Beyond IID: data-driven decision-making in heterogeneous environments

0

📊

Sign in to get full access

Overview

- Explores how to leverage historical data when past observations may not perfectly predict the future due to unobserved confounding factors

- Proposes a data-driven decision-making framework where historical samples come from unknown distributions within a known "heterogeneity ball" around the unknown future distribution

- Analyzes the performance of data-driven policies, both central and near-optimal, in these heterogeneous environments

- Establishes bounds on the asymptotic worst-case regret of a broad class of policies

- Provides a general analysis of Sample Average Approximation (SAA) performance as a function of the heterogeneity ball radius

- Introduces the "approximation parameter" to capture how heterogeneity and problem structure impact SAA

- Illustrates the analysis on several widely-studied problems like newsvendor and pricing

- Motivates designing alternative rate-optimal policies when SAA fails

Plain English Explanation

This paper tackles the challenge of using historical data to make decisions when that data may not perfectly reflect the future. The researchers propose a framework where the historical data comes from unknown distributions, but those distributions are assumed to lie within a certain "heterogeneity ball" around the unknown future distribution.

Within this framework, the paper analyzes the performance of different decision-making policies, both those that are optimal on average and those that are near-optimal. The key contribution is establishing an upper bound on the "regret" - the difference between the policy's performance and the best possible performance - for a broad class of policies.

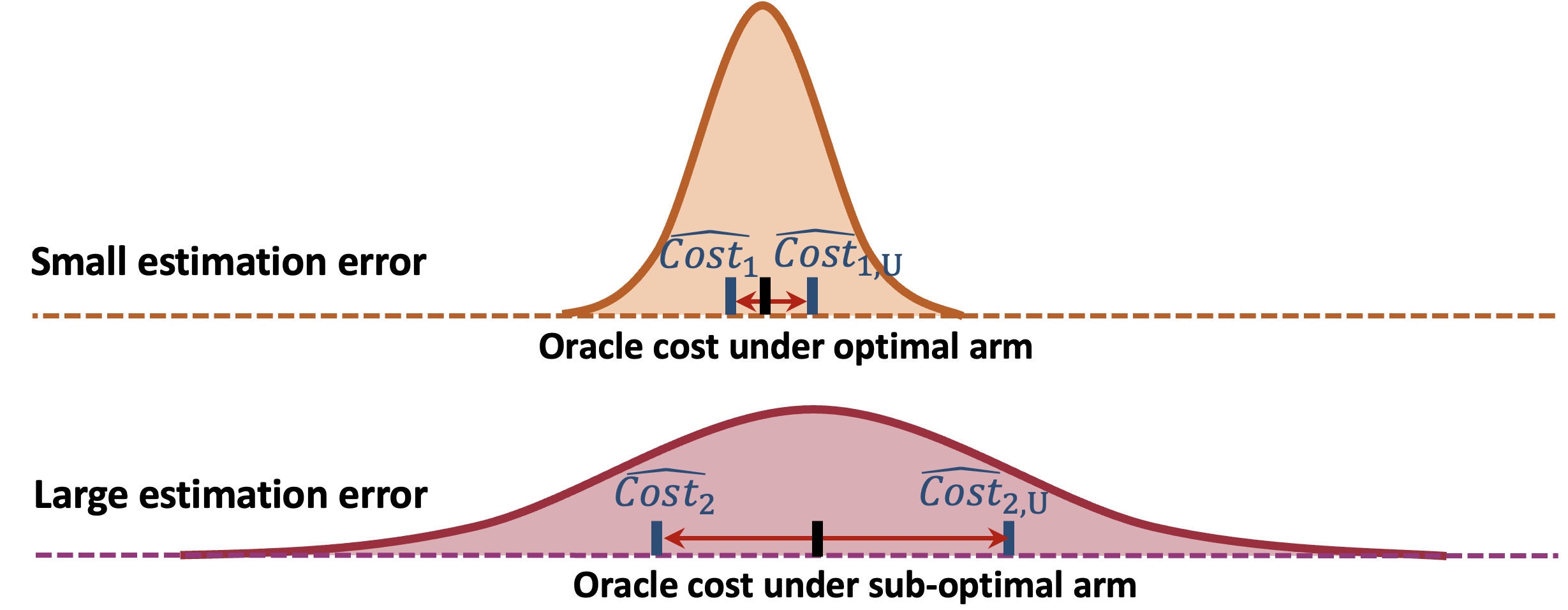

Building on this result, the paper then provides a detailed analysis of the Sample Average Approximation (SAA) policy, which uses the historical data to estimate the optimal decision. The analysis shows how the performance of SAA depends on the radius of the heterogeneity ball, as well as an "approximation parameter" that captures how the interplay between heterogeneity and problem structure impacts SAA.

