Orthogonal Bootstrap: Efficient Simulation of Input Uncertainty

0

Sign in to get full access

Overview

- This paper presents a new technique called "Orthogonal Bootstrap" for efficiently simulating input uncertainty in machine learning models.

- The method aims to improve upon standard bootstrap techniques by leveraging the orthogonal structure of the model parameters.

- The authors demonstrate the effectiveness of their approach through experiments on various datasets and models, showing that Orthogonal Bootstrap can provide significant computational savings over traditional methods.

Plain English Explanation

Machine learning models are often trained on data that contains some level of uncertainty or noise. This input uncertainty can have a significant impact on the model's performance and reliability. To address this, researchers commonly use a technique called "bootstrap" to simulate different versions of the input data and analyze the model's behavior.

However, the standard bootstrap approach can be computationally expensive, especially for large or complex models. The paper's key insight is to exploit the parameter-efficient orthogonal finetuning structure of the model parameters to develop a more efficient simulation method, called "Orthogonal Bootstrap."

The basic idea is to decompose the model parameters into a set of orthogonal vectors, which allows the authors to generate new bootstrap samples by simply rotating these vectors. This approach is much faster than the traditional bootstrap, as it avoids the need to retrain the entire model for each simulation.

The authors demonstrate the effectiveness of Orthogonal Bootstrap on a variety of datasets and models, showing that it can provide significant computational savings while maintaining the same level of accuracy as the standard bootstrap. This could be especially useful for online-calibrated conformal prediction or other applications where running many simulations is required.

