Integrating Mamba and Transformer for Long-Short Range Time Series Forecasting

0

🔎

Sign in to get full access

Overview

- Time series forecasting is an important problem with applications in various fields like weather, finance, and scientific simulations.

- Transformers have proven effective in capturing dependencies, but their quadratic complexity limits their use in long-range time series forecasting.

- Recent progress on state space models (SSMs) like Mamba have shown promise in modeling long-range dependencies due to their subquadratic complexity.

- This paper introduces a hybrid framework called Mambaformer that combines Mamba for long-range dependency and Transformer for short-range dependency to address long-short range forecasting.

Plain English Explanation

Time series forecasting is the task of predicting future values based on past data. This is crucial in areas like weather forecasting, stock market analysis, and scientific simulations. Transformers, a type of machine learning model, have shown great success in capturing dependencies in data. However, the way they process information, known as the attention mechanism, has a significant drawback – it scales quadratically with the length of the input. This makes it difficult to use transformers for forecasting long-range time series, where the data can be very extensive.

On the other hand, recent advancements in state space models (SSMs), like the Mamba model, have demonstrated impressive performance in modeling long-range dependencies. This is because SSMs have a more efficient, subquadratic computational complexity, allowing them to handle long sequences of data.

The researchers in this paper propose a hybrid approach called Mambaformer that combines the strengths of Mamba and Transformer models. Mambaformer uses Mamba to capture the long-range dependencies in the time series data, while the Transformer component focuses on the short-range relationships. By integrating these two complementary models, the researchers aim to achieve better performance in long-short range time series forecasting tasks.

Technical Explanation

The paper introduces a hybrid framework called Mambaformer that combines the Mamba state space model and the Transformer architecture for long-short range time series forecasting.

Transformers have proven effective in capturing dependencies, but their quadratic complexity of the attention mechanism prevents their widespread adoption in long-range time series forecasting tasks. Recent progress on state space models (SSMs), such as Mamba, have shown impressive performance in modeling long-range dependencies due to their subquadratic complexity.

The researchers investigate different hybrid architectures to combine the Mamba layer and the attention layer of the Transformer for long-short range time series forecasting. The comparative study shows that the Mambaformer family can outperform both Mamba and Transformer models in long-short range time series forecasting problems.

Critical Analysis

The paper presents a promising approach to addressing the limitations of Transformers in long-range time series forecasting by leveraging the strengths of Mamba, a state space model. The authors provide a thorough comparative analysis and demonstrate the effectiveness of the Mambaformer family of models.

However, the paper does not discuss potential limitations or caveats of the proposed approach. For example, it would be valuable to understand the computational trade-offs of the hybrid architecture compared to the individual Mamba and Transformer models, as well as the sensitivity of the Mambaformer to hyperparameter tuning or dataset characteristics.

Additionally, the paper would benefit from a more in-depth discussion of the specific mechanisms by which the Mamba and Transformer components interact and complement each other in the hybrid framework. A deeper exploration of the insights gained from this combination could further strengthen the contributions of the research.

Conclusion

This paper presents a novel hybrid framework called Mambaformer that combines the Mamba state space model and the Transformer architecture to address the limitations of Transformers in long-range time series forecasting. By leveraging the strengths of Mamba in modeling long-range dependencies and the Transformer in capturing short-range relationships, the Mambaformer family of models demonstrates improved performance over standalone Mamba and Transformer models.

The proposed approach holds promise for advancing the field of time series forecasting, with potential applications in various domains that rely on accurate long-short range predictions, such as weather forecasting, financial analysis, and scientific simulations. Further research could explore the scalability, robustness, and practical implications of the Mambaformer framework, as well as its adaptability to different types of time series data and forecasting tasks.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

🔎

0

Integrating Mamba and Transformer for Long-Short Range Time Series Forecasting

Xiongxiao Xu, Canyu Chen, Yueqing Liang, Baixiang Huang, Guangji Bai, Liang Zhao, Kai Shu

