DAM: A Universal Dual Attention Mechanism for Multimodal Timeseries Cryptocurrency Trend Forecasting

0

Sign in to get full access

Overview

- This paper presents a novel deep learning model called "DAM" (Dual Attention Mechanism) for forecasting cryptocurrency price trends using multimodal time-series data.

- The model combines textual data from crypto-related news articles and social media with traditional financial data to improve prediction accuracy.

- The key innovation is the use of a "dual attention mechanism" that allows the model to dynamically focus on the most relevant features from both textual and numerical data sources.

Plain English Explanation

The goal of this research is to develop a more accurate way to predict the future price movements of cryptocurrencies. Cryptocurrencies are a type of digital currency that have become increasingly popular in recent years, but their prices can be volatile and difficult to forecast.

The researchers propose a new deep learning model called "DAM" that combines two different types of data to make these predictions:

- Textual data from news articles and social media posts related to cryptocurrencies

- Traditional financial data like trading volume and historical prices

The key innovation in the DAM model is the "dual attention mechanism", which allows the model to automatically identify and focus on the most relevant features from both the textual and numerical data sources. This is important because the factors driving cryptocurrency prices can come from a variety of sources, and the relative importance of these factors may change over time.

By fusing these diverse data sources using the dual attention mechanism, the researchers were able to create a more robust and accurate model for forecasting cryptocurrency price trends. This could be useful for investors, traders, and others who need to make informed decisions about the cryptocurrency market.

Technical Explanation

The DAM model proposed in this paper combines multimodal deep learning techniques with a novel "dual attention mechanism" to improve cryptocurrency price trend forecasting.

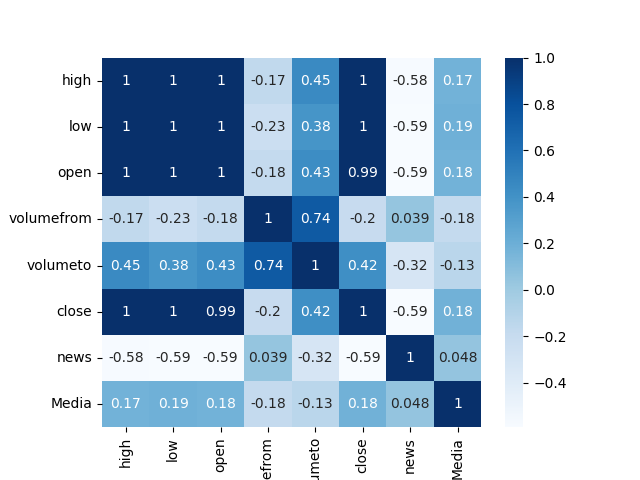

The model takes two main inputs: 1) textual data from news articles and social media related to cryptocurrencies, processed using a CryptoBERT language model, and 2) traditional financial time-series data like historical prices and trading volume.

The dual attention mechanism consists of two parallel attention modules - one focused on the textual data and one on the numerical data. These modules dynamically learn to weigh the relative importance of different features from each modality when making predictions. This allows the model to focus on the most relevant information, whether it comes from the text or the financial data.

The textual attention module uses a transformer-based architecture to capture semantic and contextual relationships in the news/social media data. The numerical attention module uses an LSTM-based network to model temporal dependencies in the financial time-series.

The outputs of these two attention modules are then combined and passed through additional neural network layers to generate the final price trend prediction. The researchers demonstrate the effectiveness of their DAM model through experiments on real-world cryptocurrency datasets, showing consistent improvements over baseline approaches.

Critical Analysis

The DAM model presented in this paper represents a promising advance in the area of multimodal time-series forecasting for cryptocurrencies. The novel dual attention mechanism is a clever way to dynamically fuse textual and numerical data sources, which is an important capability given the complex, multifaceted nature of the cryptocurrency market.

That said, the researchers acknowledge several limitations and areas for future work. For example, they note that their experiments were primarily focused on short-term price trend prediction, and longer-term forecasting may require different modeling approaches. Additionally, the model's performance could potentially be improved by incorporating additional data sources, such as on-chain metrics or macroeconomic indicators related to the cryptocurrency ecosystem.

