Robust Predictions with Ambiguous Time Delays: A Bootstrap Strategy

0

Sign in to get full access

Overview

- Paper proposes a bootstrap-based strategy for making robust predictions with ambiguous time delays

- Focuses on time series forecasting tasks with uncertain time lags between variables

- Introduces a resampling approach to capture the impact of unknown time delays on prediction performance

Plain English Explanation

This paper tackles the challenge of making accurate predictions when the time delays between related variables are unclear or unknown. In many real-world forecasting problems, such as predicting stock prices or electricity demand, the time it takes for changes in one factor to affect another is often uncertain.

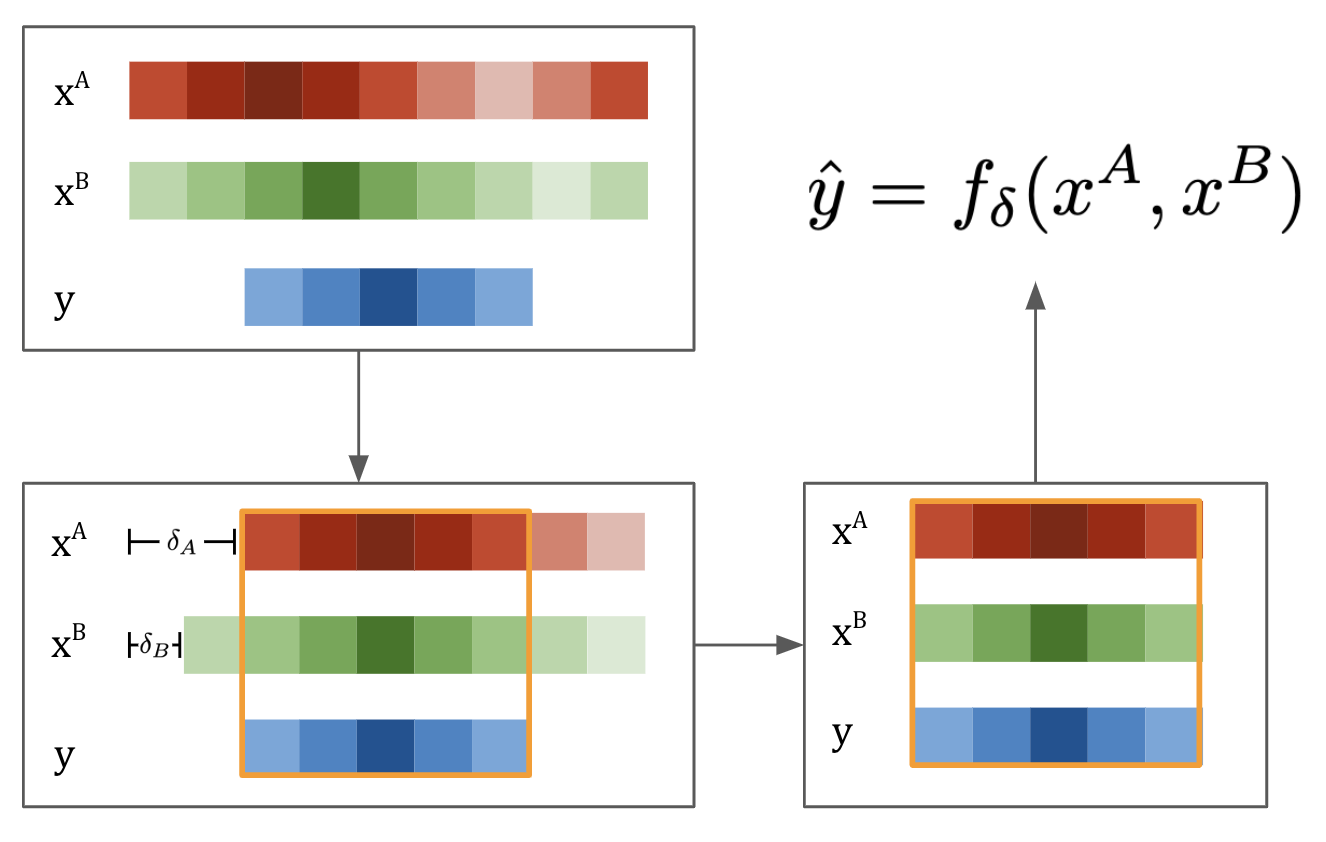

The researchers introduce a bootstrap strategy to address this issue. The bootstrap is a statistical technique that involves resampling the original data to generate multiple versions of the dataset. By repeatedly fitting a predictive model on these resampled datasets, the researchers can estimate the impact of the uncertain time delays on the model's performance.

