Markowitz Meets Bellman: Knowledge-distilled Reinforcement Learning for Portfolio Management

0

Sign in to get full access

Overview

- This paper presents a new approach to portfolio management using a combination of Markowitz's modern portfolio theory and deep reinforcement learning.

- The researchers developed a knowledge-distilled reinforcement learning (KDRL) algorithm that can learn effective portfolio management strategies from historical data.

- The KDRL model is designed to be more sample-efficient and robust compared to traditional deep reinforcement learning approaches.

Plain English Explanation

The paper looks at the problem of portfolio management, which is the process of deciding how to invest money across different assets like stocks, bonds, and real estate to achieve the best balance of risk and return.

The Markowitz model is a classic approach to portfolio management that uses mathematical optimization to find the optimal mix of assets. However, the Markowitz model has some limitations, such as its reliance on historical data and its inability to adapt to changing market conditions.

The researchers in this paper propose using a deep reinforcement learning approach to portfolio management, which allows the model to learn effective strategies directly from data. Specifically, they developed a "knowledge-distilled" reinforcement learning algorithm that is designed to be more sample-efficient and robust compared to traditional deep reinforcement learning approaches.

The key idea is to have the reinforcement learning model "learn" from a pre-trained model that has been imbued with knowledge about portfolio management, similar to how knowledge distillation is used to transfer knowledge from a large, complex model to a smaller, more efficient one.

