Learning Decision Policies with Instrumental Variables through Double Machine Learning

0

Sign in to get full access

Overview

- This paper presents a method for learning decision policies using instrumental variables and double machine learning.

- The method aims to estimate the causal effect of a decision policy on an outcome of interest, even when the decision policy is confounded by unobserved factors.

- The paper builds on previous work in bounding causal effects with leaky instruments, estimating causal effects with double machine learning, and other causal hybrid modeling approaches.

Plain English Explanation

The paper describes a way to figure out the effects of a decision or policy, even when there are hidden factors that influence both the decision and the outcome. This is a common challenge in many real-world situations, where we can't directly observe all the things that go into a decision and its consequences.

The key idea is to use "instrumental variables" - factors that influence the decision, but don't directly affect the outcome in any other way. By leveraging these instrumental variables, the method can tease apart the causal effect of the decision policy from the confounding effects of the hidden factors.

The paper builds on previous work that has shown how to use machine learning techniques, like double machine learning, to estimate causal effects in the presence of complex relationships and confounding factors.

The approach proposed in this paper could be useful in a wide range of applications, from policy analysis to personalized decision-making, where understanding the true impact of decisions is crucial but hampered by unobserved confounding factors.

Technical Explanation

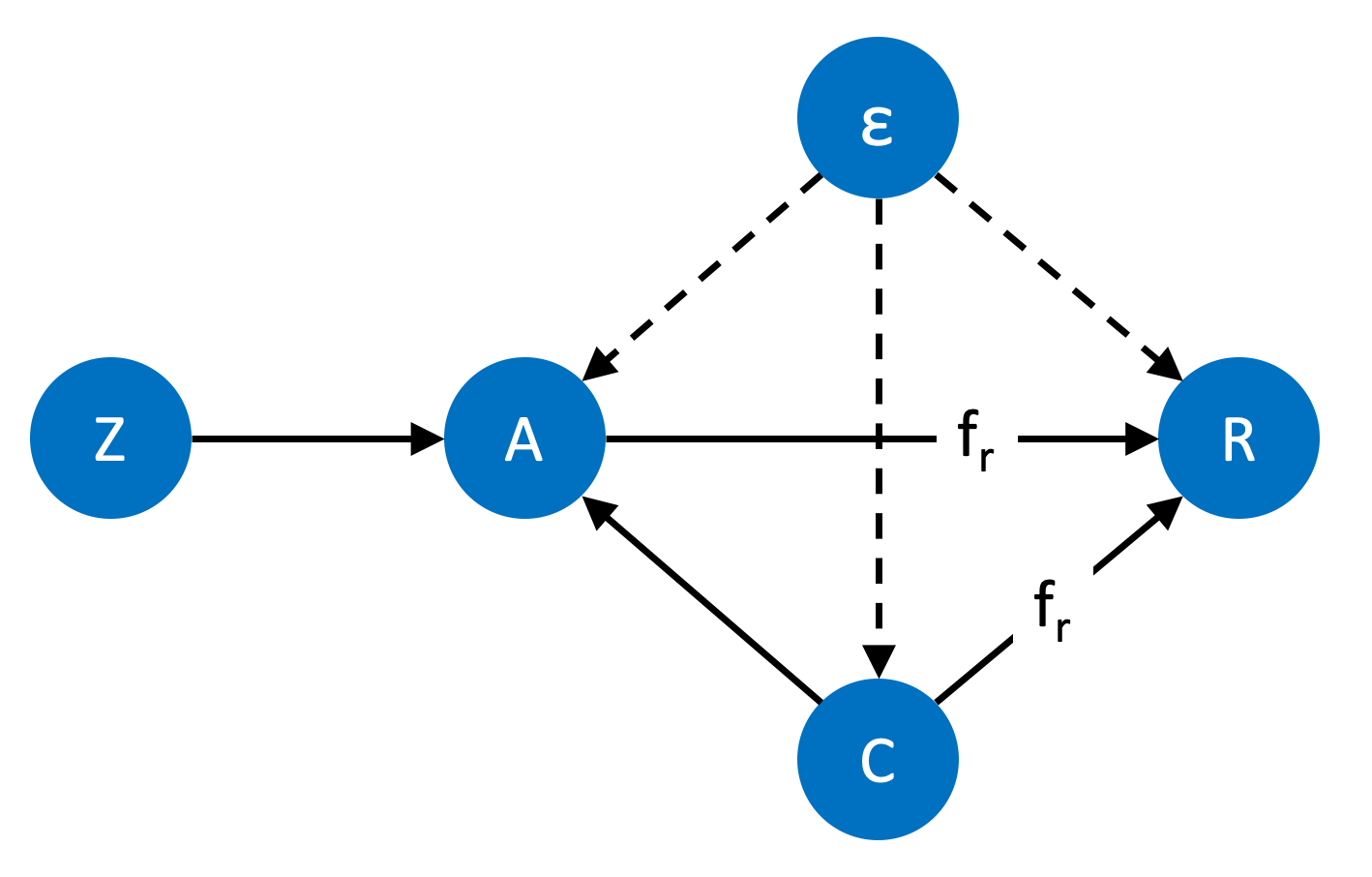

The paper presents a method for learning decision policies using instrumental variables and double machine learning. The core idea is to leverage "instrumental variables" - factors that influence the decision policy, but do not directly affect the outcome of interest in any other way.

By using instrumental variables, the method can isolate the causal effect of the decision policy from the confounding effects of unobserved factors that influence both the decision and the outcome. This is achieved through a two-stage process:

- First, the method learns a model to predict the decision policy based on the observed covariates and instrumental variables.

- Second, it uses this predicted decision policy, along with the observed covariates, to estimate the causal effect on the outcome of interest.

This approach builds on previous work in bounding causal effects with leaky instruments, estimating causal effects with double machine learning, and other causal hybrid modeling approaches. By combining instrumental variables with double machine learning, the method can flexibly handle complex, nonlinear relationships and provide robust estimates of the causal effect of the decision policy.

