Rating Multi-Modal Time-Series Forecasting Models (MM-TSFM) for Robustness Through a Causal Lens

0

Sign in to get full access

Related Work

Time-Series Forecasting with Large Language Models

Recent research has explored using large language models (LLMs) for time-series forecasting, such as TimeCMA: Towards LLM-Empowered Time-Series Forecasting and CALF: Aligning LLMs for Time-Series Forecasting via Causal Learning. These approaches leverage the powerful language understanding capabilities of LLMs to enhance traditional time-series forecasting techniques.

Multi-Modal Robustness

Another related area is research on quantifying and enhancing the multi-modal robustness of forecasting models, as seen in papers like Quantifying and Enhancing Multi-Modal Robustness through Modality Preference. These studies explore techniques to make forecasting models more resilient to missing or corrupted input data across different modalities.

Multi-Modal Spatio-Temporal Forecasting

The challenge of multi-modal spatio-temporal forecasting has also been investigated, as demonstrated in Multi-Modality Spatio-Temporal Forecasting via Self-Supervised Representation Learning. This work focuses on developing models that can effectively leverage diverse data sources to improve forecasting performance in complex, multi-dimensional scenarios.

Benchmarking Forecasting Models

Lastly, the paper ProbTS: Benchmarking Point and Distributional Forecasting Across Diverse Time Series introduces a comprehensive evaluation framework for assessing the performance of time-series forecasting models, including both point and distributional forecasts.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Rating Multi-Modal Time-Series Forecasting Models (MM-TSFM) for Robustness Through a Causal Lens

Kausik Lakkaraju, Rachneet Kaur, Zhen Zeng, Parisa Zehtabi, Sunandita Patra, Biplav Srivastava, Marco Valtorta