This approach allows them to make more robust predictions that account for the ambiguity in the time lags between the variables. Rather than assuming a single fixed time delay, the bootstrap strategy captures the range of possible lags and their effects on the predictions.

Technical Explanation

The paper proposes a bootstrap-based approach for making predictions in the presence of ambiguous time delays between variables in a time series forecasting task.

The key steps of the method are:

- Construct bootstrap samples: The original time series data is resampled with replacement to generate multiple bootstrap datasets.

- Fit predictive models: A predictive model (e.g., a regression or machine learning model) is trained on each bootstrap sample.

- Evaluate model performance: The predictive performance of each model is assessed on a held-out test set.

- Aggregate predictions: The predictions from the individual bootstrap models are combined to produce a final, robust prediction that accounts for the uncertainty in the time delays.

By repeatedly fitting the predictive model on the resampled data, the approach captures the impact of the unknown time lags on the model's performance. This allows the researchers to quantify the sensitivity of the predictions to the ambiguous time delays and make more robust forecasts.

The paper demonstrates the effectiveness of this bootstrap strategy through experiments on both simulated and real-world time series datasets, showing improved prediction accuracy and uncertainty quantification compared to standard forecasting methods.

Critical Analysis

The paper provides a thoughtful approach to handling ambiguous time delays in time series forecasting, a common issue in many practical applications. The bootstrap strategy is a well-established technique that the authors leverage effectively to capture the impact of the unknown time lags on the predictive performance.

One potential limitation is that the method assumes the time delays are constant over time, whereas in reality, they may change dynamically. Extending the approach to handle time-varying time lags could be an interesting area for future research.

Additionally, the paper focuses on demonstrating the effectiveness of the bootstrap strategy through empirical evaluation, but a more in-depth theoretical analysis of the properties and convergence of the proposed method could further strengthen the contribution.

Overall, the paper presents a practical and well-designed solution to a relevant problem in time series forecasting, which could have important implications for applications where accounting for uncertainty in time delays is crucial.

Conclusion

This paper introduces a bootstrap-based strategy for making robust predictions in the presence of ambiguous time delays between variables in a time series forecasting task. By resampling the original data and fitting predictive models on the bootstrap samples, the approach captures the impact of the unknown time lags on the model's performance, allowing for more reliable and accurate forecasts.

The empirical results demonstrate the effectiveness of this method, which could have significant applications in domains where accounting for uncertainty in the time delays between variables is crucial, such as finance, energy forecasting, and supply chain management.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Robust Predictions with Ambiguous Time Delays: A Bootstrap Strategy

Jiajie Wang, Zhiyuan Jerry Lin, Wen Chen

In contemporary data-driven environments, the generation and processing of multivariate time series data is an omnipresent challenge, often complicated by time delays between different time series. These delays, originating from a multitude of sources like varying data transmission dynamics, sensor interferences, and environmental changes, introduce significant complexities. Traditional Time Delay Estimation methods, which typically assume a fixed constant time delay, may not fully capture these variabilities, compromising the precision of predictive models in diverse settings. To address this issue, we introduce the Time Series Model Bootstrap (TSMB), a versatile framework designed to handle potentially varying or even nondeterministic time delays in time series modeling. Contrary to traditional approaches that hinge on the assumption of a single, consistent time delay, TSMB adopts a nonparametric stance, acknowledging and incorporating time delay uncertainties. TSMB significantly bolsters the performance of models that are trained and make predictions using this framework, making it highly suitable for a wide range of dynamic and interconnected data environments.