Another potential issue is the generalizability of the DAM model. While the experiments demonstrate strong results on the datasets tested, it's unclear how well the model would transfer to forecasting prices for different cryptocurrencies or in different market conditions. Further research would be needed to assess the broader applicability of this approach.

Overall, the DAM model represents a valuable contribution to the field of cryptocurrency price forecasting. By blending textual and numerical data using a novel attention-based mechanism, the researchers have developed a more comprehensive and adaptive approach to this challenging predictive task. As the cryptocurrency market continues to evolve, models like DAM will likely play an important role in helping investors, traders, and other stakeholders navigate this complex and dynamic landscape.

Conclusion

This paper introduces the DAM (Dual Attention Mechanism) model, a novel deep learning approach for forecasting cryptocurrency price trends using multimodal time-series data. The key innovation is the use of a dual attention mechanism that allows the model to dynamically focus on the most relevant features from both textual (e.g., news, social media) and numerical (e.g., prices, trading volume) data sources.

Through experiments on real-world cryptocurrency datasets, the researchers demonstrate that the DAM model can outperform baseline forecasting approaches that use either textual or numerical data alone. This suggests that the fusion of diverse data sources, enabled by the dual attention mechanism, can lead to more accurate and robust price predictions.

While the DAM model shows promising results, the researchers also identify several limitations and areas for future work. These include exploring longer-term forecasting horizons, incorporating additional data sources, and assessing the model's generalizability to different cryptocurrencies and market conditions.

Overall, this research represents an important step forward in the field of cryptocurrency price forecasting. By leveraging multimodal deep learning techniques and a novel attention-based architecture, the DAM model provides a more comprehensive and adaptive approach to this challenging predictive task. As the cryptocurrency market continues to evolve, tools like DAM will likely play an increasingly valuable role in helping investors, traders, and other stakeholders navigate this dynamic landscape.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

DAM: A Universal Dual Attention Mechanism for Multimodal Timeseries Cryptocurrency Trend Forecasting

Yihang Fu, Mingyu Zhou, Luyao Zhang

In the distributed systems landscape, Blockchain has catalyzed the rise of cryptocurrencies, merging enhanced security and decentralization with significant investment opportunities. Despite their potential, current research on cryptocurrency trend forecasting often falls short by simplistically merging sentiment data without fully considering the nuanced interplay between financial market dynamics and external sentiment influences. This paper presents a novel Dual Attention Mechanism (DAM) for forecasting cryptocurrency trends using multimodal time-series data. Our approach, which integrates critical cryptocurrency metrics with sentiment data from news and social media analyzed through CryptoBERT, addresses the inherent volatility and prediction challenges in cryptocurrency markets. By combining elements of distributed systems, natural language processing, and financial forecasting, our method outperforms conventional models like LSTM and Transformer by up to 20% in prediction accuracy. This advancement deepens the understanding of distributed systems and has practical implications in financial markets, benefiting stakeholders in cryptocurrency and blockchain technologies. Moreover, our enhanced forecasting approach can significantly support decentralized science (DeSci) by facilitating strategic planning and the efficient adoption of blockchain technologies, improving operational efficiency and financial risk management in the rapidly evolving digital asset domain, thus ensuring optimal resource allocation.

Read more5/3/2024

📈

0

DAM: Towards A Foundation Model for Time Series Forecasting

Luke Darlow, Qiwen Deng, Ahmed Hassan, Martin Asenov, Rajkarn Singh, Artjom Joosen, Adam Barker, Amos Storkey