The paper illustrates this analysis on several classic problems like the newsvendor problem and pricing. Interestingly, it finds that SAA can perform poorly in certain instances, motivating the design of alternative "rate-optimal" policies that can achieve strong performance guarantees.

Technical Explanation

The paper starts by introducing a data-driven decision-making framework where historical samples are drawn from unknown distributions that are assumed to lie within a known "heterogeneity ball" around the unknown future distribution. This setup captures scenarios where past observations may not perfectly predict the future due to unobserved confounding factors.

Within this framework, the authors analyze the performance of both central data-driven policies (which aim to optimize average-case performance) and near-optimal policies. They establish a key result that allows bounding the asymptotic worst-case regret of a broad class of policies.

Leveraging this result, the paper then provides a general analysis of the Sample Average Approximation (SAA) policy, which estimates the optimal decision using historical samples. The analysis characterizes SAA's performance as a function of the heterogeneity ball radius, introducing a novel notion of "approximation parameter" to capture how heterogeneity and problem structure interact.

The paper illustrates this analysis on several well-studied problems, including the newsvendor problem, pricing, and others. Interestingly, it finds that SAA can perform poorly in some instances, motivating the design of alternative rate-optimal policies.

Critical Analysis

The paper makes a valuable contribution by proposing a framework to analyze data-driven decision-making in the presence of heterogeneous historical data. The analysis of SAA's performance and the introduction of the "approximation parameter" provide useful insights into how problem structure and heterogeneity can impact the effectiveness of this widely-used policy.

That said, the paper does not address the challenging problem of how to estimate or bound the heterogeneity ball radius in practice. This information is assumed to be known, but in real-world settings, it may be difficult to obtain. Additionally, the paper focuses on asymptotic results, while practitioners may be more interested in finite-sample guarantees.

The design and analysis of rate-optimal policies are also still in the early stages, and the paper acknowledges that more work is needed to develop a principled approach for this task. Further research is required to better understand the tradeoffs between different policy design choices and their performance in heterogeneous environments.

Overall, this paper represents an important step forward in understanding the limitations of using historical data for decision-making and provides a foundation for developing more robust and adaptable policies. As the authors note, the insights from this work could be valuable for a wide range of applications, from adaptive data analysis to sequential decision-making with expert demonstrations and beyond.

Conclusion

This paper tackles the challenging problem of leveraging historical data for decision-making when past observations may not perfectly predict the future due to unobserved confounding factors. By proposing a framework of heterogeneous historical distributions within a known "ball" around the unknown future distribution, the authors are able to analyze the performance of both central and near-optimal data-driven policies.

The key contributions include establishing bounds on the asymptotic worst-case regret of a broad class of policies, as well as a detailed analysis of the Sample Average Approximation (SAA) policy. This analysis introduces the novel "approximation parameter" to capture the interplay between heterogeneity and problem structure, and illustrates how SAA's performance can vary considerably across different problem domains.

The failure of SAA in certain instances motivates the design of alternative rate-optimal policies, which the paper begins to explore. Overall, this work represents an important step forward in understanding the limitations of historical data and developing more robust decision-making frameworks, with potential applications across a wide range of fields.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

