A Tutorial on Doubly Robust Learning for Causal Inference

2406.00853

0

0

Abstract

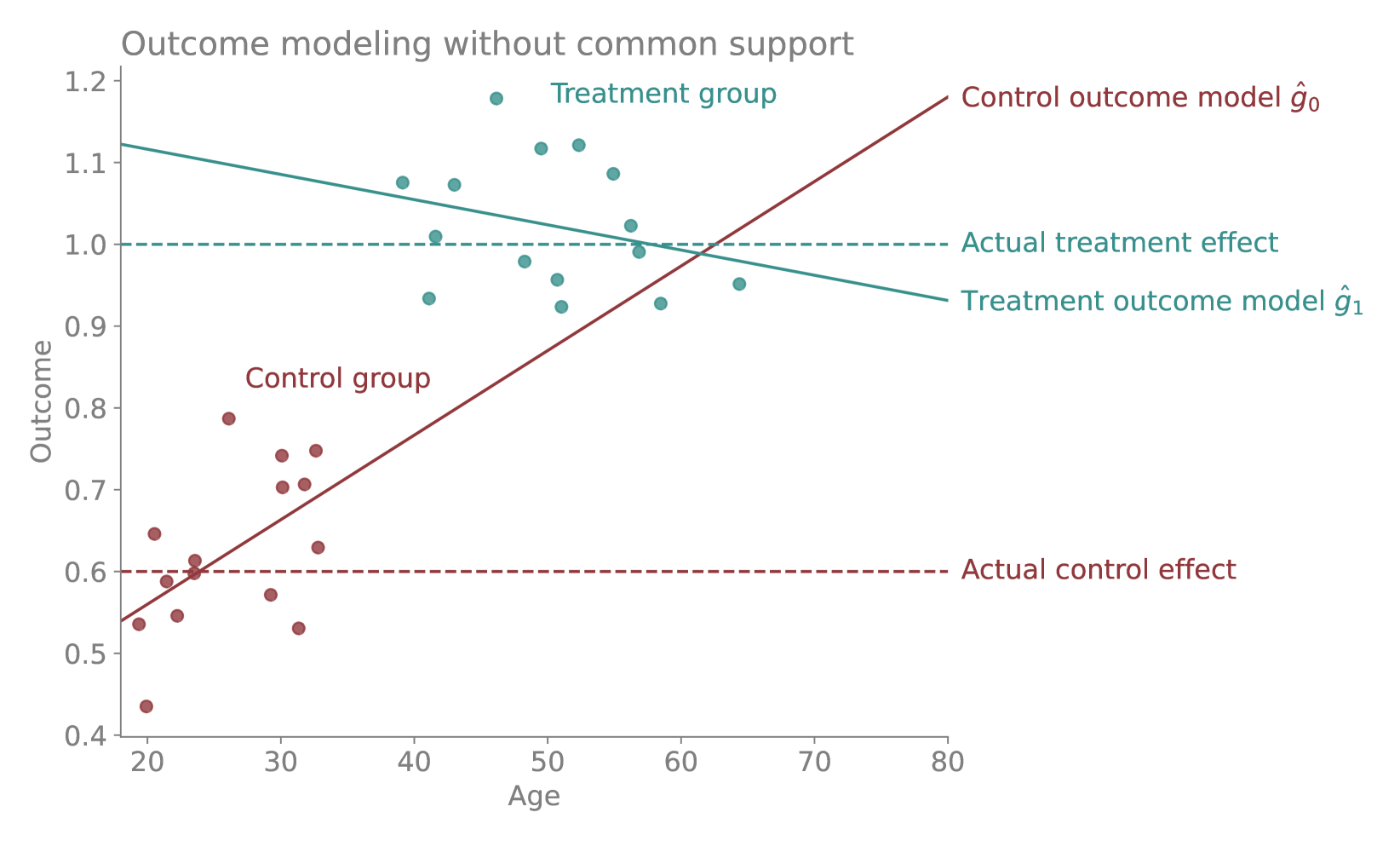

Doubly robust learning offers a robust framework for causal inference from observational data by integrating propensity score and outcome modeling. Despite its theoretical appeal, practical adoption remains limited due to perceived complexity and inaccessible software. This tutorial aims to demystify doubly robust methods and demonstrate their application using the EconML package. We provide an introduction to causal inference, discuss the principles of outcome modeling and propensity scores, and illustrate the doubly robust approach through simulated case studies. By simplifying the methodology and offering practical coding examples, we intend to make doubly robust learning accessible to researchers and practitioners in data science and statistics.