It is challenging to scale time series forecasting models such that they forecast accurately for multiple distinct domains and datasets, all with potentially different underlying collection procedures (e.g., sample resolution), patterns (e.g., periodicity), and prediction requirements (e.g., reconstruction vs. forecasting). We call this general task universal forecasting. Existing methods usually assume that input data is regularly sampled, and they forecast to pre-determined horizons, resulting in failure to generalise outside of the scope of their training. We propose the DAM - a neural model that takes randomly sampled histories and outputs an adjustable basis composition as a continuous function of time for forecasting to non-fixed horizons. It involves three key components: (1) a flexible approach for using randomly sampled histories from a long-tail distribution, that enables an efficient global perspective of the underlying temporal dynamics while retaining focus on the recent history; (2) a transformer backbone that is trained on these actively sampled histories to produce, as representational output, (3) the basis coefficients of a continuous function of time. We show that a single univariate DAM, trained on 25 time series datasets, either outperformed or closely matched existing SoTA models at multivariate long-term forecasting across 18 datasets, including 8 held-out for zero-shot transfer, even though these models were trained to specialise for each dataset-horizon combination. This single DAM excels at zero-shot transfer and very-long-term forecasting, performs well at imputation, is interpretable via basis function composition and attention, can be tuned for different inference-cost requirements, is robust to missing and irregularly sampled data {by design}.

Read more7/26/2024

✨

0

Causal Feature Engineering of Price Directions of Cryptocurrencies using Dynamic Bayesian Networks

Rasoul Amirzadeh, Asef Nazari, Dhananjay Thiruvady, Mong Shan Ee

Cryptocurrencies have gained popularity across various sectors, especially in finance and investment. The popularity is partly due to their unique specifications originating from blockchain-related characteristics such as privacy, decentralisation, and untraceability. Despite their growing popularity, cryptocurrencies remain a high-risk investment due to their price volatility and uncertainty. The inherent volatility in cryptocurrency prices, coupled with internal cryptocurrency-related factors and external influential global economic factors makes predicting their prices and price movement directions challenging. Nevertheless, the knowledge obtained from predicting the direction of cryptocurrency prices can provide valuable guidance for investors in making informed investment decisions. To address this issue, this paper proposes a dynamic Bayesian network (DBN) approach, which can model complex systems in multivariate settings, to predict the price movement direction of five popular altcoins (cryptocurrencies other than Bitcoin) in the next trading day. The efficacy of the proposed model in predicting cryptocurrency price directions is evaluated from two perspectives. Firstly, our proposed approach is compared to two baseline models, namely an auto-regressive integrated moving average and support vector regression. Secondly, from a feature engineering point of view, the impact of twenty-three different features, grouped into four categories, on the DBN's prediction performance is investigated. The experimental results demonstrate that the DBN significantly outperforms the baseline models. In addition, among the groups of features, technical indicators are found to be the most effective predictors of cryptocurrency price directions.

Read more4/30/2024

0

Review of deep learning models for crypto price prediction: implementation and evaluation

Jingyang Wu, Xinyi Zhang, Fangyixuan Huang, Haochen Zhou, Rohtiash Chandra

There has been much interest in accurate cryptocurrency price forecast models by investors and researchers. Deep Learning models are prominent machine learning techniques that have transformed various fields and have shown potential for finance and economics. Although various deep learning models have been explored for cryptocurrency price forecasting, it is not clear which models are suitable due to high market volatility. In this study, we review the literature about deep learning for cryptocurrency price forecasting and evaluate novel deep learning models for cryptocurrency stock price prediction. Our deep learning models include variants of long short-term memory (LSTM) recurrent neural networks, variants of convolutional neural networks (CNNs), and the Transformer model. We evaluate univariate and multivariate approaches for multi-step ahead predicting of cryptocurrencies close-price. We also carry out volatility analysis on the four cryptocurrencies which reveals significant fluctuations in their prices throughout the COVID-19 pandemic. Additionally, we investigate the prediction accuracy of two scenarios identified by different training sets for the models. First, we use the pre-COVID-19 datasets to model cryptocurrency close-price forecasting during the early period of COVID-19. Secondly, we utilise data from the COVID-19 period to predict prices for 2023 to 2024. Our results show that the convolutional LSTM with a multivariate approach provides the best prediction accuracy in two major experimental settings. Our results also indicate that the multivariate deep learning models exhibit better performance in forecasting four different cryptocurrencies when compared to the univariate models.

Read more6/4/2024