📊

0

Beyond IID: data-driven decision-making in heterogeneous environments

Omar Besbes, Will Ma, Omar Mouchtaki

How should one leverage historical data when past observations are not perfectly indicative of the future, e.g., due to the presence of unobserved confounders which one cannot correct for? Motivated by this question, we study a data-driven decision-making framework in which historical samples are generated from unknown and different distributions assumed to lie in a heterogeneity ball with known radius and centered around the (also) unknown future (out-of-sample) distribution on which the performance of a decision will be evaluated. This work aims at analyzing the performance of central data-driven policies but also near-optimal ones in these heterogeneous environments and understanding key drivers of performance. We establish a first result which allows to upper bound the asymptotic worst-case regret of a broad class of policies. Leveraging this result, for any integral probability metric, we provide a general analysis of the performance achieved by Sample Average Approximation (SAA) as a function of the radius of the heterogeneity ball. This analysis is centered around the approximation parameter, a notion of complexity we introduce to capture how the interplay between the heterogeneity and the problem structure impacts the performance of SAA. In turn, we illustrate through several widely-studied problems -- e.g., newsvendor, pricing -- how this methodology can be applied and find that the performance of SAA varies considerably depending on the combinations of problem classes and heterogeneity. The failure of SAA for certain instances motivates the design of alternative policies to achieve rate-optimality. We derive problem-dependent policies achieving strong guarantees for the illustrative problems described above and provide initial results towards a principled approach for the design and analysis of general rate-optimal algorithms.

Read more6/21/2024

0

Closing the Gaps: Optimality of Sample Average Approximation for Data-Driven Newsvendor Problems

Jiameng Lyu, Shilin Yuan, Bingkun Zhou, Yuan Zhou

We study the regret performance of Sample Average Approximation (SAA) for data-driven newsvendor problems with general convex inventory costs. In literature, the optimality of SAA has not been fully established under both alpha-global strong convexity and (alpha,beta)-local strong convexity (alpha-strongly convex within the beta-neighborhood of the optimal quantity) conditions. This paper closes the gaps between regret upper and lower bounds for both conditions. Under the (alpha,beta)-local strong convexity condition, we prove the optimal regret bound of Theta(log T/alpha + 1/ (alphabeta)) for SAA. This upper bound result demonstrates that the regret performance of SAA is only influenced by alpha and not by beta in the long run, enhancing our understanding about how local properties affect the long-term regret performance of decision-making strategies. Under the alpha-global strong convexity condition, we demonstrate that the worst-case regret of any data-driven method is lower bounded by Omega(log T/alpha), which is the first lower bound result that matches the existing upper bound with respect to both parameter alpha and time horizon T. Along the way, we propose to analyze the SAA regret via a new gradient approximation technique, as well as a new class of smooth inverted-hat-shaped hard problem instances that might be of independent interest for the lower bounds of broader data-driven problems.

Read more7/9/2024

0

Combining Experimental and Historical Data for Policy Evaluation

Ting Li, Chengchun Shi, Qianglin Wen, Yang Sui, Yongli Qin, Chunbo Lai, Hongtu Zhu

This paper studies policy evaluation with multiple data sources, especially in scenarios that involve one experimental dataset with two arms, complemented by a historical dataset generated under a single control arm. We propose novel data integration methods that linearly integrate base policy value estimators constructed based on the experimental and historical data, with weights optimized to minimize the mean square error (MSE) of the resulting combined estimator. We further apply the pessimistic principle to obtain more robust estimators, and extend these developments to sequential decision making. Theoretically, we establish non-asymptotic error bounds for the MSEs of our proposed estimators, and derive their oracle, efficiency and robustness properties across a broad spectrum of reward shift scenarios. Numerical experiments and real-data-based analyses from a ridesharing company demonstrate the superior performance of the proposed estimators.

Read more6/4/2024

0

Posterior Sampling via Autoregressive Generation

Kelly W Zhang (Tianhui), Tiffany (Tianhui), Cai, Hongseok Namkoong, Daniel Russo

Real-world decision-making requires grappling with a perpetual lack of data as environments change; intelligent agents must comprehend uncertainty and actively gather information to resolve it. We propose a new framework for learning bandit algorithms from massive historical data, which we demonstrate in a cold-start recommendation problem. First, we use historical data to pretrain an autoregressive model to predict a sequence of repeated feedback/rewards (e.g., responses to news articles shown to different users over time). In learning to make accurate predictions, the model implicitly learns an informed prior based on rich action features (e.g., article headlines) and how to sharpen beliefs as more rewards are gathered (e.g., clicks as each article is recommended). At decision-time, we autoregressively sample (impute) an imagined sequence of rewards for each action, and choose the action with the largest average imputed reward. Far from a heuristic, our approach is an implementation of Thompson sampling (with a learned prior), a prominent active exploration algorithm. We prove our pretraining loss directly controls online decision-making performance, and we demonstrate our framework on a news recommendation task where we integrate end-to-end fine-tuning of a pretrained language model to process news article headline text to improve performance.

Read more5/31/2024