, Anna Battista, Stephan Waldert

We explored the challenge of predicting and explaining the occurrence of events within sequences of data points. Our focus was particularly on scenarios in which unknown triggers causing the occurrence of events may consist of non-consecutive, masked, noisy data points. This scenario is akin to an agent tasked with learning to predict and explain the occurrence of events without understanding the underlying processes or having access to crucial information. Such scenarios are encountered across various fields, such as genomics, hardware and software verification, and financial time series prediction. We combined analytical, simulation, and machine learning (ML) approaches to investigate, quantify, and provide solutions to this challenge. We deduced and validated equations generally applicable to any variation of the underlying challenge. Using these equations, we (1) described how the level of complexity changes with various parameters (e.g., number of apparent and hidden states, trigger length, confidence, etc.) and (2) quantified the data needed to successfully train an ML model. We then (3) proved our ML solution learns and subsequently identifies unknown triggers and predicts the occurrence of events. If the complexity of the challenge is too high, our ML solution can identify trigger candidates to be used to interactively probe the system under investigation to determine the true trigger in a way considerably more efficient than brute force methods. By sharing our findings, we aim to assist others grappling with similar challenges, enabling estimates on the complexity of their problem, the data required and a solution to solve it.

Read more6/11/2024

0

An evidential time-to-event prediction model based on Gaussian random fuzzy numbers

Ling Huang, Yucheng Xing, Thierry Denoeux, Mengling Feng

We introduce an evidential model for time-to-event prediction with censored data. In this model, uncertainty on event time is quantified by Gaussian random fuzzy numbers, a newly introduced family of random fuzzy subsets of the real line with associated belief functions, generalizing both Gaussian random variables and Gaussian possibility distributions. Our approach makes minimal assumptions about the underlying time-to-event distribution. The model is fit by minimizing a generalized negative log-likelihood function that accounts for both normal and censored data. Comparative experiments on two real-world datasets demonstrate the very good performance of our model as compared to the state-of-the-art.

Read more6/21/2024