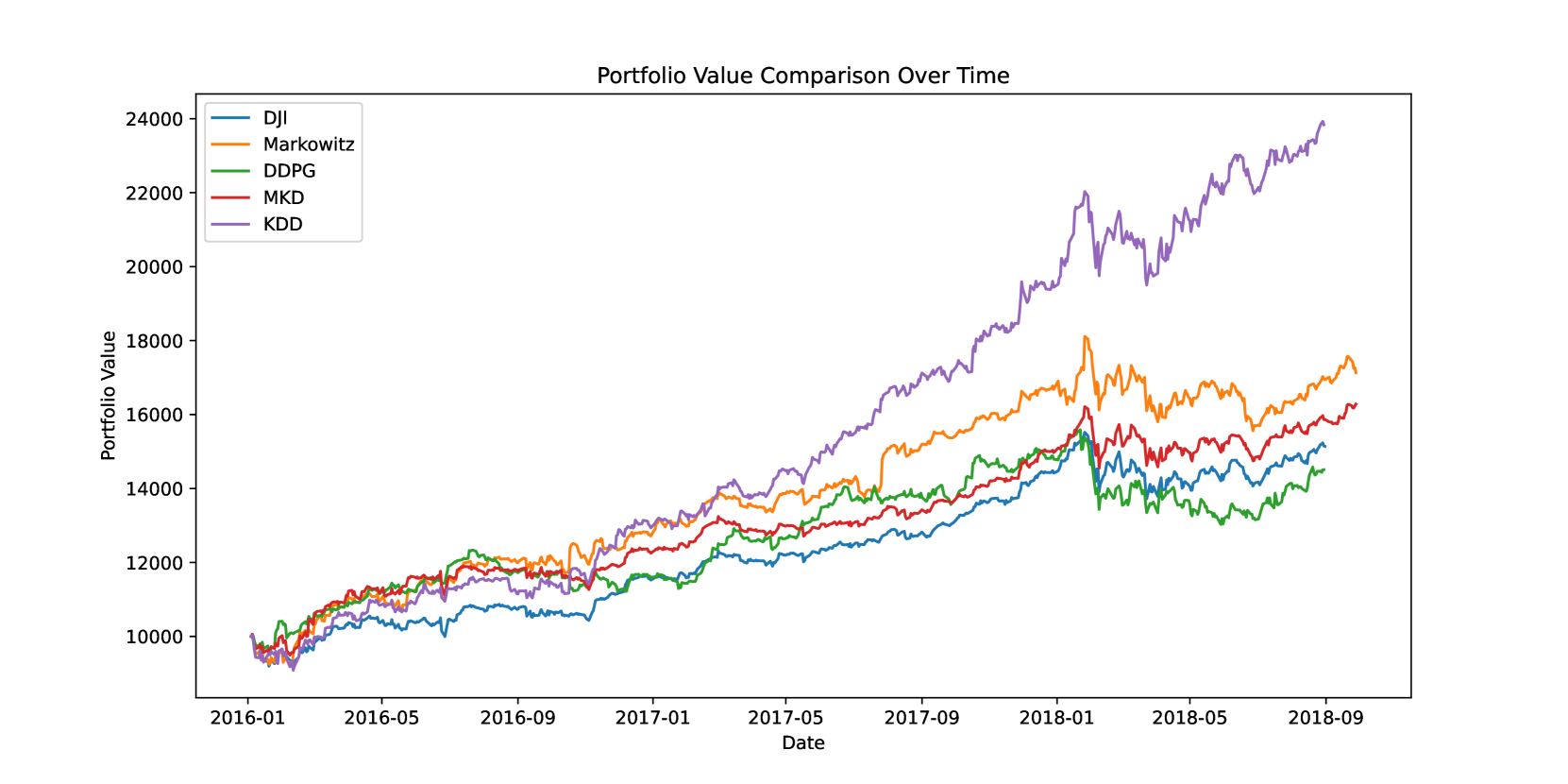

The researchers tested their KDRL model on historical financial data and found that it was able to outperform both the Markowitz model and a standard deep reinforcement learning approach in terms of risk-adjusted returns. This suggests that the KDRL model is a promising new tool for portfolio management that can adapt to changing market conditions while maintaining strong performance.

Technical Explanation

The paper presents a new approach to portfolio management called "knowledge-distilled reinforcement learning" (KDRL). The key idea is to combine Markowitz's modern portfolio theory with deep reinforcement learning in order to learn effective portfolio management strategies from historical data.

The researchers first train a Markowitz-based model to serve as a "teacher" for the reinforcement learning agent. This Markowitz model provides the reinforcement learning agent with valuable prior knowledge about portfolio management, which helps the agent learn more efficiently.

The reinforcement learning agent is then trained using a novel "knowledge distillation" approach, where the agent tries to mimic the behavior of the Markowitz teacher model. This knowledge distillation process helps the agent learn more sample-efficiently and robustly compared to standard deep reinforcement learning approaches.

The researchers tested their KDRL model on historical financial data and found that it was able to outperform both the Markowitz model and a standard deep reinforcement learning approach in terms of risk-adjusted returns. This suggests that the KDRL model is a promising new tool for portfolio management that can adapt to changing market conditions while maintaining strong performance.

The paper also discusses several extensions and applications of the KDRL framework, including its potential use in multi-agent reinforcement learning settings and information-directed sampling algorithms for more efficient exploration.

Critical Analysis

The paper presents a novel and promising approach to portfolio management that combines the strengths of Markowitz's modern portfolio theory and deep reinforcement learning. The knowledge distillation technique used to train the reinforcement learning agent is particularly interesting, as it allows the agent to benefit from the prior knowledge encoded in the Markowitz model while still maintaining the flexibility and adaptability of a deep learning-based approach.

One potential limitation of the KDRL approach is its reliance on historical data, which may not always be a reliable guide to future market behavior. The researchers acknowledge this challenge and suggest that incorporating additional market data and external knowledge could help the model better adapt to changing conditions.

Additionally, while the KDRL model outperformed the Markowitz model and a standard deep reinforcement learning approach in the reported experiments, it would be valuable to see how it compares to other state-of-the-art portfolio management techniques, such as those that incorporate interaction-aware planning or robust multi-agent reinforcement learning strategies.

Overall, the KDRL framework presented in this paper is a promising step forward in the field of portfolio management, and the researchers' focus on sample efficiency and robustness is particularly commendable. As with any new approach, further research and real-world testing will be necessary to fully assess its capabilities and limitations.

Conclusion

This paper introduces a novel knowledge-distilled reinforcement learning (KDRL) approach to portfolio management that combines the strengths of Markowitz's modern portfolio theory and deep reinforcement learning. The KDRL model is designed to be more sample-efficient and robust compared to traditional deep reinforcement learning approaches, and the researchers found that it outperformed both the Markowitz model and a standard deep reinforcement learning approach in their experiments.