The authors demonstrate the effectiveness of their approach through simulation studies and real-world applications, such as unveiling the impact of macroeconomic policies with double machine learning and a double machine learning approach to combining experimental and observational data.

Critical Analysis

The paper presents a well-designed and technically sound approach for learning decision policies with instrumental variables and double machine learning. The authors have carefully considered the limitations of previous methods and have proposed a novel solution that addresses these shortcomings.

One potential caveat is the assumption that the instrumental variables are indeed valid, meaning they influence the decision policy but do not directly affect the outcome. In practice, finding suitable instrumental variables can be challenging, and violating this assumption could lead to biased estimates.

Additionally, the paper focuses on the case where the decision policy is confounded by unobserved factors. While this is a common and important problem, there may be other scenarios where the decision policy is influenced by observed factors that the method does not explicitly address.

Further research could explore the robustness of the method to violations of the instrumental variable assumptions, as well as extend the approach to handle a broader range of confounding scenarios. Comparing the performance of this method to other causal inference techniques, such as causal hybrid modeling or combining experimental and observational data, could also provide valuable insights.

Conclusion

This paper presents a novel method for learning decision policies using instrumental variables and double machine learning. The approach aims to estimate the causal effect of a decision policy on an outcome of interest, even when the decision policy is confounded by unobserved factors.

By leveraging instrumental variables and the flexibility of machine learning techniques, the method can tease apart the true causal impact of the decision policy from the confounding effects of hidden factors. This could have significant implications for a wide range of applications, from policy analysis to personalized decision-making, where understanding the causal effects of decisions is crucial but often hampered by unobserved confounding.

While the paper highlights some potential limitations and areas for further research, the proposed approach represents an important advancement in the field of causal inference and decision-making under uncertainty.

This summary was produced with help from an AI and may contain inaccuracies - check out the links to read the original source documents!

