Enhanced LFTSformer: A Novel Long-Term Financial Time Series Prediction Model Using Advanced Feature Engineering and the DS Encoder Informer Architecture

2310.01884

0

0

Abstract

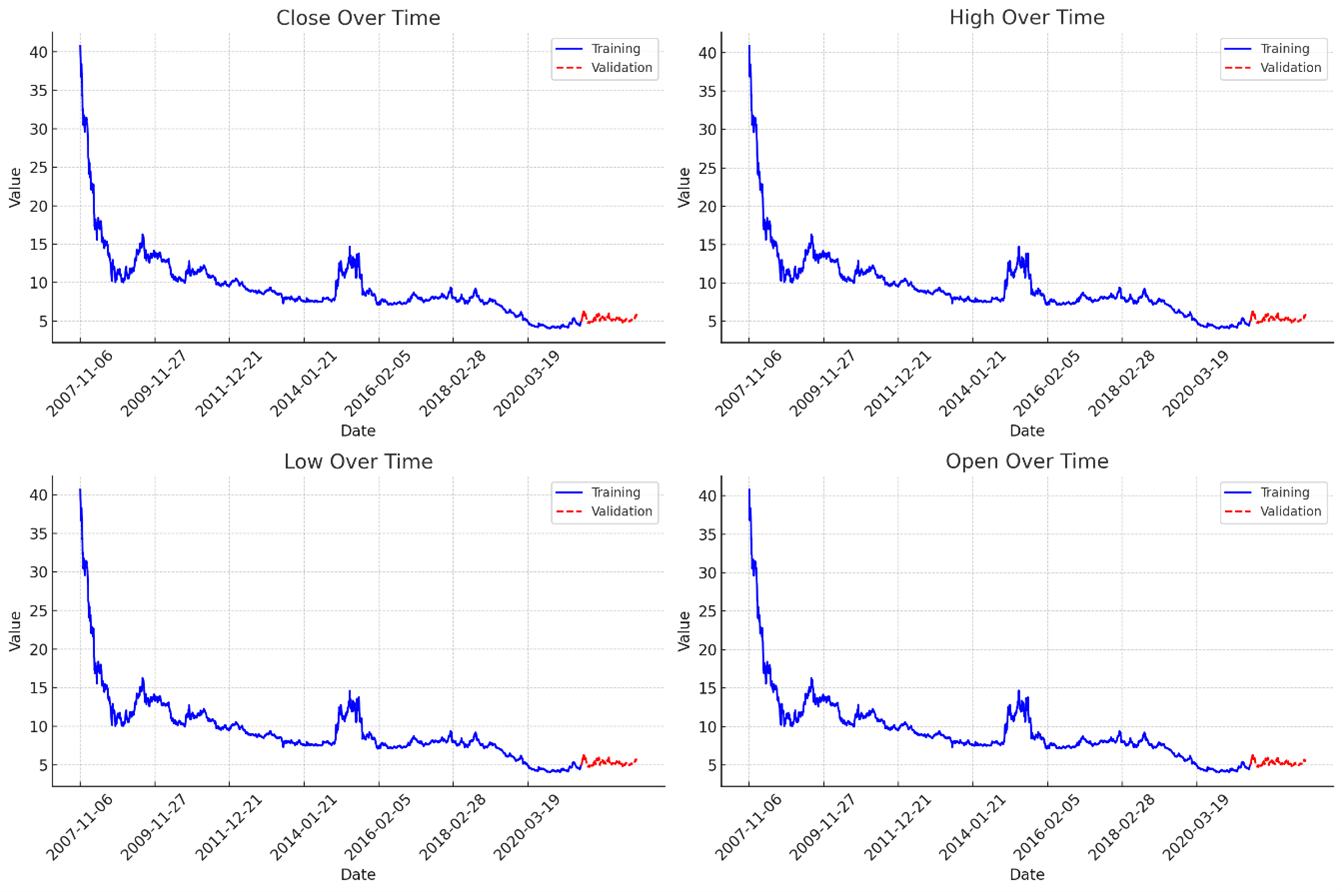

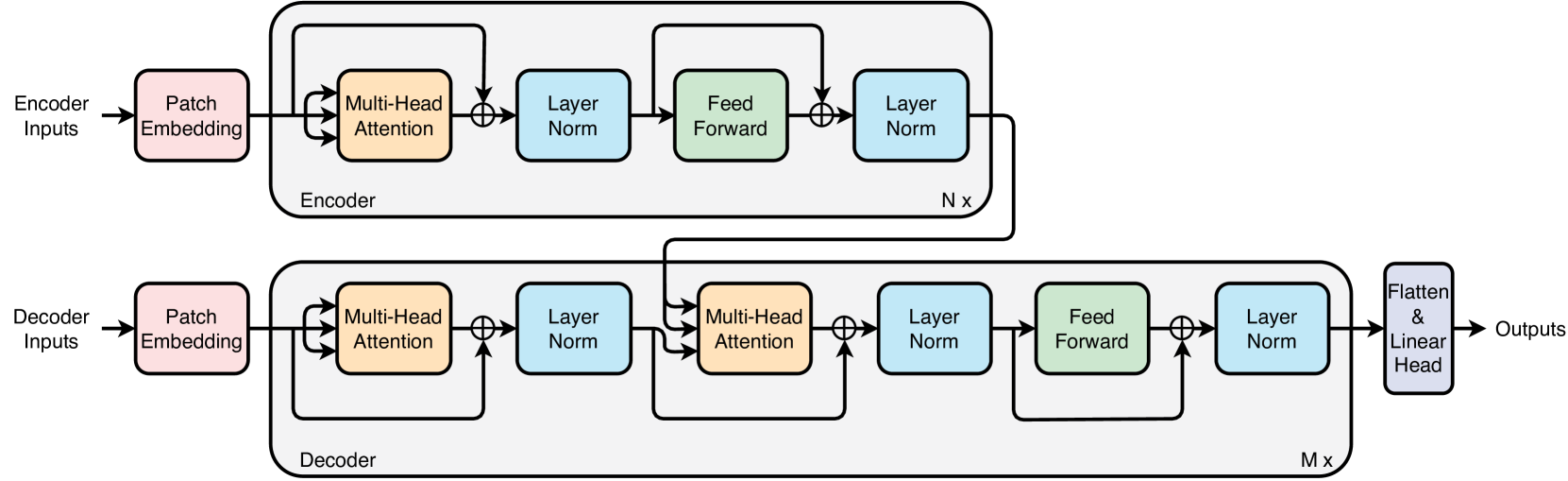

This study presents a groundbreaking model for forecasting long-term financial time series, termed the Enhanced LFTSformer. The model distinguishes itself through several significant innovations: (1) VMD-MIC+FE Feature Engineering: The incorporation of sophisticated feature engineering techniques, specifically through the integration of Variational Mode Decomposition (VMD), Maximal Information Coefficient (MIC), and feature engineering (FE) methods, enables comprehensive perception and extraction of deep-level features from complex and variable financial datasets. (2) DS Encoder Informer: The architecture of the original Informer has been modified by adopting a Stacked Informer structure in the encoder, and an innovative introduction of a multi-head decentralized sparse attention mechanism, referred to as the Distributed Informer. This modification has led to a reduction in the number of attention blocks, thereby enhancing both the training accuracy and speed. (3) GC Enhanced Adam & Dynamic Loss Function: The deployment of a Gradient Clipping-enhanced Adam optimization algorithm and a dynamic loss function represents a pioneering approach within the domain of financial time series prediction. This novel methodology optimizes model performance and adapts more dynamically to evolving data patterns. Systematic experimentation on a range of benchmark stock market datasets demonstrates that the Enhanced LFTSformer outperforms traditional machine learning models and other Informer-based architectures in terms of prediction accuracy, adaptability, and generality. Furthermore, the paper identifies potential avenues for future enhancements, with a particular focus on the identification and quantification of pivotal impacting events and news. This is aimed at further refining the predictive efficacy of the model.