Despite significant progress in time series forecasting, existing forecasters often overlook the heterogeneity between long-range and short-range time series, leading to performance degradation in practical applications. In this work, we highlight the need of distinct objectives tailored to different ranges. We point out that time series can be decomposed into global patterns and local variations, which should be addressed separately in long- and short-range time series. To meet the objectives, we propose a multi-scale hybrid Mamba-Transformer experts model State Space Transformer (SST). SST leverages Mamba as an expert to extract global patterns in coarse-grained long-range time series, and Local Window Transformer (LWT), the other expert to focus on capturing local variations in fine-grained short-range time series. With an input-dependent mechanism, State Space Model (SSM)-based Mamba is able to selectively retain long-term patterns and filter out fluctuations, while LWT employs a local window to enhance locality-awareness capability, thus effectively capturing local variations. To adaptively integrate the global patterns and local variations, a long-short router dynamically adjusts contributions of the two experts. SST achieves superior performance with scaling linearly $O(L)$ on time series length $L$. The comprehensive experiments demonstrate the SST can achieve SOTA results in long-short range time series forecasting while maintaining low memory footprint and computational cost. The code of SST is available at https://github.com/XiongxiaoXu/SST.

Read more8/23/2024

0

New!Integration of Mamba and Transformer -- MAT for Long-Short Range Time Series Forecasting with Application to Weather Dynamics

Wenqing Zhang, Junming Huang, Ruotong Wang, Changsong Wei, Wenqian Huang, Yuxin Qiao

Long-short range time series forecasting is essential for predicting future trends and patterns over extended periods. While deep learning models such as Transformers have made significant strides in advancing time series forecasting, they often encounter difficulties in capturing long-term dependencies and effectively managing sparse semantic features. The state-space model, Mamba, addresses these issues through its adept handling of selective input and parallel computing, striking a balance between computational efficiency and prediction accuracy. This article examines the advantages and disadvantages of both Mamba and Transformer models, and introduces a combined approach, MAT, which leverages the strengths of each model to capture unique long-short range dependencies and inherent evolutionary patterns in multivariate time series. Specifically, MAT harnesses the long-range dependency capabilities of Mamba and the short-range characteristics of Transformers. Experimental results on benchmark weather datasets demonstrate that MAT outperforms existing comparable methods in terms of prediction accuracy, scalability, and memory efficiency.

Read more9/16/2024

0

Bi-Mamba+: Bidirectional Mamba for Time Series Forecasting

Aobo Liang, Xingguo Jiang, Yan Sun, Xiaohou Shi, Ke Li

Long-term time series forecasting (LTSF) provides longer insights into future trends and patterns. Over the past few years, deep learning models especially Transformers have achieved advanced performance in LTSF tasks. However, LTSF faces inherent challenges such as long-term dependencies capturing and sparse semantic characteristics. Recently, a new state space model (SSM) named Mamba is proposed. With the selective capability on input data and the hardware-aware parallel computing algorithm, Mamba has shown great potential in balancing predicting performance and computational efficiency compared to Transformers. To enhance Mamba's ability to preserve historical information in a longer range, we design a novel Mamba+ block by adding a forget gate inside Mamba to selectively combine the new features with the historical features in a complementary manner. Furthermore, we apply Mamba+ both forward and backward and propose Bi-Mamba+, aiming to promote the model's ability to capture interactions among time series elements. Additionally, multivariate time series data in different scenarios may exhibit varying emphasis on intra- or inter-series dependencies. Therefore, we propose a series-relation-aware decider that controls the utilization of channel-independent or channel-mixing tokenization strategy for specific datasets. Extensive experiments on 8 real-world datasets show that our model achieves more accurate predictions compared with state-of-the-art methods.