Create account to get full access

Overview

• This paper provides a tutorial on Doubly Robust Learning for Causal Inference. • It explains the concept of doubly robust estimation, which combines two models to achieve unbiased causal effect estimates even if one of the models is misspecified. • The paper covers the theoretical foundations, practical implementation, and applications of doubly robust learning in the context of causal inference.

Plain English Explanation

Causal inference is the process of determining the cause-and-effect relationships between different factors. This is an important task in many fields, from medicine to social science. However, it can be challenging to establish causality, especially when dealing with observational data where the researcher cannot control all the variables.

Doubly robust learning is a statistical technique that can help overcome this challenge. It uses two separate models to estimate the causal effect of a factor on an outcome. Even if one of the models is not entirely accurate, the final estimate will still be unbiased as long as the other model is correct. This makes the technique more robust and reliable than relying on a single model.

The paper explains the mathematical principles behind doubly robust learning and provides guidance on how to implement it in practice. It also discusses various applications of this approach, such as causal attribution and causal modeling with latent factors. By understanding and applying doubly robust learning, researchers can obtain more reliable estimates of causal effects, which can lead to better-informed decisions and policies.

Technical Explanation

The paper begins by introducing the concept of causal inference and the challenges involved in establishing causal relationships from observational data. It then explains the doubly robust estimation approach, which combines two models: a propensity score model that predicts the likelihood of treatment assignment, and an outcome regression model that predicts the outcome variable.

The authors provide a detailed mathematical formulation of the doubly robust estimator, including the assumptions and properties that ensure its unbiasedness. They also discuss practical considerations, such as the choice of model types (e.g., parametric, semiparametric, or nonparametric) and the impact of model misspecification.

The paper then explores several applications of doubly robust learning, including causal attribution, where the goal is to quantify the contribution of different factors to an observed outcome, and causal modeling with latent factors, where the causal relationships are influenced by unobserved variables.

Throughout the technical explanation, the authors provide illustrative examples, simulation studies, and references to relevant literature to help readers understand the concepts and their implementation.

Critical Analysis

The paper presents a comprehensive tutorial on doubly robust learning for causal inference, covering both the theoretical foundations and practical applications. The authors have done an excellent job of explaining the key principles and highlighting the advantages of this approach over traditional causal inference methods.

One potential limitation of the paper is that it does not delve into the specific challenges and considerations for implementing doubly robust learning in real-world, high-dimensional, or complex data scenarios. While the authors mention the impact of model misspecification, a more in-depth discussion of model selection, regularization, and dealing with large feature spaces could be beneficial for readers looking to apply these techniques in their own research or applications.

Additionally, the paper does not extensively cover the limitations or potential drawbacks of doubly robust learning. For example, it would be helpful to discuss the sensitivity of the method to violations of the underlying assumptions, the challenges in selecting appropriate propensity score and outcome regression models, and the computational overhead compared to simpler causal inference approaches.

Overall, the paper provides a solid foundation for understanding doubly robust learning for causal inference, and the authors have done a commendable job of presenting the technical details in an accessible and engaging manner. However, readers may benefit from additional resources or further research to address the practical considerations and limitations of this approach.

Conclusion

This paper offers a comprehensive tutorial on doubly robust learning for causal inference. It explains the key concepts, mathematical foundations, and practical applications of this powerful technique, which combines two models to provide unbiased causal effect estimates even when one of the models is misspecified.