Related Papers

0

Learning Decision Policies with Instrumental Variables through Double Machine Learning

Daqian Shao, Ashkan Soleymani, Francesco Quinzan, Marta Kwiatkowska

A common issue in learning decision-making policies in data-rich settings is spurious correlations in the offline dataset, which can be caused by hidden confounders. Instrumental variable (IV) regression, which utilises a key unconfounded variable known as the instrument, is a standard technique for learning causal relationships between confounded action, outcome, and context variables. Most recent IV regression algorithms use a two-stage approach, where a deep neural network (DNN) estimator learnt in the first stage is directly plugged into the second stage, in which another DNN is used to estimate the causal effect. Naively plugging the estimator can cause heavy bias in the second stage, especially when regularisation bias is present in the first stage estimator. We propose DML-IV, a non-linear IV regression method that reduces the bias in two-stage IV regressions and effectively learns high-performing policies. We derive a novel learning objective to reduce bias and design the DML-IV algorithm following the double/debiased machine learning (DML) framework. The learnt DML-IV estimator has strong convergence rate and $O(N^{-1/2})$ suboptimality guarantees that match those when the dataset is unconfounded. DML-IV outperforms state-of-the-art IV regression methods on IV regression benchmarks and learns high-performing policies in the presence of instruments.

Read more7/1/2024

0

Data-driven Conditional Instrumental Variables for Debiasing Recommender Systems

Zhirong Huang, Shichao Zhang, Debo Cheng, Jiuyong Li, Lin Liu, Guangquan Lu

In recommender systems, latent variables can cause user-item interaction data to deviate from true user preferences. This biased data is then used to train recommendation models, further amplifying the bias and ultimately compromising both recommendation accuracy and user satisfaction. Instrumental Variable (IV) methods are effective tools for addressing the confounding bias introduced by latent variables; however, identifying a valid IV is often challenging. To overcome this issue, we propose a novel data-driven conditional IV (CIV) debiasing method for recommender systems, called CIV4Rec. CIV4Rec automatically generates valid CIVs and their corresponding conditioning sets directly from interaction data, significantly reducing the complexity of IV selection while effectively mitigating the confounding bias caused by latent variables in recommender systems. Specifically, CIV4Rec leverages a variational autoencoder (VAE) to generate the representations of the CIV and its conditional set from interaction data, followed by the application of least squares to derive causal representations for click prediction. Extensive experiments on two real-world datasets, Movielens-10M and Douban-Movie, demonstrate that our CIV4Rec successfully identifies valid CIVs, effectively reduces bias, and consequently improves recommendation accuracy.

Read more8/20/2024

↗️

0

Nonparametric Instrumental Variable Regression through Stochastic Approximate Gradients

Yuri Fonseca, Caio Peixoto, Yuri Saporito

Instrumental variables (IVs) provide a powerful strategy for identifying causal effects in the presence of unobservable confounders. Within the nonparametric setting (NPIV), recent methods have been based on nonlinear generalizations of Two-Stage Least Squares and on minimax formulations derived from moment conditions or duality. In a novel direction, we show how to formulate a functional stochastic gradient descent algorithm to tackle NPIV regression by directly minimizing the populational risk. We provide theoretical support in the form of bounds on the excess risk, and conduct numerical experiments showcasing our method's superior stability and competitive performance relative to current state-of-the-art alternatives. This algorithm enables flexible estimator choices, such as neural networks or kernel based methods, as well as non-quadratic loss functions, which may be suitable for structural equations beyond the setting of continuous outcomes and additive noise. Finally, we demonstrate this flexibility of our framework by presenting how it naturally addresses the important case of binary outcomes, which has received far less attention by recent developments in the NPIV literature.

Read more5/27/2024

0

Geometry-Aware Instrumental Variable Regression

Heiner Kremer, Bernhard Scholkopf

Instrumental variable (IV) regression can be approached through its formulation in terms of conditional moment restrictions (CMR). Building on variants of the generalized method of moments, most CMR estimators are implicitly based on approximating the population data distribution via reweightings of the empirical sample. While for large sample sizes, in the independent identically distributed (IID) setting, reweightings can provide sufficient flexibility, they might fail to capture the relevant information in presence of corrupted data or data prone to adversarial attacks. To address these shortcomings, we propose the Sinkhorn Method of Moments, an optimal transport-based IV estimator that takes into account the geometry of the data manifold through data-derivative information. We provide a simple plug-and-play implementation of our method that performs on par with related estimators in standard settings but improves robustness against data corruption and adversarial attacks.

Read more5/21/2024