Read more6/28/2024

0

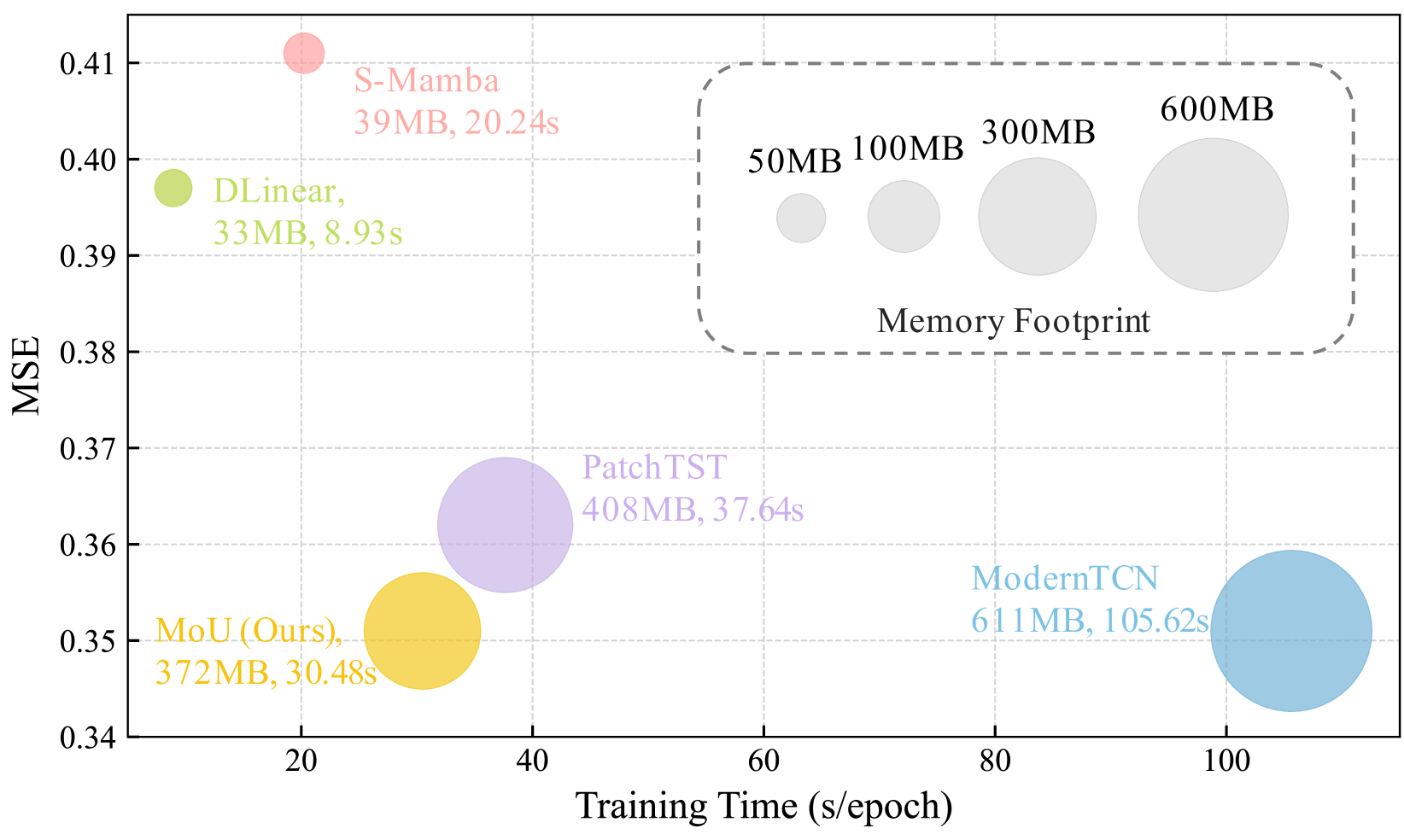

Mamba or Transformer for Time Series Forecasting? Mixture of Universals (MoU) Is All You Need

Sijia Peng, Yun Xiong, Yangyong Zhu, Zhiqiang Shen

Time series forecasting requires balancing short-term and long-term dependencies for accurate predictions. Existing methods mainly focus on long-term dependency modeling, neglecting the complexities of short-term dynamics, which may hinder performance. Transformers are superior in modeling long-term dependencies but are criticized for their quadratic computational cost. Mamba provides a near-linear alternative but is reported less effective in time series longterm forecasting due to potential information loss. Current architectures fall short in offering both high efficiency and strong performance for long-term dependency modeling. To address these challenges, we introduce Mixture of Universals (MoU), a versatile model to capture both short-term and long-term dependencies for enhancing performance in time series forecasting. MoU is composed of two novel designs: Mixture of Feature Extractors (MoF), an adaptive method designed to improve time series patch representations for short-term dependency, and Mixture of Architectures (MoA), which hierarchically integrates Mamba, FeedForward, Convolution, and Self-Attention architectures in a specialized order to model long-term dependency from a hybrid perspective. The proposed approach achieves state-of-the-art performance while maintaining relatively low computational costs. Extensive experiments on seven real-world datasets demonstrate the superiority of MoU. Code is available at https://github.com/lunaaa95/mou/.

Read more8/29/2024