The KDRL framework represents a promising new direction in portfolio management, as it has the potential to adapt to changing market conditions while maintaining strong risk-adjusted returns. Furthermore, the knowledge distillation technique used in the KDRL model could have broader applications in other areas of finance and beyond, making this research a valuable contribution to the field of AI and machine learning.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Markowitz Meets Bellman: Knowledge-distilled Reinforcement Learning for Portfolio Management

Gang Hu, Ming Gu

Investment portfolios, central to finance, balance potential returns and risks. This paper introduces a hybrid approach combining Markowitz's portfolio theory with reinforcement learning, utilizing knowledge distillation for training agents. In particular, our proposed method, called KDD (Knowledge Distillation DDPG), consist of two training stages: supervised and reinforcement learning stages. The trained agents optimize portfolio assembly. A comparative analysis against standard financial models and AI frameworks, using metrics like returns, the Sharpe ratio, and nine evaluation indices, reveals our model's superiority. It notably achieves the highest yield and Sharpe ratio of 2.03, ensuring top profitability with the lowest risk in comparable return scenarios.

Read more5/10/2024

0

Portfolio Management using Deep Reinforcement Learning

Ashish Anil Pawar, Vishnureddy Prashant Muskawar, Ritesh Tiku

Algorithmic trading or Financial robots have been conquering the stock markets with their ability to fathom complex statistical trading strategies. But with the recent development of deep learning technologies, these strategies are becoming impotent. The DQN and A2C models have previously outperformed eminent humans in game-playing and robotics. In our work, we propose a reinforced portfolio manager offering assistance in the allocation of weights to assets. The environment proffers the manager the freedom to go long and even short on the assets. The weight allocation advisements are restricted to the choice of portfolio assets and tested empirically to knock benchmark indices. The manager performs financial transactions in a postulated liquid market without any transaction charges. This work provides the conclusion that the proposed portfolio manager with actions centered on weight allocations can surpass the risk-adjusted returns of conventional portfolio managers.

Read more5/6/2024

0

New!A Deep Reinforcement Learning Framework For Financial Portfolio Management

Jinyang Li

In this research paper, we investigate into a paper named A Deep Reinforcement Learning Framework for the Financial Portfolio Management Problem [arXiv:1706.10059]. It is a portfolio management problem which is solved by deep learning techniques. The original paper proposes a financial-model-free reinforcement learning framework, which consists of the Ensemble of Identical Independent Evaluators (EIIE) topology, a Portfolio-Vector Memory (PVM), an Online Stochastic Batch Learning (OSBL) scheme, and a fully exploiting and explicit reward function. Three different instants are used to realize this framework, namely a Convolutional Neural Network (CNN), a basic Recurrent Neural Network (RNN), and a Long Short-Term Memory (LSTM). The performance is then examined by comparing to a number of recently reviewed or published portfolio-selection strategies. We have successfully replicated their implementations and evaluations. Besides, we further apply this framework in the stock market, instead of the cryptocurrency market that the original paper uses. The experiment in the cryptocurrency market is consistent with the original paper, which achieve superior returns. But it doesn't perform as well when applied in the stock market.

Read more9/16/2024

0

Explainable Post hoc Portfolio Management Financial Policy of a Deep Reinforcement Learning agent

Alejandra de la Rica Escudero, Eduardo C. Garrido-Merchan, Maria Coronado-Vaca

Financial portfolio management investment policies computed quantitatively by modern portfolio theory techniques like the Markowitz model rely on a set on assumptions that are not supported by data in high volatility markets. Hence, quantitative researchers are looking for alternative models to tackle this problem. Concretely, portfolio management is a problem that has been successfully addressed recently by Deep Reinforcement Learning (DRL) approaches. In particular, DRL algorithms train an agent by estimating the distribution of the expected reward of every action performed by an agent given any financial state in a simulator. However, these methods rely on Deep Neural Networks model to represent such a distribution, that although they are universal approximator models, they cannot explain its behaviour, given by a set of parameters that are not interpretable. Critically, financial investors policies require predictions to be interpretable, so DRL agents are not suited to follow a particular policy or explain their actions. In this work, we developed a novel Explainable Deep Reinforcement Learning (XDRL) approach for portfolio management, integrating the Proximal Policy Optimization (PPO) with the model agnostic explainable techniques of feature importance, SHAP and LIME to enhance transparency in prediction time. By executing our methodology, we can interpret in prediction time the actions of the agent to assess whether they follow the requisites of an investment policy or to assess the risk of following the agent suggestions. To the best of our knowledge, our proposed approach is the first explainable post hoc portfolio management financial policy of a DRL agent. We empirically illustrate our methodology by successfully identifying key features influencing investment decisions, which demonstrate the ability to explain the agent actions in prediction time.

Read more7/22/2024