By understanding and applying doubly robust learning, researchers and practitioners in various fields can obtain more reliable estimates of causal relationships, leading to better-informed decisions and policies. The paper's clear explanations and illustrative examples make it a valuable resource for those interested in advancing their understanding and application of causal inference methods.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

Doubly Robust Inference in Causal Latent Factor Models

Alberto Abadie, Anish Agarwal, Raaz Dwivedi, Abhin Shah

0

0

This article introduces a new estimator of average treatment effects under unobserved confounding in modern data-rich environments featuring large numbers of units and outcomes. The proposed estimator is doubly robust, combining outcome imputation, inverse probability weighting, and a novel cross-fitting procedure for matrix completion. We derive finite-sample and asymptotic guarantees, and show that the error of the new estimator converges to a mean-zero Gaussian distribution at a parametric rate. Simulation results demonstrate the practical relevance of the formal properties of the estimators analyzed in this article.

4/16/2024

🌐

Graph Machine Learning based Doubly Robust Estimator for Network Causal Effects

Seyedeh Baharan Khatami, Harsh Parikh, Haowei Chen, Sudeepa Roy, Babak Salimi

0

0

We address the challenge of inferring causal effects in social network data. This results in challenges due to interference -- where a unit's outcome is affected by neighbors' treatments -- and network-induced confounding factors. While there is extensive literature focusing on estimating causal effects in social network setups, a majority of them make prior assumptions about the form of network-induced confounding mechanisms. Such strong assumptions are rarely likely to hold especially in high-dimensional networks. We propose a novel methodology that combines graph machine learning approaches with the double machine learning framework to enable accurate and efficient estimation of direct and peer effects using a single observational social network. We demonstrate the semiparametric efficiency of our proposed estimator under mild regularity conditions, allowing for consistent uncertainty quantification. We demonstrate that our method is accurate, robust, and scalable via an extensive simulation study. We use our method to investigate the impact of Self-Help Group participation on financial risk tolerance.

6/4/2024

Estimating Causal Effects with Double Machine Learning -- A Method Evaluation

Jonathan Fuhr, Philipp Berens, Dominik Papies

0

0

The estimation of causal effects with observational data continues to be a very active research area. In recent years, researchers have developed new frameworks which use machine learning to relax classical assumptions necessary for the estimation of causal effects. In this paper, we review one of the most prominent methods - double/debiased machine learning (DML) - and empirically evaluate it by comparing its performance on simulated data relative to more traditional statistical methods, before applying it to real-world data. Our findings indicate that the application of a suitably flexible machine learning algorithm within DML improves the adjustment for various nonlinear confounding relationships. This advantage enables a departure from traditional functional form assumptions typically necessary in causal effect estimation. However, we demonstrate that the method continues to critically depend on standard assumptions about causal structure and identification. When estimating the effects of air pollution on housing prices in our application, we find that DML estimates are consistently larger than estimates of less flexible methods. From our overall results, we provide actionable recommendations for specific choices researchers must make when applying DML in practice.

5/1/2024

Multiply-Robust Causal Change Attribution

Victor Quintas-Martinez, Mohammad Taha Bahadori, Eduardo Santiago, Jeff Mu, Dominik Janzing, David Heckerman

0

0

Comparing two samples of data, we observe a change in the distribution of an outcome variable. In the presence of multiple explanatory variables, how much of the change can be explained by each possible cause? We develop a new estimation strategy that, given a causal model, combines regression and re-weighting methods to quantify the contribution of each causal mechanism. Our proposed methodology is multiply robust, meaning that it still recovers the target parameter under partial misspecification. We prove that our estimator is consistent and asymptotically normal. Moreover, it can be incorporated into existing frameworks for causal attribution, such as Shapley values, which will inherit the consistency and large-sample distribution properties. Our method demonstrates excellent performance in Monte Carlo simulations, and we show its usefulness in an empirical application. Our method is implemented as part of the Python library DoWhy (arXiv:2011.04216, arXiv:2206.06821).

6/4/2024