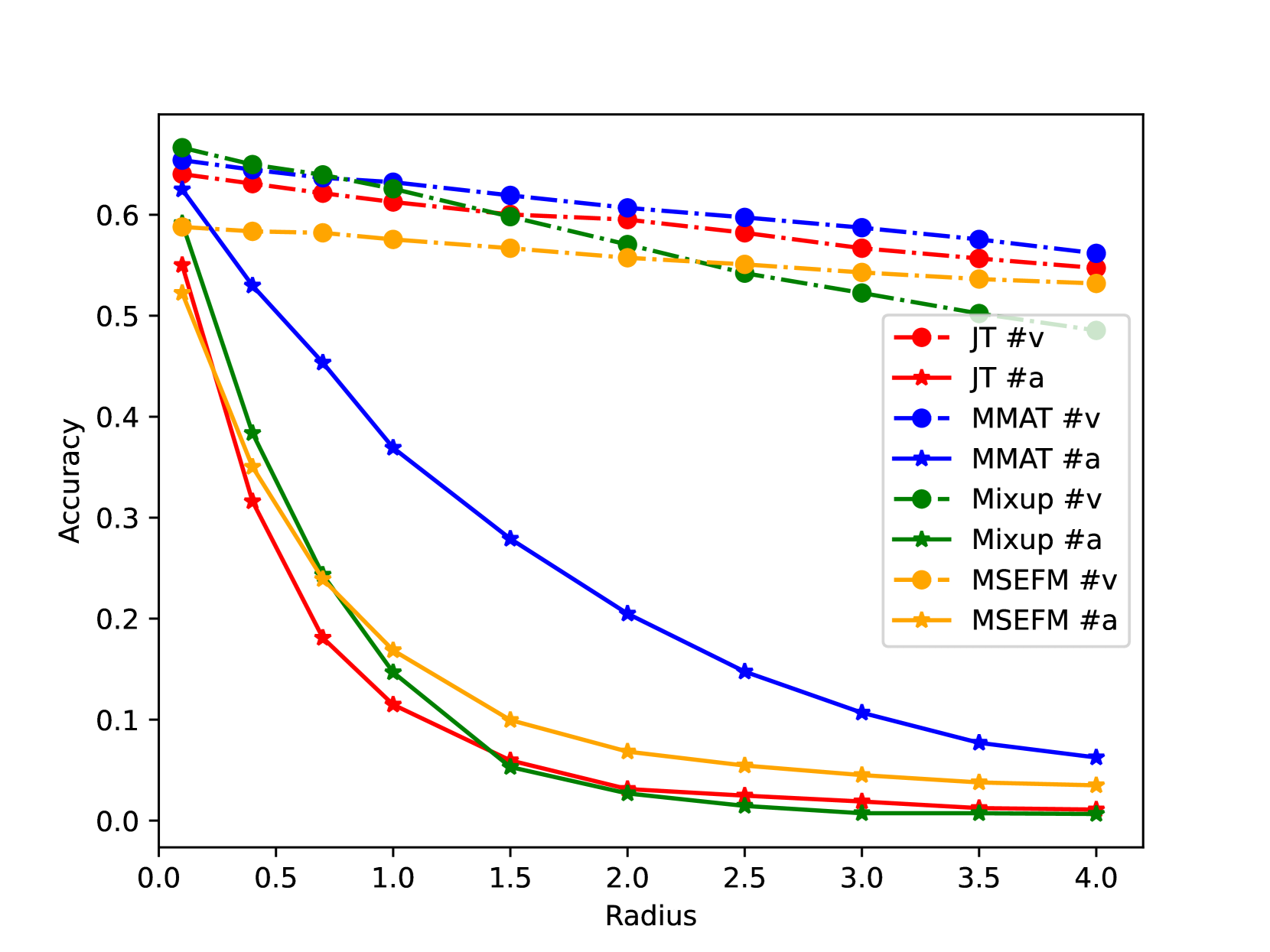

AI systems are notorious for their fragility; minor input changes can potentially cause major output swings. When such systems are deployed in critical areas like finance, the consequences of their uncertain behavior could be severe. In this paper, we focus on multi-modal time-series forecasting, where imprecision due to noisy or incorrect data can lead to erroneous predictions, impacting stakeholders such as analysts, investors, and traders. Recently, it has been shown that beyond numeric data, graphical transformations can be used with advanced visual models to achieve better performance. In this context, we introduce a rating methodology to assess the robustness of Multi-Modal Time-Series Forecasting Models (MM-TSFM) through causal analysis, which helps us understand and quantify the isolated impact of various attributes on the forecasting accuracy of MM-TSFM. We apply our novel rating method on a variety of numeric and multi-modal forecasting models in a large experimental setup (six input settings of control and perturbations, ten data distributions, time series from six leading stocks in three industries over a year of data, and five time-series forecasters) to draw insights on robust forecasting models and the context of their strengths. Within the scope of our study, our main result is that multi-modal (numeric + visual) forecasting, which was found to be more accurate than numeric forecasting in previous studies, can also be more robust in diverse settings. Our work will help different stakeholders of time-series forecasting understand the models` behaviors along trust (robustness) and accuracy dimensions to select an appropriate model for forecasting using our rating method, leading to improved decision-making.

Read more6/21/2024

0

TimeCMA: Towards LLM-Empowered Time Series Forecasting via Cross-Modality Alignment

Chenxi Liu, Qianxiong Xu, Hao Miao, Sun Yang, Lingzheng Zhang, Cheng Long, Ziyue Li, Rui Zhao

The widespread adoption of scalable mobile sensing has led to large amounts of time series data for real-world applications. A fundamental application is multivariate time series forecasting (MTSF), which aims to predict future time series values based on historical observations. Existing MTSF methods suffer from limited parameterization and small-scale training data. Recently, Large language models (LLMs) have been introduced in time series, which achieve promising forecasting performance but incur heavy computational costs. To solve these challenges, we propose TimeCMA, an LLM-empowered framework for time series forecasting with cross-modality alignment. We design a dual-modality encoding module with two branches, where the time series encoding branch extracts relatively low-quality yet pure embeddings of time series through an inverted Transformer. In addition, the LLM-empowered encoding branch wraps the same time series as prompts to obtain high-quality yet entangled prompt embeddings via a Pre-trained LLM. Then, we design a cross-modality alignment module to retrieve high-quality and pure time series embeddings from the prompt embeddings. Moreover, we develop a time series forecasting module to decode the aligned embeddings while capturing dependencies among multiple variables for forecasting. Notably, we tailor the prompt to encode sufficient temporal information into a last token and design the last token embedding storage to reduce computational costs. Extensive experiments on real data offer insight into the accuracy and efficiency of the proposed framework.

Read more6/17/2024

0

Quantifying and Enhancing Multi-modal Robustness with Modality Preference

Zequn Yang, Yake Wei, Ce Liang, Di Hu

Multi-modal models have shown a promising capability to effectively integrate information from various sources, yet meanwhile, they are found vulnerable to pervasive perturbations, such as uni-modal attacks and missing conditions. To counter these perturbations, robust multi-modal representations are highly expected, which are positioned well away from the discriminative multi-modal decision boundary. In this paper, different from conventional empirical studies, we focus on a commonly used joint multi-modal framework and theoretically discover that larger uni-modal representation margins and more reliable integration for modalities are essential components for achieving higher robustness. This discovery can further explain the limitation of multi-modal robustness and the phenomenon that multi-modal models are often vulnerable to attacks on the specific modality. Moreover, our analysis reveals how the widespread issue, that the model has different preferences for modalities, limits the multi-modal robustness by influencing the essential components and could lead to attacks on the specific modality highly effective. Inspired by our theoretical finding, we introduce a training procedure called Certifiable Robust Multi-modal Training (CRMT), which can alleviate this influence from modality preference and explicitly regulate essential components to significantly improve robustness in a certifiable manner. Our method demonstrates substantial improvements in performance and robustness compared with existing methods. Furthermore, our training procedure can be easily extended to enhance other robust training strategies, highlighting its credibility and flexibility.

Read more4/19/2024

0

Multi-Knowledge Fusion Network for Time Series Representation Learning

Sagar Srinivas Sakhinana, Shivam Gupta, Krishna Sai Sudhir Aripirala, Venkataramana Runkana

Forecasting the behaviour of complex dynamical systems such as interconnected sensor networks characterized by high-dimensional multivariate time series(MTS) is of paramount importance for making informed decisions and planning for the future in a broad spectrum of applications. Graph forecasting networks(GFNs) are well-suited for forecasting MTS data that exhibit spatio-temporal dependencies. However, most prior works of GFN-based methods on MTS forecasting rely on domain-expertise to model the nonlinear dynamics of the system, but neglect the potential to leverage the inherent relational-structural dependencies among time series variables underlying MTS data. On the other hand, contemporary works attempt to infer the relational structure of the complex dependencies between the variables and simultaneously learn the nonlinear dynamics of the interconnected system but neglect the possibility of incorporating domain-specific prior knowledge to improve forecast accuracy. To this end, we propose a hybrid architecture that combines explicit prior knowledge with implicit knowledge of the relational structure within the MTS data. It jointly learns intra-series temporal dependencies and inter-series spatial dependencies by encoding time-conditioned structural spatio-temporal inductive biases to provide more accurate and reliable forecasts. It also models the time-varying uncertainty of the multi-horizon forecasts to support decision-making by providing estimates of prediction uncertainty. The proposed architecture has shown promising results on multiple benchmark datasets and outperforms state-of-the-art forecasting methods by a significant margin. We report and discuss the ablation studies to validate our forecasting architecture.

Read more8/23/2024