Time Series Data Augmentation as an Imbalanced Learning Problem

0

Sign in to get full access

Overview

- Time series data augmentation is explored as an approach to address imbalanced learning problems in forecasting tasks.

- The research investigates using synthetic data generation techniques to address class imbalance in time series forecasting.

- Experiments are conducted to evaluate the effectiveness of data augmentation for improving forecasting performance on imbalanced datasets.

- The paper proposes leveraging imbalanced-domain learning strategies to enhance time series forecasting.

Plain English Explanation

Time series forecasting is an important task in many fields, but can be challenging when the available data is imbalanced - meaning there is an uneven distribution of the different classes or patterns you are trying to predict. This can lead to poor forecasting performance, as the model may struggle to learn from the underrepresented classes.

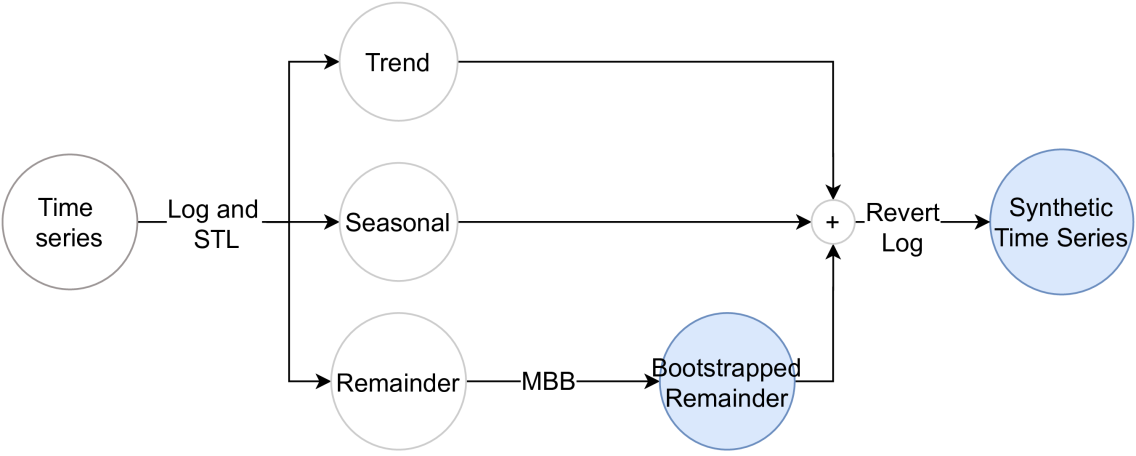

The researchers in this paper explored using data augmentation techniques as a way to address this imbalance problem. Data augmentation involves generating synthetic data that mimics the real data, in order to create a more balanced dataset for training the forecasting model.

By treating the time series forecasting problem as an "imbalanced learning" task, the researchers were able to leverage specialized techniques from that field to enhance their data augmentation approach. This included using generative adversarial networks (GANs) to create realistic synthetic time series data.

The experiments showed that this data augmentation strategy can significantly improve forecasting performance, especially on datasets with severe class imbalances. The synthetic data helps the model learn the patterns in the underrepresented classes better, leading to more accurate and robust forecasts.

Technical Explanation

The paper frames time series forecasting as an imbalanced learning problem, where certain patterns or classes of data are underrepresented in the training set. To address this, the researchers propose using data augmentation techniques to generate synthetic time series data and balance the dataset.

They evaluate several data augmentation approaches, including generative adversarial networks (GANs) and time series-specific augmentation methods like time warping and noise injection. These synthetic samples are then combined with the original training data to train time series forecasting models.

The experiments are conducted on both simulated and real-world time series datasets, with varying degrees of class imbalance. The forecasting models used include both traditional time series methods as well as modern deep learning architectures.

The results demonstrate that data augmentation can significantly improve forecasting performance, especially on highly imbalanced datasets. The synthetic data helps the models better learn the patterns in the underrepresented classes, leading to more accurate and robust predictions.

The paper also investigates using imbalanced-domain learning strategies, which explicitly account for the class distribution during training. This is shown to further enhance the benefits of data augmentation for time series forecasting.

Critical Analysis

The paper provides a compelling approach to addressing class imbalance in time series forecasting through data augmentation. The experiments are well-designed and the results are promising, showing the potential of this technique to improve forecasting in real-world applications with imbalanced data.

However, the paper does not delve deep into the limitations and potential drawbacks of the proposed approach. For example, it does not discuss the computational overhead or training time required for the data augmentation and imbalanced-domain learning techniques, which could be a practical concern for some use cases.

Additionally, the paper only evaluates the method on a limited set of datasets and forecasting models. Further research would be needed to assess the generalizability of the findings and understand how the approach performs across a wider range of time series forecasting problems and architectures.

It would also be valuable to explore the robustness of the augmented data, and whether the synthetic samples introduce any biases or artifacts that could negatively impact the forecasting performance in real-world deployment.

Overall, the paper presents a promising direction for addressing imbalanced learning in time series forecasting, but additional research is needed to fully understand the strengths, limitations, and practical considerations of this data augmentation approach.

Conclusion

This paper investigates the use of data augmentation as a means to address class imbalance in time series forecasting tasks. By treating the problem as an imbalanced learning challenge, the researchers were able to leverage specialized techniques from that field to enhance their data augmentation strategy.

The experiments demonstrate that generating synthetic time series data can significantly improve forecasting performance, especially on datasets with severe class imbalances. The synthetic samples help the models better learn the patterns in the underrepresented classes, leading to more accurate and robust predictions.