Read more8/26/2024

👨🏫

0

Surrogate uncertainty estimation for your time series forecasting black-box: learn when to trust

Leonid Erlygin, Vladimir Zholobov, Valeriia Baklanova, Evgeny Sokolovskiy, Alexey Zaytsev

Machine learning models play a vital role in time series forecasting. These models, however, often overlook an important element: point uncertainty estimates. Incorporating these estimates is crucial for effective risk management, informed model selection, and decision-making.To address this issue, our research introduces a method for uncertainty estimation. We employ a surrogate Gaussian process regression model. It enhances any base regression model with reasonable uncertainty estimates. This approach stands out for its computational efficiency. It only necessitates training one supplementary surrogate and avoids any data-specific assumptions. Furthermore, this method for work requires only the presence of the base model as a black box and its respective training data. The effectiveness of our approach is supported by experimental results. Using various time-series forecasting data, we found that our surrogate model-based technique delivers significantly more accurate confidence intervals. These techniques outperform both bootstrap-based and built-in methods in a medium-data regime. This superiority holds across a range of base model types, including a linear regression, ARIMA, gradient boosting and a neural network.

Read more9/11/2024

0

Rating Multi-Modal Time-Series Forecasting Models (MM-TSFM) for Robustness Through a Causal Lens

Kausik Lakkaraju, Rachneet Kaur, Zhen Zeng, Parisa Zehtabi, Sunandita Patra, Biplav Srivastava, Marco Valtorta

AI systems are notorious for their fragility; minor input changes can potentially cause major output swings. When such systems are deployed in critical areas like finance, the consequences of their uncertain behavior could be severe. In this paper, we focus on multi-modal time-series forecasting, where imprecision due to noisy or incorrect data can lead to erroneous predictions, impacting stakeholders such as analysts, investors, and traders. Recently, it has been shown that beyond numeric data, graphical transformations can be used with advanced visual models to achieve better performance. In this context, we introduce a rating methodology to assess the robustness of Multi-Modal Time-Series Forecasting Models (MM-TSFM) through causal analysis, which helps us understand and quantify the isolated impact of various attributes on the forecasting accuracy of MM-TSFM. We apply our novel rating method on a variety of numeric and multi-modal forecasting models in a large experimental setup (six input settings of control and perturbations, ten data distributions, time series from six leading stocks in three industries over a year of data, and five time-series forecasters) to draw insights on robust forecasting models and the context of their strengths. Within the scope of our study, our main result is that multi-modal (numeric + visual) forecasting, which was found to be more accurate than numeric forecasting in previous studies, can also be more robust in diverse settings. Our work will help different stakeholders of time-series forecasting understand the models` behaviors along trust (robustness) and accuracy dimensions to select an appropriate model for forecasting using our rating method, leading to improved decision-making.

Read more6/21/2024

0

Test Time Learning for Time Series Forecasting

Panayiotis Christou, Shichu Chen, Xupeng Chen, Parijat Dube

Time-series forecasting has seen significant advancements with the introduction of token prediction mechanisms such as multi-head attention. However, these methods often struggle to achieve the same performance as in language modeling, primarily due to the quadratic computational cost and the complexity of capturing long-range dependencies in time-series data. State-space models (SSMs), such as Mamba, have shown promise in addressing these challenges by offering efficient solutions with linear RNNs capable of modeling long sequences with larger context windows. However, there remains room for improvement in accuracy and scalability. We propose the use of Test-Time Training (TTT) modules in a parallel architecture to enhance performance in long-term time series forecasting. Through extensive experiments on standard benchmark datasets, we demonstrate that TTT modules consistently outperform state-of-the-art models, including the Mamba-based TimeMachine, particularly in scenarios involving extended sequence and prediction lengths. Our results show significant improvements in Mean Squared Error (MSE) and Mean Absolute Error (MAE), especially on larger datasets such as Electricity, Traffic, and Weather, underscoring the effectiveness of TTT in capturing long-range dependencies. Additionally, we explore various convolutional architectures within the TTT framework, showing that even simple configurations like 1D convolution with small filters can achieve competitive results. This work sets a new benchmark for time-series forecasting and lays the groundwork for future research in scalable, high-performance forecasting models.

Read more9/24/2024