Technical Explanation

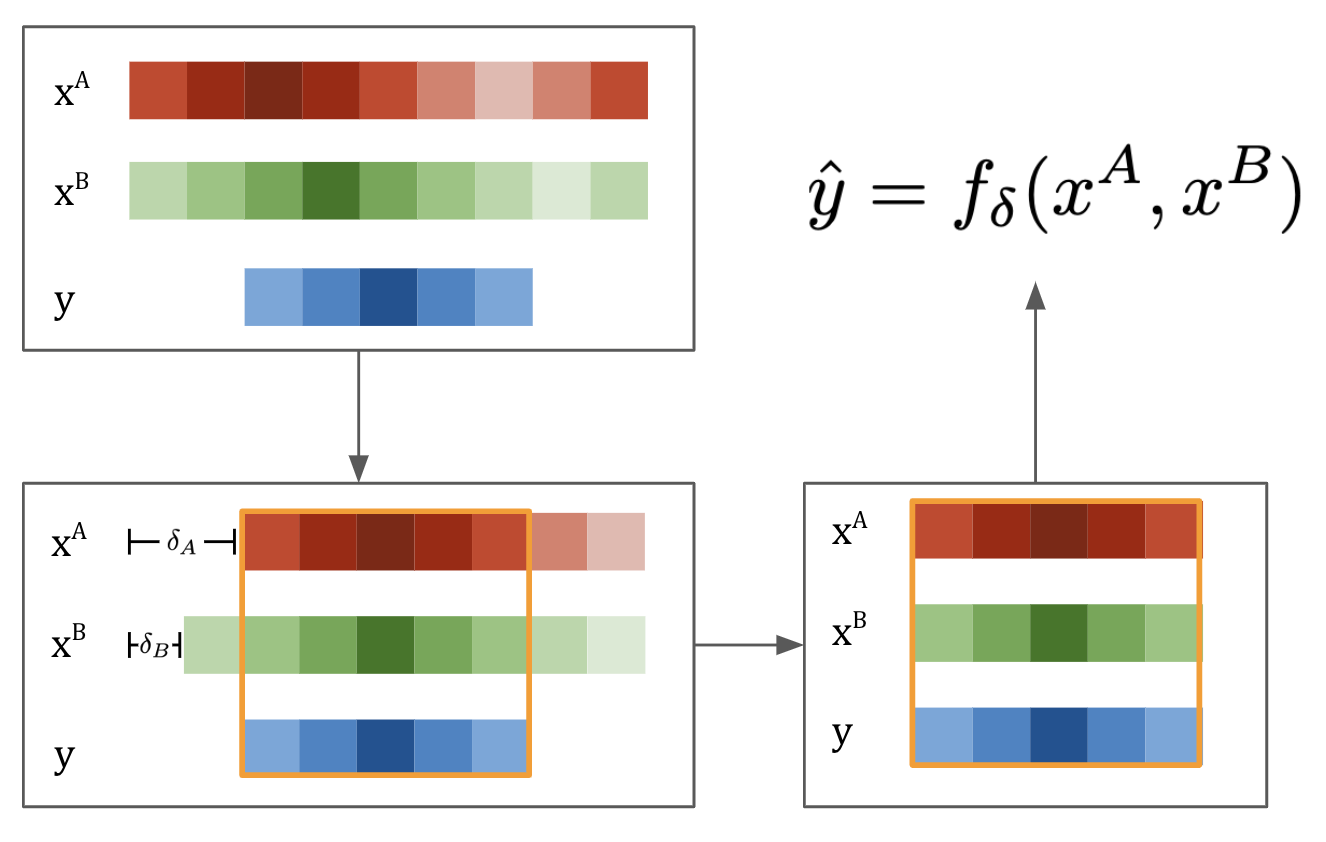

The key technical contribution of the paper is the Orthogonal Bootstrap algorithm, which leverages the debiased distribution compression structure of the model parameters to efficiently simulate input uncertainty.

The authors first show that the model parameters can be decomposed into a set of orthogonal vectors using a matrix factorization technique. They then demonstrate that new bootstrap samples can be generated by simply rotating these orthogonal vectors, without the need to retrain the entire model.

Formally, let $\theta$ be the model parameters and $X$ be the input data. The authors define the Orthogonal Bootstrap as follows:

- Decompose $\theta$ into a set of orthogonal vectors ${\mathbf{v}_1, \mathbf{v}_2, \ldots, \mathbf{v}_k}$ using a matrix factorization method such as butterfly factorization.

- For each bootstrap sample $b = 1, 2, \ldots, B$:

- Generate a set of rotation angles ${\theta_1^{(b)}, \theta_2^{(b)}, \ldots, \theta_k^{(b)}}$.

- Compute the new bootstrap parameters $\theta^{(b)} = \sum_{i=1}^k \cos(\theta_i^{(b)}) \mathbf{v}_i$.

- Evaluate the model on the original input data $X$ using the bootstrap parameters $\theta^{(b)}$.

The authors show that this approach is much faster than the standard bootstrap, as it avoids the need to retrain the entire model for each bootstrap sample. They also provide theoretical analysis to justify the statistical properties of the Orthogonal Bootstrap.

The experimental results in the paper demonstrate the effectiveness of the Orthogonal Bootstrap on a variety of datasets and models, including simultaneous inference in generalized linear models with unmeasured confounders and selection of the most probable best problems.

Critical Analysis

The Orthogonal Bootstrap technique presented in the paper is a novel and promising approach for efficiently simulating input uncertainty in machine learning models. The authors provide a clear and rigorous theoretical foundation for their method, as well as extensive experimental validation.

One potential limitation of the Orthogonal Bootstrap is that it relies on the assumption that the model parameters can be well-approximated by a set of orthogonal vectors. While the authors demonstrate the validity of this assumption for a variety of models, it may not hold true in all cases, particularly for highly complex or nonlinear architectures.

Additionally, the paper does not explore the potential limitations or failure modes of the Orthogonal Bootstrap, such as cases where the method may not provide significant computational savings or where the simulated uncertainty may not accurately reflect the true input uncertainty. Further research in these areas would be valuable to fully understand the scope and limitations of the technique.

Overall, the Orthogonal Bootstrap appears to be a useful and efficient tool for simulating input uncertainty, with potential applications in areas such as online-calibrated conformal prediction and Bayesian optimization. The paper makes a valuable contribution to the field of machine learning, and the authors' insights could inspire further advancements in efficient uncertainty quantification techniques.