The findings suggest that data augmentation could be a valuable tool for improving the reliability and applicability of time series forecasting models in real-world scenarios with imbalanced data. Further research is needed to fully understand the limitations and practical considerations of this approach, but the paper provides a strong foundation for future work in this direction.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Time Series Data Augmentation as an Imbalanced Learning Problem

Vitor Cerqueira, Nuno Moniz, Ricardo In'acio, Carlos Soares

Recent state-of-the-art forecasting methods are trained on collections of time series. These methods, often referred to as global models, can capture common patterns in different time series to improve their generalization performance. However, they require large amounts of data that might not be readily available. Besides this, global models sometimes fail to capture relevant patterns unique to a particular time series. In these cases, data augmentation can be useful to increase the sample size of time series datasets. The main contribution of this work is a novel method for generating univariate time series synthetic samples. Our approach stems from the insight that the observations concerning a particular time series of interest represent only a small fraction of all observations. In this context, we frame the problem of training a forecasting model as an imbalanced learning task. Oversampling strategies are popular approaches used to deal with the imbalance problem in machine learning. We use these techniques to create synthetic time series observations and improve the accuracy of forecasting models. We carried out experiments using 7 different databases that contain a total of 5502 univariate time series. We found that the proposed solution outperforms both a global and a local model, thus providing a better trade-off between these two approaches.

Read more4/30/2024

0

Data Augmentation for Multivariate Time Series Classification: An Experimental Study

Romain Ilbert, Thai V. Hoang, Zonghua Zhang

Our study investigates the impact of data augmentation on the performance of multivariate time series models, focusing on datasets from the UCR archive. Despite the limited size of these datasets, we achieved classification accuracy improvements in 10 out of 13 datasets using the Rocket and InceptionTime models. This highlights the essential role of sufficient data in training effective models, paralleling the advancements seen in computer vision. Our work delves into adapting and applying existing methods in innovative ways to the domain of multivariate time series classification. Our comprehensive exploration of these techniques sets a new standard for addressing data scarcity in time series analysis, emphasizing that diverse augmentation strategies are crucial for unlocking the potential of both traditional and deep learning models. Moreover, by meticulously analyzing and applying a variety of augmentation techniques, we demonstrate that strategic data enrichment can enhance model accuracy. This not only establishes a benchmark for future research in time series analysis but also underscores the importance of adopting varied augmentation approaches to improve model performance in the face of limited data availability.

Read more6/11/2024

0

On-the-fly Data Augmentation for Forecasting with Deep Learning

Vitor Cerqueira, Mois'es Santos, Yassine Baghoussi, Carlos Soares

Deep learning approaches are increasingly used to tackle forecasting tasks. A key factor in the successful application of these methods is a large enough training sample size, which is not always available. In these scenarios, synthetic data generation techniques are usually applied to augment the dataset. Data augmentation is typically applied before fitting a model. However, these approaches create a single augmented dataset, potentially limiting their effectiveness. This work introduces OnDAT (On-the-fly Data Augmentation for Time series) to address this issue by applying data augmentation during training and validation. Contrary to traditional methods that create a single, static augmented dataset beforehand, OnDAT performs augmentation on-the-fly. By generating a new augmented dataset on each iteration, the model is exposed to a constantly changing augmented data variations. We hypothesize this process enables a better exploration of the data space, which reduces the potential for overfitting and improves forecasting performance. We validated the proposed approach using a state-of-the-art deep learning forecasting method and 8 benchmark datasets containing a total of 75797 time series. The experiments suggest that OnDAT leads to better forecasting performance than a strategy that applies data augmentation before training as well as a strategy that does not involve data augmentation. The method and experiments are publicly available.

Read more4/29/2024

0

Guidelines for Augmentation Selection in Contrastive Learning for Time Series Classification

Ziyu Liu, Azadeh Alavi, Minyi Li, Xiang Zhang

Self-supervised contrastive learning has become a key technique in deep learning, particularly in time series analysis, due to its ability to learn meaningful representations without explicit supervision. Augmentation is a critical component in contrastive learning, where different augmentations can dramatically impact performance, sometimes influencing accuracy by over 30%. However, the selection of augmentations is predominantly empirical which can be suboptimal, or grid searching that is time-consuming. In this paper, we establish a principled framework for selecting augmentations based on dataset characteristics such as trend and seasonality. Specifically, we construct 12 synthetic datasets incorporating trend, seasonality, and integration weights. We then evaluate the effectiveness of 8 different augmentations across these synthetic datasets, thereby inducing generalizable associations between time series characteristics and augmentation efficiency. Additionally, we evaluated the induced associations across 6 real-world datasets encompassing domains such as activity recognition, disease diagnosis, traffic monitoring, electricity usage, mechanical fault prognosis, and finance. These real-world datasets are diverse, covering a range from 1 to 12 channels, 2 to 10 classes, sequence lengths of 14 to 1280, and data frequencies from 250 Hz to daily intervals. The experimental results show that our proposed trend-seasonality-based augmentation recommendation algorithm can accurately identify the effective augmentations for a given time series dataset, achieving an average Recall@3 of 0.667, outperforming baselines. Our work provides guidance for studies employing contrastive learning in time series analysis, with wide-ranging applications. All the code, datasets, and analysis results will be released at https://github.com/DL4mHealth/TS-Contrastive-Augmentation-Recommendation.

Read more7/15/2024