Get summaries of the top AI research delivered straight to your inbox:

Overview

- Proposes an adaptive hybrid model for enhanced stock market predictions

- Combines an improved Variational Mode Decomposition (VMD) algorithm and a Stacked Informer model

- Aims to improve the accuracy and robustness of stock market forecasting

Plain English Explanation

This research paper introduces an adaptive hybrid model for enhancing stock market predictions. The key idea is to combine two powerful techniques: an improved Variational Mode Decomposition (VMD) algorithm and a Stacked Informer model.

The VMD algorithm is used to decompose the complex stock market data into multiple intrinsic mode functions (IMFs). This helps to capture the underlying patterns and dynamics more effectively. The Stacked Informer model, on the other hand, is a deep learning-based forecasting technique that can capture long-range dependencies in time series data.

By integrating these two approaches, the researchers aim to create a more accurate and robust stock market prediction system. The hybrid model takes advantage of the strengths of both methods, allowing it to better handle the non-stationary and non-linear nature of stock market data.

Technical Explanation

The proposed approach, called the Adaptive Hybrid Model (AHM), consists of two main components:

-

Improved VMD Algorithm: The researchers have introduced enhancements to the standard VMD algorithm to make it more suitable for stock market data. These include modifications to the mode update step and the parameter initialization process.

-

Stacked Informer Model: The Stacked Informer is a deep learning-based forecasting model that combines multiple Informer modules, each with a different attention mechanism. This allows the model to capture both short-term and long-term dependencies in the stock market time series.

The AHM integrates these two components by first using the improved VMD algorithm to decompose the stock market data into multiple IMFs. These IMFs are then fed into the Stacked Informer model for forecasting. The model is trained end-to-end, allowing it to learn the optimal way to combine the information from the different IMFs.

The researchers have evaluated the AHM on several stock market datasets and compared its performance to various benchmark models, including deep learning-based techniques and traditional econometric approaches. The results demonstrate the superior performance of the AHM in terms of prediction accuracy and robustness.

Critical Analysis

The paper provides a comprehensive and well-designed study on the proposed Adaptive Hybrid Model. The researchers have made a strong case for the benefits of combining the improved VMD algorithm and the Stacked Informer model, which is supported by the experimental results.

However, the paper does not address the potential limitations of the approach. For example, the computational complexity of the model and its sensitivity to parameter tuning could be areas for further investigation. Additionally, the generalization of the AHM to other financial time series or its performance in real-world trading scenarios could be explored in future research.

Overall, the paper presents a promising and novel approach to stock market forecasting, which could have significant implications for financial decision-making and investment strategies. The integration of advanced signal processing and deep learning techniques is an exciting direction in the field of time series analysis and forecasting.

Conclusion

The Adaptive Hybrid Model proposed in this paper offers a compelling solution for enhancing stock market predictions. By combining the strengths of the improved VMD algorithm and the Stacked Informer model, the researchers have developed a robust and accurate forecasting system that can better capture the complex dynamics of the stock market.

The findings of this study have the potential to significantly impact the field of financial time series analysis and provide valuable insights for investors, traders, and policymakers. The proposed approach could be further explored and extended to other financial and economic forecasting domains, contributing to the ongoing advancements in the field of time series analysis and prediction.