Conclusion

The Orthogonal Bootstrap presented in this paper offers a novel and computationally efficient approach for simulating input uncertainty in machine learning models. By leveraging the orthogonal structure of the model parameters, the authors demonstrate that their method can provide significant speedups over traditional bootstrap techniques while maintaining the same level of accuracy.

This research has the potential to have a significant impact on a wide range of applications, from online-calibrated conformal prediction to Bayesian optimization, where the efficient simulation of input uncertainty is crucial. The authors' insights into the structure of model parameters and the use of orthogonal decomposition techniques could also inspire further advancements in the field of efficient uncertainty quantification.

Overall, this paper represents an important contribution to the machine learning literature, and the Orthogonal Bootstrap technique is a valuable tool for researchers and practitioners alike.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Orthogonal Bootstrap: Efficient Simulation of Input Uncertainty

Kaizhao Liu, Jose Blanchet, Lexing Ying, Yiping Lu

Bootstrap is a popular methodology for simulating input uncertainty. However, it can be computationally expensive when the number of samples is large. We propose a new approach called textbf{Orthogonal Bootstrap} that reduces the number of required Monte Carlo replications. We decomposes the target being simulated into two parts: the textit{non-orthogonal part} which has a closed-form result known as Infinitesimal Jackknife and the textit{orthogonal part} which is easier to be simulated. We theoretically and numerically show that Orthogonal Bootstrap significantly reduces the computational cost of Bootstrap while improving empirical accuracy and maintaining the same width of the constructed interval.

Read more5/2/2024

0

Robust Predictions with Ambiguous Time Delays: A Bootstrap Strategy

Jiajie Wang, Zhiyuan Jerry Lin, Wen Chen

In contemporary data-driven environments, the generation and processing of multivariate time series data is an omnipresent challenge, often complicated by time delays between different time series. These delays, originating from a multitude of sources like varying data transmission dynamics, sensor interferences, and environmental changes, introduce significant complexities. Traditional Time Delay Estimation methods, which typically assume a fixed constant time delay, may not fully capture these variabilities, compromising the precision of predictive models in diverse settings. To address this issue, we introduce the Time Series Model Bootstrap (TSMB), a versatile framework designed to handle potentially varying or even nondeterministic time delays in time series modeling. Contrary to traditional approaches that hinge on the assumption of a single, consistent time delay, TSMB adopts a nonparametric stance, acknowledging and incorporating time delay uncertainties. TSMB significantly bolsters the performance of models that are trained and make predictions using this framework, making it highly suitable for a wide range of dynamic and interconnected data environments.

Read more8/26/2024

🤯

0

Resampling methods for Private Statistical Inference

Karan Chadha, John Duchi, Rohith Kuditipudi

We consider the task of constructing confidence intervals with differential privacy. We propose two private variants of the non-parametric bootstrap, which privately compute the median of the results of multiple little bootstraps run on partitions of the data and give asymptotic bounds on the coverage error of the resulting confidence intervals. For a fixed differential privacy parameter $epsilon$, our methods enjoy the same error rates as that of the non-private bootstrap to within logarithmic factors in the sample size $n$. We empirically validate the performance of our methods for mean estimation, median estimation, and logistic regression with both real and synthetic data. Our methods achieve similar coverage accuracy to existing methods (and non-private baselines) while providing notably shorter ($gtrsim 10$ times) confidence intervals than previous approaches.

Read more6/5/2024

0

Bootstrap SGD: Algorithmic Stability and Robustness

Andreas Christmann, Yunwen Lei

In this paper some methods to use the empirical bootstrap approach for stochastic gradient descent (SGD) to minimize the empirical risk over a separable Hilbert space are investigated from the view point of algorithmic stability and statistical robustness. The first two types of approaches are based on averages and are investigated from a theoretical point of view. A generalization analysis for bootstrap SGD of Type 1 and Type 2 based on algorithmic stability is done. Another type of bootstrap SGD is proposed to demonstrate that it is possible to construct purely distribution-free pointwise confidence intervals of the median curve using bootstrap SGD.

Read more9/4/2024