Related Papers

Advancing Long-Term Multi-Energy Load Forecasting with Patchformer: A Patch and Transformer-Based Approach

Qiuyi Hong, Fanlin Meng, Felipe Maldonado

0

0

In the context of increasing demands for long-term multi-energy load forecasting in real-world applications, this paper introduces Patchformer, a novel model that integrates patch embedding with encoder-decoder Transformer-based architectures. To address the limitation in existing Transformer-based models, which struggle with intricate temporal patterns in long-term forecasting, Patchformer employs patch embedding, which predicts multivariate time-series data by separating it into multiple univariate data and segmenting each of them into multiple patches. This method effectively enhances the model's ability to capture local and global semantic dependencies. The numerical analysis shows that the Patchformer obtains overall better prediction accuracy in both multivariate and univariate long-term forecasting on the novel Multi-Energy dataset and other benchmark datasets. In addition, the positive effect of the interdependence among energy-related products on the performance of long-term time-series forecasting across Patchformer and other compared models is discovered, and the superiority of the Patchformer against other models is also demonstrated, which presents a significant advancement in handling the interdependence and complexities of long-term multi-energy forecasting. Lastly, Patchformer is illustrated as the only model that follows the positive correlation between model performance and the length of the past sequence, which states its ability to capture long-range past local semantic information.

4/17/2024

🤖

An End-to-End Structure with Novel Position Mechanism and Improved EMD for Stock Forecasting

Chufeng Li, Jianyong Chen

0

0

As a branch of time series forecasting, stock movement forecasting is one of the challenging problems for investors and researchers. Since Transformer was introduced to analyze financial data, many researchers have dedicated themselves to forecasting stock movement using Transformer or attention mechanisms. However, existing research mostly focuses on individual stock information but ignores stock market information and high noise in stock data. In this paper, we propose a novel method using the attention mechanism in which both stock market information and individual stock information are considered. Meanwhile, we propose a novel EMD-based algorithm for reducing short-term noise in stock data. Two randomly selected exchange-traded funds (ETFs) spanning over ten years from US stock markets are used to demonstrate the superior performance of the proposed attention-based method. The experimental analysis demonstrates that the proposed attention-based method significantly outperforms other state-of-the-art baselines. Code is available at https://github.com/DurandalLee/ACEFormer.

4/12/2024

📈

A decoder-only foundation model for time-series forecasting

Abhimanyu Das, Weihao Kong, Rajat Sen, Yichen Zhou

0

0

Motivated by recent advances in large language models for Natural Language Processing (NLP), we design a time-series foundation model for forecasting whose out-of-the-box zero-shot performance on a variety of public datasets comes close to the accuracy of state-of-the-art supervised forecasting models for each individual dataset. Our model is based on pretraining a patched-decoder style attention model on a large time-series corpus, and can work well across different forecasting history lengths, prediction lengths and temporal granularities.

4/19/2024

Longitudinal Targeted Minimum Loss-based Estimation with Temporal-Difference Heterogeneous Transformer

Toru Shirakawa, Yi Li, Yulun Wu, Sky Qiu, Yuxuan Li, Mingduo Zhao, Hiroyasu Iso, Mark van der Laan

0

0

We propose Deep Longitudinal Targeted Minimum Loss-based Estimation (Deep LTMLE), a novel approach to estimate the counterfactual mean of outcome under dynamic treatment policies in longitudinal problem settings. Our approach utilizes a transformer architecture with heterogeneous type embedding trained using temporal-difference learning. After obtaining an initial estimate using the transformer, following the targeted minimum loss-based likelihood estimation (TMLE) framework, we statistically corrected for the bias commonly associated with machine learning algorithms. Furthermore, our method also facilitates statistical inference by enabling the provision of 95% confidence intervals grounded in asymptotic statistical theory. Simulation results demonstrate our method's superior performance over existing approaches, particularly in complex, long time-horizon scenarios. It remains effective in small-sample, short-duration contexts, matching the performance of asymptotically efficient estimators. To demonstrate our method in practice, we applied our method to estimate counterfactual mean outcomes for standard versus intensive blood pressure management strategies in a real-world cardiovascular epidemiology cohort study.

4/9/2024